CIS Expenses Guide for Construction Workers UK

If you work in construction as a subcontractor, the Construction Industry Scheme (CIS) means your contractor takes tax off your pay before it reaches you. That deduction takes no account of your running costs, so most subcontractors overpay and are owed money back at the end of the year.

Margins in construction are tight enough without leaving cash sitting with HMRC. This CIS expenses guide sets out what counts as an allowable expense, how to record it properly, and how those costs turn into a tax refund. Our construction accountants do this for subcontractors across the UK, and the rules below apply whether you file your own return or hand it to an accountant.

Table Of Contents

- What is the Construction Industry Scheme (CIS) and why does understanding expenses matter?

- What qualifies as an allowable expense under CIS?

- How should travel, mileage & CIS mileage allowance be handled and claimed?

- Which tools, equipment and protective clothing can be claimed under CIS expenses?

- How are job materials treated differently from labour in CIS expenses?

- Can telephone, internet, meals whilst working, and overnight stays be claimed?

- What evidence should subcontractors retain to support their CIS tax return?

- What are common misconceptions around CIS expenses & how can they be avoided?

- How does understanding these expenses impact your CIS tax return and overall tax efficiency?

- How to claim a CIS tax refund

What is the Construction Industry Scheme (CIS) and why does understanding expenses matter?

CIS is HMRC’s system for collecting tax from construction subcontractors. Instead of waiting for you to file a return, your contractor takes the tax straight out of your pay and sends it to HMRC. The rate depends on your status:

- 20% if you are registered for CIS

- 30% if you are not registered

- 0% if you hold gross payment status

The catch is that this is a flat deduction on your labour. It ignores your expenses entirely. Your real tax bill is worked out on your profit, which is your income minus your allowable costs, so the amount taken at source is almost always more than you actually owe. Misclassify your expenses, or leave them off altogether, and you can hand HMRC hundreds of pounds you were never required to pay.

If you also run contractor-style projects, it is worth having both sides of the work reviewed together. Our contractor accountants prepare and file CIS returns, keep you clear of late-filing penalties, and make sure every claim that reduces your bill is on the return.

What qualifies as an allowable expense under CIS?

HMRC will only allow a cost if it passes the “wholly, exclusively and necessarily” test. In plain terms, the expense has to be there because of your construction work and nothing else. That test is what decides your CIS subcontractor allowable expenses.

The first split to get right is labour versus materials. Labour has the CIS deduction taken off it; materials and your other business costs do not. If your invoices don’t separate the two, GOV.UK warns that a contractor can end up applying the deduction to the whole amount, materials included, and you lose net pay you should have kept.

So itemise every invoice and show labour and materials on separate lines. It’s the simplest safeguard against over-deduction, and it leaves you a clear record if HMRC ever queries the return.

The costs you can claim usually fall into four groups:

- Tools, equipment and protective clothing

- Materials bought directly for a job

- Professional fees, such as accountancy, insurance and training

- Office and admin costs, including a fair share of phone, stationery and software

