Are Staff Gifts Tax Deductible?

Table Of Contents

- Are Christmas Bonuses Employee Gifts Tax Deductible?

- Are Staff Gifts Tax Deductible at Christmas Party?

- Are Gifts to Employees Tax Deductible on Christmas?

- VAT on Christmas Gifts to Your Clients

- Frequently Asked Questions

Are Christmas Bonuses Employee Gifts Tax Deductible?

If you give a cash bonus to your employees, it counts as earnings, so you will need to add that to the employee’s payroll and deduct the relevant tax and National Insurance. Many employers wonder, are staff gifts tax deductible when it comes to bonuses. The answer is yes, but only if the bonus is part of the regular pay and taxed accordingly

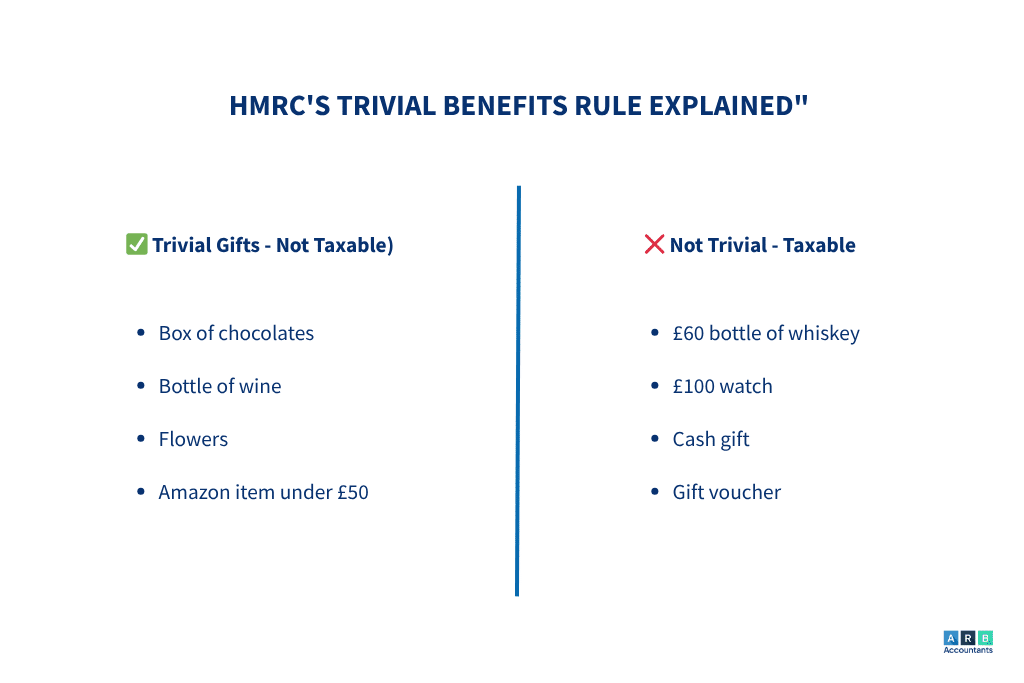

If you provide your employees with gifts such as chocolates, a bottle of wine, etc., there are no tax implications if the gift is considered “trivial” by HMRC. However, are staff gifts tax deductible when they are seen as trivial? Generally, anything up to £50 is considered trivial, and thus not subject to tax. There is no set monetary limit for trivial gifts, but typically up to £50 would be deemed acceptable by HMRC.

Are Staff Gifts Tax Deductible at Christmas Party?

