How Likely Are You to Be Investigated by HMRC? 2026 Guide

How likely are you to be investigated by HMRC?

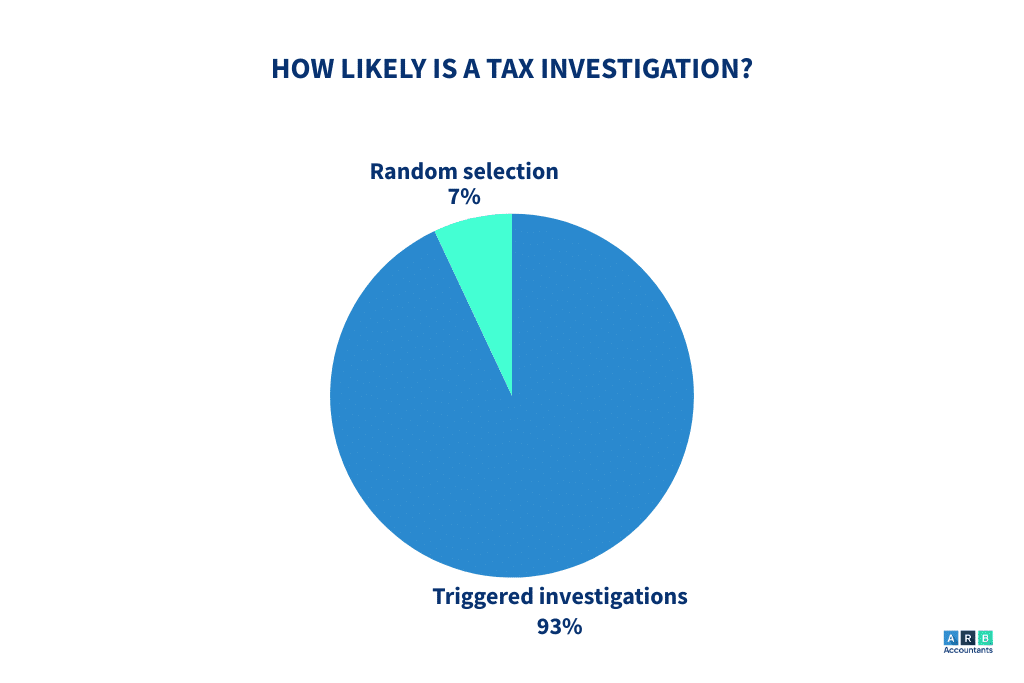

Roughly 7% of HMRC tax investigations are random; the other 93% are triggered. Across the UK's ~12 million Self Assessment filings, only a small fraction face a formal enquiry each year. But if HMRC's Connect system flags a discrepancy with bank, Land Registry, employer or digital-platform data, your odds change quickly. Cash-trade businesses, high-income earners and frequent amenders sit at the top of the risk list.

This guide covers your real chances of being investigated, the red flags HMRC watches for, what triggers a compliance check, the 5 stages of an HMRC investigation, how far back HMRC can go, and what to do if you’re worried.

Table Of Contents

- How Likely Are You to Be Investigated by HMRC?

- What Are the Chances of Being Investigated by HMRC?

- What Triggers an HMRC Investigation? (HMRC Red Flags)

- The 5 Stages of an HMRC Tax Investigation

- How Far Back Can HMRC Go?

- How HMRC Knows About Your Income & Assets

- Can HMRC Check Your Bank Account?

- HMRC’s Personal Expenditure Crackdown

- HMRC Wage Raid & Payroll Compliance Checks

- Side Hustle & Vinted Data Sharing (One Year In)

- How Do HMRC Decide Who to Investigate?

- Do HMRC Do Random Checks?

- What Happens During an HMRC Tax Investigation?

- How Will I Know If HMRC Are Investigating Me?

- When Does HMRC Investigate the Self-Employed?

- How Long Does an HMRC Investigation Take?

- What Happens When You Report Someone to HMRC?

- MTD for ITSA: One Trigger to Watch in 2026

- How to Reduce Your Chances of an HMRC Investigation

- Get Expert Help with an HMRC Investigation

How Likely Are You to Be Investigated by HMRC?

About 7% of HMRC tax investigations are random checks. Even a business that's done nothing wrong can be picked. The other 93% are triggered, usually by an error on the return, data HMRC has cross-matched from somewhere else, or a tip-off.

If your records are clean and your numbers line up with what HMRC already knows, the odds of an investigation are low. Inconsistencies, mismatches against third-party data, or working in a high-risk sector all push the odds up sharply.

How many people get investigated by HMRC?

HMRC opens hundreds of thousands of compliance checks each year, against ~12 million Self Assessment returns and roughly 5.5 million UK businesses. Most are narrow aspect enquiries — single questions about a single line on a return. Only a small fraction escalate to full investigations.