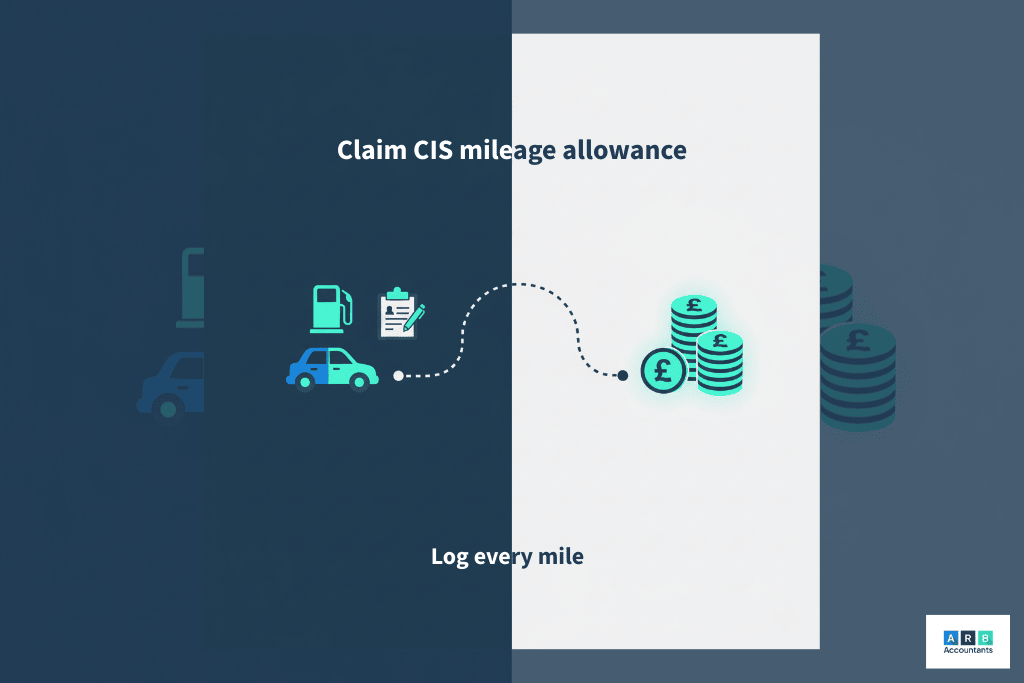

How should travel, mileage & CIS mileage allowance be handled and claimed?

Travel is where subcontractors slip up most often. You can claim the cost of getting to a temporary workplace, which HMRC defines as a site you expect to work at for less than 24 months. Travel to a permanent base doesn’t qualify.

There are two ways to claim. The first is the CIS mileage allowance, which uses HMRC’s flat rates:

- 45p per mile for the first 10,000 business miles in the tax year

- 25p per mile after that

The second is your actual running costs: fuel, repairs, insurance, servicing and road tax, scaled down to your business use. Newer, economical vehicles usually do better on the flat mileage rate; older vans with high mileage often do better on actual costs. Pick one method per vehicle and keep a mileage log either way.

One thing to watch is CIS deductions on travel expenses. If a contractor takes the 20% or 30% deduction off money that is really a travel reimbursement, you lose cash on every payment. Check your deduction statements and query anything that looks wrong.

Which tools, equipment and protective clothing can be claimed under CIS expenses?

Tools, equipment and protective clothing are some of the most straightforward claims. HMRC lets you claim anything bought wholly and necessarily for construction work: drills, power saws, safety helmets, steel-toe boots, hi-vis and the rest of your PPE.

Where subcontractors get caught out is everyday clothing. Ordinary jeans or a winter coat aren’t allowable, even if you only ever wear them on site. Specialist protective gear qualifies; general clothing doesn’t.

For the cost itself, the usual position is full relief in the year you buy the kit. Under the cash basis most subcontractors now use, tools are simply deducted when you pay for them, so a £1,200 drill set is a £1,200 deduction this year. The Annual Investment Allowance does the same job if you use traditional accounting. Spreading the cost over several years is possible, but it’s a deliberate planning choice, usually only worth it when claiming the lot in one go would waste your personal allowance.