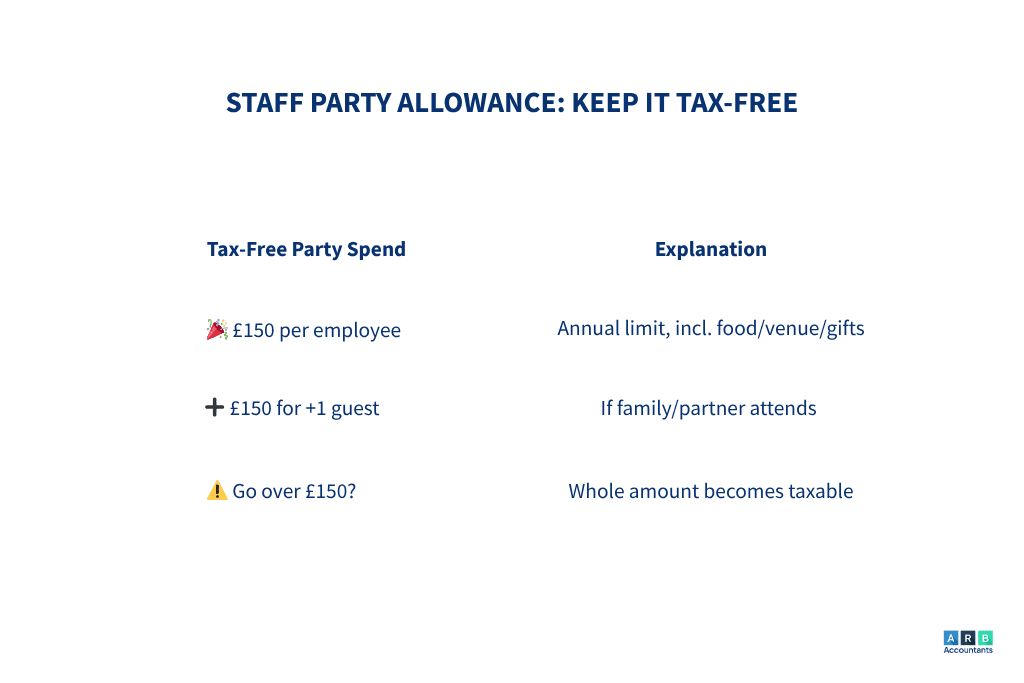

You can spend up to £150 per year per head without any tax implications, which raises the question, are staff gifts tax deductible in relation to party expenses?. The £150 is the annual limit, so if you have more than one party in a year, the total spent per person for the year should be less than £150. If it goes over £150, the whole amount becomes taxable. In this case, the answer to are staff gifts tax deductible is yes, provided you stay within the limits. Additionally, you can claim an extra £150 per person for each employee if they bring along a partner or family member. To claim the £150 exemption, the party must be open to all employees.

A very helpful company . They have explained things my previous accountant didn't and I cannot recommend them highly enough.

Are Gifts to Employees Tax Deductible on Christmas?

These are treated as business entertainment and are disallowed for tax purposes unless the following three conditions are met:

-

The gift must carry a business logo and be branded as advertising. The logo should be on the gift itself, not just on the wrapping paper.

-

The value of the gift must be less than £50.

-

The gift must not be food, drink, tobacco, or vouchers.

So, are staff gifts tax deductible if they are given to clients? In this case, the tax treatment is different from gifts to employees, as the focus is on business branding.

UK employee gifts, like Christmas presents, are normally not taxed if they meet specific conditions. If the gift is below cost (less than £50) and is neither cash nor a cash voucher, it is normally not taxed according to the 'trivial benefits' rule. However, if the gift exceeds this threshold or is cash, it may be taxable and subject to National Insurance contributions.

VAT on Christmas Gifts to Your Clients

You can claim the VAT on business gifts made to customers if the value of the gift does not exceed £50. This limit applies over a 12-month period. However, if you’re wondering are staff gifts are tax deductible under VAT rules, you’ll need to account for output VAT on the value of the gift if it exceeds £50 in a year.

For more information, please contact us on 01702 345 207 or email us at [email protected]

Frequently Asked Questions

1. Are staff gifts tax deductible for businesses?

Yes, staff gifts can be tax deductible if they qualify as a business expense. Non-cash gifts under £50, considered trivial benefits by HMRC, are generally deductible. However, cash gifts and vouchers must go through payroll and do not qualify for deductions.

2. Are employee gifts taxable under HMRC rules?

Employee gifts are taxable if they are cash or cash equivalents like vouchers. Non-cash gifts, such as chocolates or wine, are usually exempt if they fall under the trivial benefits rule.

3. Are gifts to employees tax deductible if they exceed £50?

If a gift to an employee exceeds £50 and is not considered trivial, it is subject to tax and National Insurance. It may still be a deductible business expense, but it must be reported on a P11D form.

4. Are staff gifts allowable for corporation tax deductions?

Non-cash staff gifts that meet the trivial benefits criteria are allowable for corporation tax deductions. However, gifts considered a reward for services or exceeding the trivial benefits limit must go through payroll and cannot be deducted.

5. Are gift vouchers taxable in the UK for employees?

Yes, gift vouchers are taxable in the UK as they are treated as cash equivalents. Their value must be included in the employee’s earnings and taxed accordingly. Unlike trivial non-cash gifts, they do not qualify for tax exemptions.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008