What are the actual odds of getting audited?

For a typical Self Assessment taxpayer with clean records, the odds of a full investigation in any single year are well under 1 in 50. They climb fast for cash-trade businesses (construction, hospitality, taxis, beauty), people with offshore accounts, frequent amenders, and anyone whose return doesn't line up with bank, Land Registry or digital-platform data HMRC already holds. ("Audit" is the US term; HMRC calls it a compliance check or enquiry.)

HMRC now receives international banking data under global information sharing agreements. One of our clients received a letter saying they had discovered undisclosed foreign interest income — in this case, from fixed deposits in India.

Her previous accountant had never informed her that UK tax residents must declare worldwide income. We helped her prepare a disclosure, calculating interest, penalties, and the additional tax owed for several years. HMRC hasn't responded yet, but we expect the matter to be resolved similarly with tax and penalties paid, and no further consequences.

This case highlights the importance of proper advice, especially for clients with overseas assets or accounts.

What Are the Chances of Being Investigated by HMRC?

It depends on your risk profile. The biggest single multipliers are cash-based trades, offshore income, repeated amendments, late filings, and any mismatch between your return and third-party data HMRC already holds (bank interest, employer payroll, Land Registry, digital platforms). A clean, on-time return that matches those data feeds is in the low-risk band.

The rest are driven by data: discrepancies on a return, unusual expense claims, undeclared income, or a mismatch between what you’ve reported and what HMRC has been told by a bank, employer, digital platform or overseas tax authority.

Some sectors carry higher risk by nature. Cash trades like construction, hospitality, beauty, taxis and market traders are harder for HMRC to verify independently, so they get more attention. VAT-registered businesses and PAYE employers should also expect routine compliance contact every few years, even when nothing is wrong.

There’s a long-running rumour that HMRC sets internal investigation quotas. True or not, the pattern is the same year after year: small inconsistencies get picked up, and the easiest way to lower your odds is to make sure your filings line up with the data HMRC already holds.

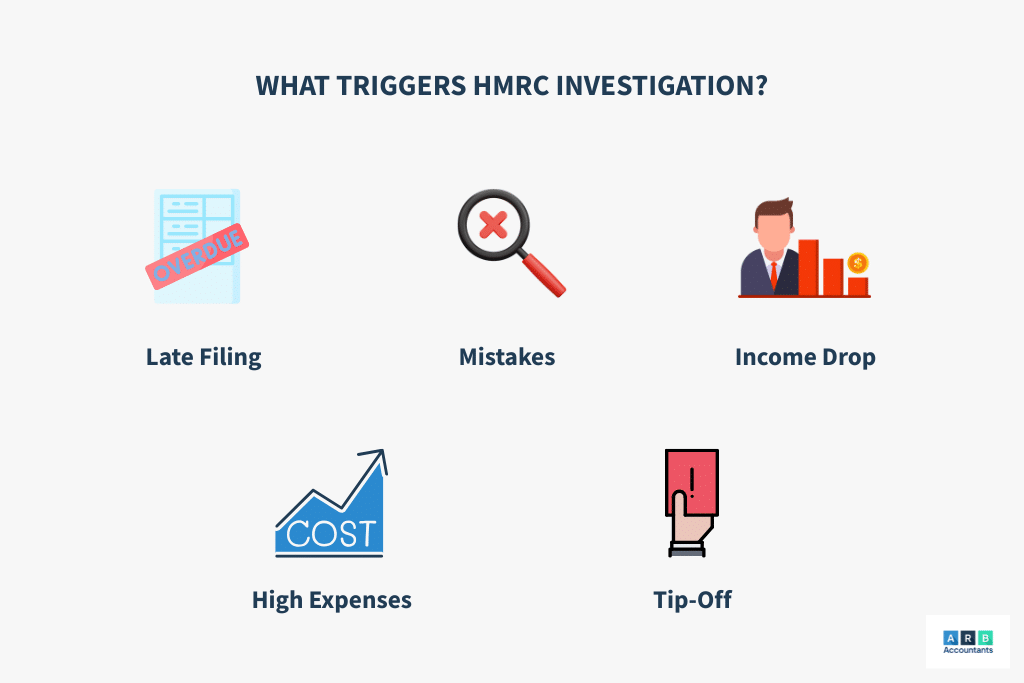

What Triggers an HMRC Investigation? (HMRC Red Flags)

Most HMRC investigations are triggered, not random. The trigger is almost always one of two things: something on your return doesn't match what HMRC already knows (banks, employers, Land Registry, digital platforms, overseas tax authorities), or it looks abnormal next to the rest of your sector.

What would make HMRC investigate you?

The most common triggers, in order of frequency: data mismatches picked up by Connect (bank interest, platform sales, rental property, employer payroll), late filings, expense claims that look high for your sector, large unexplained income swings, repeated amendments, and tip-offs HMRC's fraud system has risk-scored as credible.