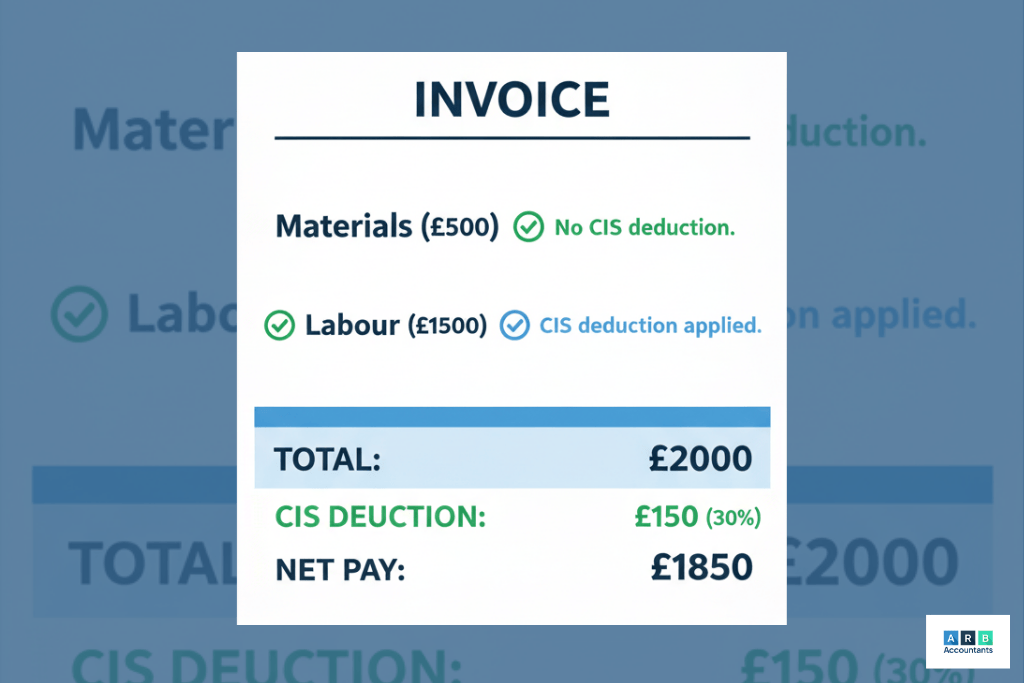

How are job materials treated differently from labour in CIS expenses?

Materials and labour are treated very differently under CIS, and mixing them up costs subcontractors real money.

Materials, such as cement, bricks or timber, are paid gross, with no CIS deduction taken off them. Labour is different: it always has the 20% or 30% deduction applied, depending on your registration status.

The problem comes when an invoice doesn’t separate the two. Say you invoice £2,000 without splitting out £500 of materials. The contractor can apply the deduction to the whole £2,000 instead of just the £1,500 of labour. At the 30% rate, that’s £150 withheld that should have stayed in your pocket.

The fix is simple. Itemise every invoice so labour and materials sit on separate lines:

- Labour: £1,500, CIS deduction applies

- Materials: £500, no CIS deduction

- Total invoice: £2,000

Do this on every job. The deduction then only ever comes off your labour, and you have a clean record if HMRC reviews the return.

Can telephone, internet, meals whilst working, and overnight stays be claimed?

The smaller running costs are the ones subcontractors forget, and they add up. Some household and subsistence costs are allowable too, as long as you only claim the business share.

Phone and internet are the clearest example. If roughly half your mobile use is for work, you can claim half the bill. Claim the business proportion, not the lot.

Meals are tighter. Food near home, or at a site you travel to every day, isn’t allowable. But a meal while you’re away at a temporary workplace counts as subsistence, and so does overnight accommodation when a job keeps you away from home, as long as you keep the receipts.

Then there are dual-purpose costs. Home broadband or a personal phone gets used for both work and life, so you can only claim the part that relates to work. Pick a fair split, note down how you worked it out, and stick to it.

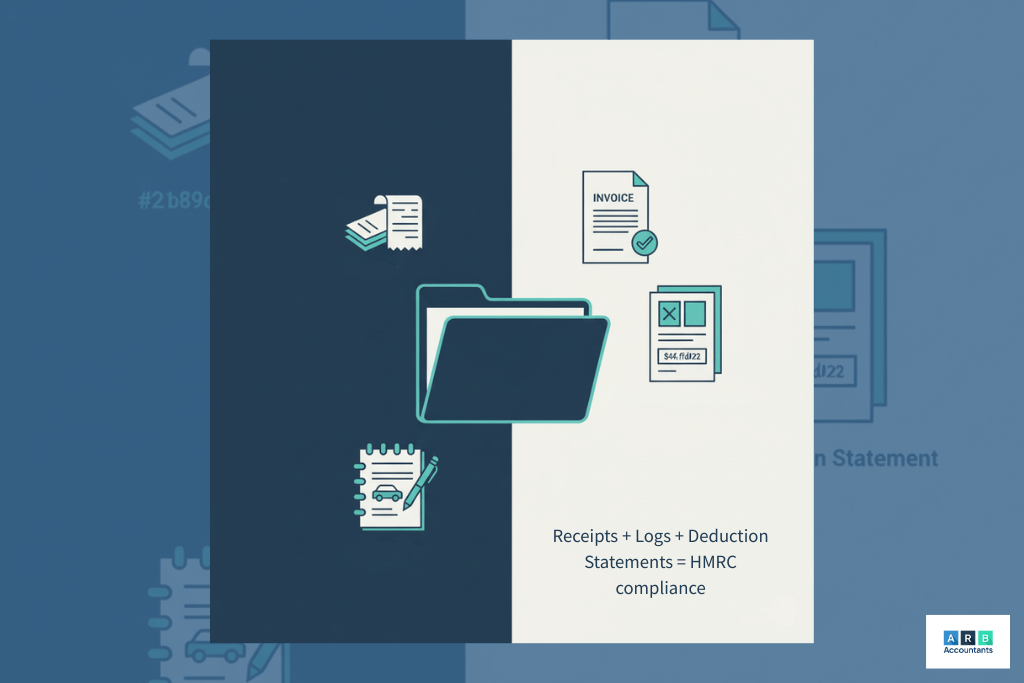

What evidence should subcontractors retain to support their CIS tax return?