HMRC red flags

| Red flag | Why HMRC notices | How to avoid it |

|---|---|---|

| Late filings or late payments | Auto-flagged by HMRC’s filing systems | File on time, even nil returns |

| Errors or inconsistencies on your return | Cross-checked against PAYE, banks, platforms | Have your return reviewed before filing |

| Large year-on-year swings in income or costs | Flagged by Connect against sector benchmarks | Document the reason in your records |

| Expenses unusually high for your industry | Sector benchmarks compared automatically | Only claim genuinely allowable expenses — see allowable expenses for landlords |

| Income that doesn’t match lifestyle | Connect cross-references property, vehicles, social media | Make sure all income streams are declared |

| Offshore accounts or assets | Reported automatically under CRS/FATCA | Disclose worldwide income on your UK return |

| Property income (rental) | Cross-matched with Land Registry & council tax | Declare all rental income — get a rental income tax accountant |

| High-risk industries (cash trades, crypto, R&D) | Sector-level targeting | Keep contemporaneous evidence and clean records |

| Frequent or material amendments | Pattern flagged by HMRC’s risk engine | Only amend with clear documentation |

| Tip-offs from third parties | Triaged through HMRC’s fraud reporting | You can’t prevent — keep records that vindicate you |

A client unknowingly failed to declare rental income from a second property. HMRC discovered it through a combination of land registry and council tax data. They knew he wasn't living there and assumed — rightly — that it was being rented out.

He received a letter inviting him to disclose the income voluntarily. We went back through five years of records, calculated the unpaid tax, interest, and penalties, and submitted a full disclosure. HMRC accepted our offer, and the case was closed.

This case shows that HMRC has access to cross-government data, and rental income is a common red flag.

The 5 Stages of an HMRC Tax Investigation

An HMRC tax investigation follows five stages: (1) initial contact letter, (2) document submission, (3) detailed review and cross-check, (4) findings and penalty assessment, (5) closure, appeal or escalation. Most aspect enquiries resolve in 3–6 months; full investigations 9–16 months; fraud cases (COP9) often longer.

Knowing where you are in the process helps you respond appropriately and stops a routine compliance check turning into something worse.

- Initial contact and information request. HMRC sends a formal letter (occasionally a phone call) explaining what they want and asking for specific records, usually within 30 days. The scope of that letter tells you whether you’re facing an aspect enquiry (one part of your return) or a full enquiry (the entire return).

- Document submission and clarification. You or your accountant provide the records. HMRC may come back with clarification questions, ask for more documents, or request a meeting. How you handle this stage shapes everything that follows.

- Detailed review and technical assessment. HMRC analyses what you’ve sent, cross-checks it against third-party data, and forms a view on whether tax has been under-declared. This is where most of the work happens. Complex cases can take months.

- Findings, adjustments and penalty consideration. HMRC sets out its conclusions: whether tax is due, how much, and what penalty applies. Penalties depend on the behaviour involved (innocent error, careless, deliberate, or deliberate and concealed) and on whether you disclosed before HMRC asked or after.

- Closure, appeal or further recovery action. The case closes by formal notice, you settle any tax and penalty due, and the file is closed. If you disagree, you can request an internal review or appeal to the First-Tier Tax Tribunal. If HMRC suspects fraud, the case can escalate into a Code of Practice 9 (COP9) investigation under the Contractual Disclosure Facility.

Aspect enquiry vs full enquiry vs COP9

| Enquiry type | Scope | Typical length | Penalty risk |

|---|---|---|---|

| Aspect enquiry | One specific element of the return (e.g. an expense category) | 3–6 months | Low–medium |

| Full enquiry | Entire return or business records | 9–16 months | Medium–high |

| COP9 (Contractual Disclosure Facility) | Suspected deliberate behaviour or fraud | Often 12+ months | High; criminal prosecution avoided only with full disclosure |

How Far Back Can HMRC Go?

HMRC's look-back period depends on behaviour: 4 years for innocent errors, 6 years for careless errors, and up to 20 years for deliberate behaviour or fraud. The standard Self Assessment enquiry window is 12 months from the date you filed the return; after that, HMRC can still issue a discovery assessment reaching back to these limits.

| Type of error | Look-back period | Penalty band (% of tax) |

|---|---|---|

| Innocent error (you took reasonable care but got it wrong) | 4 years | 0% |

| Careless error (you didn’t take reasonable care) | 6 years | 0–30% (unprompted) / 15–30% (prompted) |

| Deliberate behaviour | 20 years | 20–70% |

| Deliberate and concealed | 20 years | 30–100% |

The standard self assessment enquiry window is 12 months from the date you filed the return. After that, HMRC can still issue a discovery assessment if it later finds tax that was under-declared and couldn’t reasonably have been spotted within those 12 months. Discovery assessments can reach back to the limits in the table.

We see discovery assessments opened on returns from five or six years ago all the time, usually because new information has surfaced. Undisclosed offshore interest reported under CRS, for example, or platform income flagged by Connect.

If you already know there’s an error in an earlier return, the safer route is almost always a voluntary disclosure to HMRC before HMRC contacts you. The penalty difference between an unprompted disclosure and a prompted one is large.

How HMRC Knows About Your Income & Assets

HMRC's Connect system pulls from over 30 data sources: UK banks and building societies (BBSI), overseas tax authorities (under the Common Reporting Standard and FATCA), real-time PAYE, Land Registry, Companies House, DVLA, council tax, digital platforms (eBay, Vinted, Airbnb, Etsy, Just Eat), and tip-offs. Anywhere the data points to income or gains not on your return, Connect flags the discrepancy.

The main sources in detail:

- Annual interest returns from UK banks and building societies (BBSI), which is how HMRC knows what savings interest you’ve earned without you telling them.

- Automatic Exchange of Information (AEOI/CRS/FATCA): overseas tax authorities share data on UK residents’ offshore accounts, including balances and interest.

- Real-time PAYE data: every payslip is reported to HMRC the moment it’s run.

- Land Registry, Companies House, DVLA and council tax records, used to cross-check property, directorships, vehicles and where you live.

- Digital platform reports from eBay, Vinted, Airbnb, Etsy, Just Eat and similar sites that now report seller income to HMRC each year.

- Credit reference and lifestyle data, used in personal expenditure reviews.

- Tip-offs from members of the public, ex-employees, ex-partners and competitors.

When the data HMRC holds points to income or capital gains that don’t appear on your return, the discrepancy gets flagged. That’s how it knows about undeclared income, savings interest and capital gains.

Can HMRC Check Your Bank Account?

Yes. Under Schedule 36 of the Finance Act 2008, HMRC can issue a Financial Institution Notice (FIN) requiring a bank to hand over records on a named taxpayer — without first needing approval from the tax tribunal. The same powers cover Monzo, Revolut, Starling, Wise and any other regulated UK or EEA financial institution. Overseas accounts are visible too, via Common Reporting Standard data sharing.

The rules tightened in 2021. The main tool is the Financial Institution Notice (FIN), introduced under Schedule 36 of the Finance Act 2008.

A FIN lets HMRC require a bank or financial institution to hand over records on a named taxpayer where the information is reasonably required to check that taxpayer’s position or collect a tax debt. HMRC no longer needs prior approval from the tax tribunal to issue one. Internal authorisation is enough. That makes FINs faster and more routine than the powers they replaced.

Can HMRC see my Monzo or Revolut account?

Yes. Monzo, Revolut, Starling, Wise and the other digital banks are regulated financial institutions, so the same FIN powers apply. There’s no loophole. A digital-only account is just as visible to HMRC as a Barclays current account.

What about joint accounts?

A FIN issued in your name can pull records from any account where you’re named as an account holder, including joint accounts with a spouse or business partner. The other person’s separate accounts aren’t in scope, but their data may be visible on the joint account statements.

What about closed accounts?

Banks usually keep transaction records for at least six years after closure, and HMRC can issue a FIN against a closed account within that period. Closing the account doesn’t erase the history.

What about overseas accounts?

Under the Common Reporting Standard (CRS), more than 100 jurisdictions share account-holder data with HMRC automatically each year: balances, interest, dividends and disposal proceeds. Overseas accounts haven’t been private from HMRC for a decade.

A FIN is different from an Account Freezing Order. AFOs are issued by the courts and used in criminal or recovery cases. A FIN gathers information. An AFO actually freezes the money.

HMRC’s Personal Expenditure Crackdown

A growing focus in compliance work is the personal expenditure review. HMRC is looking harder at personal spending that appears to be funded by undeclared business income, especially where directors of small limited companies are drawing more from their personal accounts than their declared salary and dividends would explain.

What triggers a personal expenditure review?

A review usually starts when HMRC sees lifestyle data (mortgage, vehicle finance, school fees, large credit-card balances, foreign property) that doesn’t line up with the income you’ve reported. Where HMRC can model a likely cost of living and compare it against declared income, an unexplained gap is one of the strongest signals it has of undeclared earnings. From there it goes straight to a compliance check or a full investigation.

What Are Common HMRC Pension Tax Errors?

The two mistakes HMRC flags most often are breaching the pension annual allowance, and taking money out of a pension without realising it triggers the Money Purchase Annual Allowance, which cuts how much can be paid in tax-efficiently afterwards. Both show up automatically because pension providers report contributions and withdrawals to HMRC directly. Higher earners are also more likely to be caught by the tapered annual allowance as income rises.