Every claim needs evidence behind it. That has always been true, but since Making Tax Digital for Income Tax started in April 2026 for anyone with income over £50,000, keeping digital records is now a legal requirement rather than just good housekeeping. To back up your return, hold on to:

- Receipts

- Invoices

- Mileage logs

- The CIS deduction statements your contractors give you

The monthly Payment and Deduction Statement matters most. Your contractor has to give you one every month, and it should show your gross pay, any materials, the deduction taken and what you were left with. Without it, you can’t check whether the right tax was withheld, let alone reconcile a full year of payments.

Keep all of this digitally. A shared drive or a bookkeeping app, with a folder per job for receipts, invoices and mileage, means nothing goes missing and you can find any document fast if HMRC asks. Subcontractors with tidy records get their refunds quicker, and have far less to worry about if a return is ever queried.

What are common misconceptions around CIS expenses & how can they be avoided?

A few myths cost subcontractors money every year. These are the ones that come up most.

The first is that meals are always claimable. They aren’t. Food only counts as subsistence when it’s tied to a temporary workplace. A sandwich at a site you’ve worked on for two years doesn’t qualify; a meal while you’re away on a six-month job does. It’s the question behind a lot of “CIS tax return: what can I claim?” searches.

The second runs the other way: that a big tool purchase has to be spread over several years. For most subcontractors it doesn’t. The cost normally comes off in full in the year you buy it, whether you’re on the cash basis or claiming the Annual Investment Allowance.

The third is dual-purpose costs. If you use your mobile for both work and personal calls, you can’t claim the whole bill, only the work share. Claiming 100% of a cost that is plainly part-personal is exactly the kind of thing that doesn’t survive an HMRC review.

How does understanding these expenses impact your CIS tax return and overall tax efficiency?

Getting your expenses right changes your refund pound for pound. Every £1 of allowable cost takes £1 off your taxable profit. For a basic-rate subcontractor that means 20% Income Tax plus 6% Class 4 National Insurance, so roughly 26p comes back for every pound you claim.

Put numbers on it. A subcontractor earns £40,000 in a year, all under CIS, so £8,000 has already been deducted at source. Across the year they run up £6,000 of genuine costs: mileage, tools, PPE and the odd night’s accommodation. Claiming that £6,000 cuts their Income Tax and National Insurance bill by roughly £1,560. Lose those receipts and that £1,560 stays with HMRC instead of coming back to them.

That is why record-keeping is worth the effort. It isn’t paperwork for its own sake; it’s money. We prepare CIS returns for subcontractors across Southend and the rest of the UK, and the job is always the same: find every cost that counts, and make sure it lands on the return.

ARB Accountants have been my accountants for the past 5 years and I can say they are best at what they do, they look after my tax returns, and they make the whole process very easy. Any questions I have are answered in a timely manner, very reasonably priced too, I would definitely recommend them.

How to claim a CIS tax refund

You claim a CIS refund by filing a Self Assessment tax return for the tax year, declaring every CIS deduction taken from your payments alongside all your allowable expenses. HMRC compares the tax deducted at source against what you actually owe and refunds the difference, usually within 5 to 10 working days of processing your return.

Most CIS subcontractors are overpaying tax without knowing it. Under CIS, contractors deduct 20% or 30% from your payments before you receive them. Once you account for your allowable expenses and the actual tax you owe on your profits, the amount deducted is almost always higher than what you actually owe. The difference is your refund.

How much could you be owed?

The amount depends on your total earnings, your expenses, and your personal tax allowance. Take a subcontractor who earned £30,000 in a tax year, had £5,000 of allowable expenses, and was on the 20% CIS deduction rate. Their contractor would already have deducted £6,000 from their payments. Their profit works out at £25,000, so after the £12,570 personal allowance their actual liability is around £2,486 in Income Tax plus roughly £746 in Class 4 National Insurance. That is about £3,230 in total. Because £6,000 was taken at source, that subcontractor is owed a refund of around £2,750.