Self-employed people who mix personal and business spending, or who run informal payroll arrangements, are particularly exposed. If that’s you, planning your salary properly and keeping clean records is far cheaper than dealing with an enquiry after the fact.

HMRC Wage Raid & Payroll Compliance Checks

Compliance attention has shifted toward digital record-keeping ahead of the April 2026 Making Tax Digital deadline. HMRC is currently prioritising P11D accuracy and real-time payroll (RTI) data to find discrepancies between reported company profits and director withdrawals.

That has produced more targeted payroll checks. Some industry commentators call them “HMRC wage raid payroll checks”. Either way, payroll and benefits data is now examined as part of broader compliance work. National Minimum Wage compliance and Benefit-in-Kind reporting have become the main gateways for HMRC to launch wider business tax investigations. Inconsistent payroll or benefits reporting will trigger a compliance check.

Side Hustle & Vinted Data Sharing (One Year In)

By January 2026, HMRC has run its first full cycle of platform data from eBay, Vinted, Airbnb, Etsy, Just Eat and the rest. Connect flags discrepancies automatically.

The operating model has changed. HMRC isn’t waiting for taxpayers to come to it any more. It’s actively cross-referencing 2024/25 platform data against the Self Assessment returns just submitted in January 2026.

Does HMRC see my eBay / Vinted / Airbnb sales?

Yes. Under the OECD’s Digital Platform Reporting rules, UK and most international platforms now report seller income to HMRC each year. Where HMRC sees significant platform sales but no matching entry on your return, it cross-checks against bank receipts to verify whether the income actually arrived. Platform sales above the £1,000 trading allowance that weren’t declared will get a nudge letter or a formal enquiry.

Once HMRC knows what platform income you should have received, it can use a FIN to check whether the cash actually landed in your bank.

How Do HMRC Decide Who to Investigate?

Every return is run through Connect, which assigns a risk score based on how well the return matches external data HMRC already holds (bank interest, employer payroll, Land Registry, digital platforms, overseas tax authorities). High-scoring returns escalate to a human reviewer. Most don't.

The common triggers behind a high score are undeclared income, repeated late filings, expenses that look high for the sector, and patterns Connect flags as consistent with tax evasion. Tip-offs are triaged separately, but the same risk-scoring logic applies. Most reports never lead to an enquiry; the credible ones do.

Do HMRC Do Random Checks?

Yes — about 7% of HMRC investigations each year are random. They're uncommon, and HMRC won't turn up unannounced. You'll be contacted by phone or letter, asked for specific information, and given a window to respond. Respond on time. Silence is what turns a routine random check into something worse.

Random check vs triggered enquiry: what’s the difference?

| Random check | Triggered enquiry | |

|---|---|---|

| Share of cases | ~7% | ~93% |

| Cause | Statistical sample | Data mismatch, late filing, sector benchmark, tip-off |

| Scope | Usually narrow | Aspect or full |

| Predictable? | No — anyone can be picked | Yes — Connect signals are known |

| What to do | Reply on time, supply records requested | Same, plus get an accountant to read the letter first |

What Happens During an HMRC Tax Investigation?

It starts with a formal letter from HMRC setting out what they're reviewing — a specific part of your return, or your finances more broadly — and what records they want to see. The case ends one of three ways: no further action, an adjustment to the tax owed, or a penalty if errors are found.

Depending on the scope of the letter, HMRC may:

- ask for records (bank statements, sales records, VAT filings, payroll data, contracts) sent digitally or by post

- schedule a phone call or in-person meeting

- visit your business premises or, in some cases, your home

- interview you or your accountant about the accounts in question

The process can feel intrusive. Having clean documentation and a self assessment accountant on your side makes it considerably easier.

One of our clients had sold her business after 20 years and claimed Business Asset Disposal Relief on her tax return, saving a significant amount in tax by paying only 10%. About 12 years later, HMRC sent a compliance check letter asking for clarifications. We prepared a response with all documentation, answered follow-up questions, and the case was closed successfully with no penalties.

It's important to note this wasn't a full-blown investigation. HMRC didn't accuse her of wrongdoing — they just wanted to verify the claim. This is a good example of a compliance check that looked serious but was resolved smoothly.

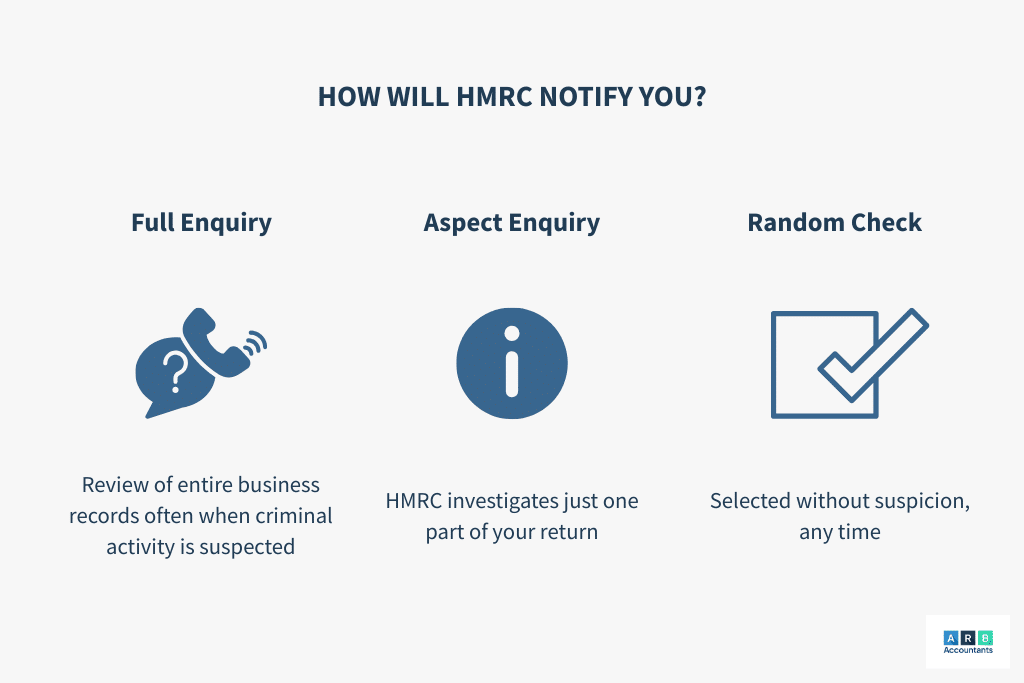

How Will I Know If HMRC Are Investigating Me?

HMRC won't turn up out of the blue. You'll be notified by phone or post when a case is opened. The letter or call either asks for specific information or simply tells you the enquiry is open. There are three types — full enquiry, aspect enquiry, or random check — and the wording of the letter usually tells you which one you've got.

There are three types of enquiry, and the wording of the letter usually tells you which one you’ve got:

- A full enquiry reviews your entire business records. HMRC opens one when it thinks there’s a significant risk of error in your tax, or when criminal activity is suspected.

- An aspect enquiry looks at one specific part of your accounts, such as a single expense category or income source.

- A random check is exactly that. Less common, and usually narrower in scope than a triggered enquiry.

If you’re not sure which you’ve been sent, an accountant can read the signal in seconds.

When Does HMRC Investigate the Self-Employed?

Many self-employed taxpayers handle their own returns. That makes innocent errors more likely, and innocent errors look like red flags to Connect. HMRC typically investigates self-employed individuals when it sees:

- Inconsistencies in reported earnings year on year

- Expenses that look high for the sector

- Late or missing tax filings

- A mismatch between declared income and lifestyle indicators

- Undeclared income from digital platforms

Freelancers, tradespeople and cash-based businesses are particularly exposed. Working with accountants for contractors and keeping clean digital records is the single biggest reduction in risk you can make.

How Long Does an HMRC Investigation Take?

It depends on scope: aspect enquiries 3–6 months, full investigations 9–16 months (sometimes longer), COP9 fraud investigations a year or more. The biggest single variable is response speed: delays in providing records consistently stretch the timeline and worsen the outcome.

Drift and delay are what turn a short enquiry into a long one. Responding promptly with complete information is the single biggest lever you have over the timeline.

What Happens When You Report Someone to HMRC?

If you’ve reported someone for tax evasion, the report goes through HMRC’s fraud reporting system. It gets risk-scored, cross-referenced against existing data, and a decision is made on whether to act.

Most reports either go nowhere (insufficient evidence) or feed into an existing intelligence picture without producing a visible enquiry. Where a report does prompt action, it can lead to a compliance check, a nudge letter, or a full investigation. The reporter is never told what happened. The process is confidential by law.

You can report tax evasion online or via HMRC’s Fraud Hotline, anonymously if you want.

MTD for ITSA: One Trigger to Watch in 2026

From 6 April 2026, sole traders and landlords with qualifying income above £50,000 must comply with Making Tax Digital for Income Tax: digital records, compatible software, and quarterly updates. HMRC has confirmed that not signing up for MTD-compatible software is now a high-priority risk indicator and can itself trigger a compliance check. For a full breakdown of the rules, deadlines and exemptions, see our guide to MTD for ITSA.

How to Reduce Your Chances of an HMRC Investigation

Random checks happen, but most investigations are triggered by inconsistencies, late filings, or unusual patterns. To lower your odds:

- Keep your records clean and consistent. Cloud accounting tools make this easier than spreadsheets ever did.