The more expenses you claim correctly, the larger your refund. This is why keeping receipts and mileage logs throughout the year matters, and why proper tax advice before you file can make a real difference to what you get back.

The process for claiming back CIS tax

- Register for Self Assessment with HMRC if you have not already done so

- File a Self Assessment tax return covering the tax year (6 April to 5 April)

- Include all CIS deductions suffered during the year on the return

- Claim all allowable expenses covered in this guide

- HMRC calculates what you owe and issues a refund for any overpayment

- Refunds are paid directly to your bank account, usually within 5 to 10 working days of HMRC processing the return

The deadline for filing your Self Assessment return online is 31 January each year for the previous tax year. If you are filing for the first time, you need to register with HMRC by 5 October following the end of the tax year.

What most subcontractors get wrong

The most common reason subcontractors miss out on their full refund is underclaiming expenses. Many do not claim mileage at all, forget professional fees like insurance and accountancy costs, or fail to separate materials from labour on invoices. Each missed expense reduces the refund you receive.

Filing the return yourself is possible but errors are common. A misclassified expense or a missed CIS deduction on the return can mean a smaller refund or an unexpected tax bill. Our self-assessment service handles the full return, ensures every allowable expense is captured, and deals directly with HMRC on your behalf.

Get back every pound you are owed

We handle CIS Self Assessment returns for subcontractors across the UK. We claim every allowable expense, account for all deductions, and make sure you get back every pound you are owed.

Frequently Asked Questions

How do I claim my CIS refund?

You claim your CIS refund by filing a Self Assessment tax return with HMRC for the relevant tax year. You include all CIS deductions that were taken from your payments during the year, along with your allowable expenses. HMRC calculates the difference between what was deducted and what you actually owe. If more was deducted than your tax liability, the overpayment is refunded directly to your bank account. The deadline to file online is 31 January each year. Our self-assessment service handles this process in full.

How much CIS can I claim back?

The amount you can claim back depends on your total CIS earnings, the deductions taken, your allowable expenses, and your personal tax allowance. Most subcontractors are due a refund because contractors deduct 20% from all payments regardless of your actual tax liability. Once your personal allowance and expenses are factored in, the tax you genuinely owe is almost always less than what was deducted. We can calculate your exact refund before you file.

What can I claim for on my CIS tax return?

On your CIS Self Assessment return you can claim any expense that was wholly, exclusively and necessarily incurred in carrying out your construction work. This includes mileage or vehicle running costs for travel to temporary workplaces, tools and equipment, materials you purchased for jobs, protective clothing, phone and internet costs used for work, public liability insurance, and professional fees including accountancy costs. Each of these reduces your taxable profit and increases your refund.

What is the CIS mileage allowance?

CIS subcontractors can claim 45p per mile for the first 10,000 miles in a tax year and 25p per mile after that for travel to temporary workplaces. Alternatively you can claim actual vehicle running costs including fuel, insurance, repairs, and road tax.

What expenses can a CIS-registered subcontractor claim?

A CIS registered subcontractor can claim tools, protective clothing, materials used for jobs, travel to temporary sites, accommodation for site work, and a fair proportion of household costs like phone or internet used for business. These costs reduce taxable profit and increase refunds.

How do I report CIS expenses on a construction industry scheme tax return?

You must record these under the ‘expenses’ section of your self-employment pages. Following a detailed cis expenses guide ensures you don’t miss categories like cis travel expenses or professional fees.

Can I claim mileage or CIS mileage allowance for CIS expenses?

Yes. The cis mileage allowance is currently 45p per mile for the first 10,000 miles. This is often the biggest factor in securing a construction worker tax refund.

What records does HMRC require for CIS expense claims?

HMRC requires proof of purchase, mileage logs, and your CIS deduction statements. Keep these organized to ensure your hmrc cis tax return is accurate.

How do I treat overnight stays, meals and dual-purpose costs under CIS?

Overnight stays are allowable if essential for work. Meals are subsistence (only at temporary sites). Dual-purpose costs must be split by percentage of business use. This is a standard part of any cis tax return what can i claim checklist.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008