- Declare every income stream: rental, freelance, dividends, savings interest, platform sales.

- Stay on top of the rules for your sector. Sector-specific risks are where HMRC focuses.

- Only claim deductions HMRC permits for your trade. Avoid the borderline ones.

- File on time. Late filings are the single most common avoidable trigger.

- Get your return reviewed by an accountant before you submit. Even if you do your own bookkeeping, a fresh pair of eyes catches red flags before HMRC does.

The rising cost of being wrong

As of January 2026, HMRC’s late payment interest rate sits at 7.75% (set at Bank of England base rate plus 4%, which has applied since 6 April 2025; the previous formula was base rate plus 2.5%). Still close to triple the 2022 rate. Penalties for careless or deliberate errors stack on top, scaled to the behaviour involved and to whether you disclosed before HMRC asked or after.

Your chances of being investigated come down to how accurate and transparent your tax submissions are. Getting it right at the front end is far cheaper than fixing it during an enquiry.

One client had a PAYE job and some rental income, so we submitted a self-assessment. He forgot to mention that he had an outstanding student loan, so it wasn't included in the return.

HMRC noticed the omission and sent a letter. We replied, explaining it was a genuine oversight, and because it was his first error, they allowed us to correct it without penalties.

These types of cases are surprisingly common — people forget to tick the student loan box or assume their employer has handled it. It's a simple mistake, but still triggers inquiries.

Get Expert Help with an HMRC Investigation

ARB Accountants offers a full tax investigation accountant service for individuals and businesses facing HMRC enquiries, from a single aspect enquiry to a full investigation or COP9 case.

We read the letter. We work out what HMRC is really looking at. We prepare the response and supporting evidence, handle correspondence on your behalf, and negotiate any settlement or penalty position. The earlier we get involved, the better the outcome usually is.

Speak to a tax investigation specialist today.

Free 60-minute consultation. ACCA-chartered. Handling HMRC enquiries since 2008.

"ARB Accountants helped me resolve an issue with HMRC that had been dragging on for months. Their knowledge and persistence saved me a lot of stress — and money. I can't recommend them enough." Jay Sach · Google Review (Tax Audit)

Frequently Asked Questions

Can HMRC investigate past tax years?

Yes. HMRC can reopen tax years from the past. For innocent errors they typically go back four years, six years for careless mistakes, and up to 20 years where deliberate behaviour or fraud is suspected. The further back HMRC reaches, the higher the bar of evidence they need.

How do I know if HMRC are investigating me for undeclared income?

HMRC will not turn up unannounced. You will normally receive a letter (sometimes a 'nudge letter') or a phone call asking for specific records or explanations. Requests focused on a particular bank account, a property, a digital platform like eBay or Vinted, or overseas income are strong signals that HMRC has matched outside data against your return.

What triggers an HMRC investigation for high-income individuals?

Complex tax structures, offshore accounts, multiple income streams, large unexplained increases in wealth, and inconsistencies between lifestyle and declared income. HMRC's Wealthy and Mid-Sized Business Compliance team also runs targeted reviews of higher-income taxpayers.

When does HMRC investigate self-employed individuals in cash-based businesses?

Cash-based trades — taxis, market traders, hospitality, construction, beauty — are higher-risk because income is harder to verify. HMRC compares your reported turnover to industry benchmarks, supplier records, card-payment data, and lifestyle indicators. Sustained margins out of line with the sector often trigger a review.

How do HMRC decide who to investigate in cases of property income?

HMRC cross-references Land Registry data, council tax records, and lender data with your tax return. If you own a property where you do not live and no rental income appears on your return, that mismatch can prompt a Let Property Campaign letter or a formal enquiry.

What are the chances of being investigated by HMRC if you frequently amend tax returns?

Occasional corrections are normal. Repeated amendments — especially ones that materially change taxable income — can flag your record as higher risk. Multiple amendments in the same year almost always invite a closer look.

What are the red flags for HMRC?

Late filings, unexplained income jumps or drops, unusually high expenses for the sector, undeclared rental or platform income, large cash deposits, frequent amendments, and any mismatch between data HMRC already holds (banks, employers, platforms, Land Registry) and what is on your return.

How can I reduce my chances of an HMRC investigation?

Keep accurate digital records, declare all income (including side hustles and savings interest), file on time, only claim allowable expenses, and have your return reviewed by an accountant. Consistency between years — and between your return and the data HMRC already holds — is the strongest defence.

Can you report someone to HMRC anonymously?

Yes. HMRC's online fraud reporting form and the Fraud Hotline both allow anonymous reports. You will not be told what HMRC does with the information, and most reports are screened and risk-scored before any action is taken.

How do HMRC investigate tax evasion?

HMRC uses a data-matching system called Connect to cross-reference tax returns against bank records, Land Registry data, employer payroll, digital platform reports, and even social media. Where Connect flags a discrepancy, a compliance check or fraud investigation may follow.

How far back can HMRC go?

Four years for innocent mistakes, six years for careless errors, and up to 20 years if HMRC suspects deliberate evasion. The standard self assessment enquiry window is 12 months from the date the return is filed, but discovery assessments can reach back much further.

Can HMRC check your bank account?

Yes. Under Schedule 36 of the Finance Act 2008, HMRC can issue a Financial Institution Notice (FIN) to require a bank to hand over records on a named taxpayer, without first needing tax tribunal approval, where the information is reasonably required to check that taxpayer's position.

How far can the taxman go back?

Four years is the standard window for routine checks. The taxman can reopen cases from up to 20 years ago where there is evidence of deliberate concealment of income or assets.

What happens if HMRC investigate you?

You will receive an official letter or phone call setting out what HMRC wants to see. The process can range from a single information request (an 'aspect enquiry') to a full review of your business records. The case may close with no action, an adjustment to your tax, or penalties depending on what HMRC finds.

How do HMRC find out about undeclared income?

Automatic data feeds from banks, employers, pension providers, overseas tax authorities (under CRS and FATCA), digital platforms (eBay, Vinted, Airbnb), Land Registry, and tip-offs from members of the public. HMRC's Connect system pulls these together and flags where reported income falls short.

What happens when you report someone to HMRC?

HMRC triages the report through its fraud reporting system, scores it for risk, and decides whether the intelligence merits a compliance check or a full investigation. The reporter is not updated on case progress and the process is confidential.

Can HMRC see my Monzo or Revolut account?

Yes. Monzo, Revolut, Starling, Wise, and other digital banks are regulated UK or EEA financial institutions. HMRC can issue a Financial Institution Notice to obtain records from any of them in the same way it would from a high-street bank.

What is HMRC Connect?

Connect is HMRC's data-matching and analytics system. It pulls together information from over 30 sources — banks, employers, Land Registry, DVLA, overseas tax authorities, digital platforms — and flags discrepancies between what taxpayers report and what other parties have reported about them.

How does HMRC know about my savings interest?

UK banks and building societies submit annual Bank and Building Society Interest (BBSI) returns to HMRC, which detail interest paid to each customer. HMRC also receives offshore interest data automatically under the Common Reporting Standard (CRS), so foreign savings accounts are no longer hidden.

What is a Financial Institution Notice (FIN)?

A FIN is a power introduced in 2021 under Schedule 36 of the Finance Act 2008. It lets HMRC require a bank or financial institution to provide records on a named taxpayer where the information is reasonably required to check that taxpayer's position or collect a tax debt — without first having to obtain approval from the tax tribunal.

What is Code of Practice 9 (COP9)?

COP9 is HMRC's fraud-investigation procedure under the Contractual Disclosure Facility, used where HMRC suspects deliberate behaviour. Recipients are invited to make a full disclosure of all deliberate conduct in return for protection from criminal prosecution. The standard COP9 disclosure timetable is 60 days, after which a detailed Outline Disclosure is followed by a Full Disclosure Report.

What is a Discovery Assessment?

A discovery assessment is a retrospective HMRC assessment raised after the standard 12-month enquiry window has closed. HMRC can issue one where tax has been under-declared and the omission could not reasonably have been spotted within the enquiry window. Discovery assessments can reach back 4 years (innocent), 6 years (careless) or 20 years (deliberate).

What's the difference between a compliance check and a tax investigation?

A compliance check is a routine review of part of your tax position — often a single aspect like one expense category. A tax investigation (sometimes a 'full enquiry') is broader, longer, and more invasive, looking at the whole of your return or business records. Compliance checks can escalate into investigations if HMRC finds something significant.

Will HMRC investigate me if I'm a sole trader?

Sole traders are not exempt — quite the opposite. HMRC actively reviews sole-trader returns where margins, expenses, or turnover look out of line with the sector, where digital platform income hasn't been declared, or where filings are repeatedly late. Cash-based sole traders are a particular focus.

How does HMRC find out about undeclared rental income?

HMRC matches Land Registry ownership records and council tax data against tax returns. Where it finds someone owns a property they don't live in, and no rental income appears on their return, it issues a Let Property Campaign letter inviting voluntary disclosure before opening a formal enquiry.

Does HMRC investigate inheritance tax returns?

Yes. HMRC opens compliance checks on IHT400 forms where the estate's declared value looks low against Land Registry, share registry or bank data it already holds. The most common triggers are property undervaluation, gifts made in the seven years before death that weren't declared, and estates claiming reliefs such as Business Property Relief or Agricultural Property Relief without supporting paperwork. Executors are personally liable for errors on the IHT400, so it's worth having the valuation and any lifetime gifts checked before submission.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008