MTD for ITSA 2026: Who's In Scope, Deadlines & What to Do

Free · 30 seconds · No email needed to see your answer

Are you in MTD for ITSA — and when do you start?

Answer two quick questions to see whether the rules apply to you, your mandatory start date, and the first deadline you need to hit.

Your answer

Based on the current MTD for ITSA timetable and your answers. The threshold is tested on gross income from your last full tax year, so if you are near a cut-off it is worth confirming.

Want your start date confirmed and the setup handled?

Book a free, no-obligation call. We'll confirm exactly where you stand, register you, and set up the right software so the next deadline is one less thing to worry about.

How is this worked out?

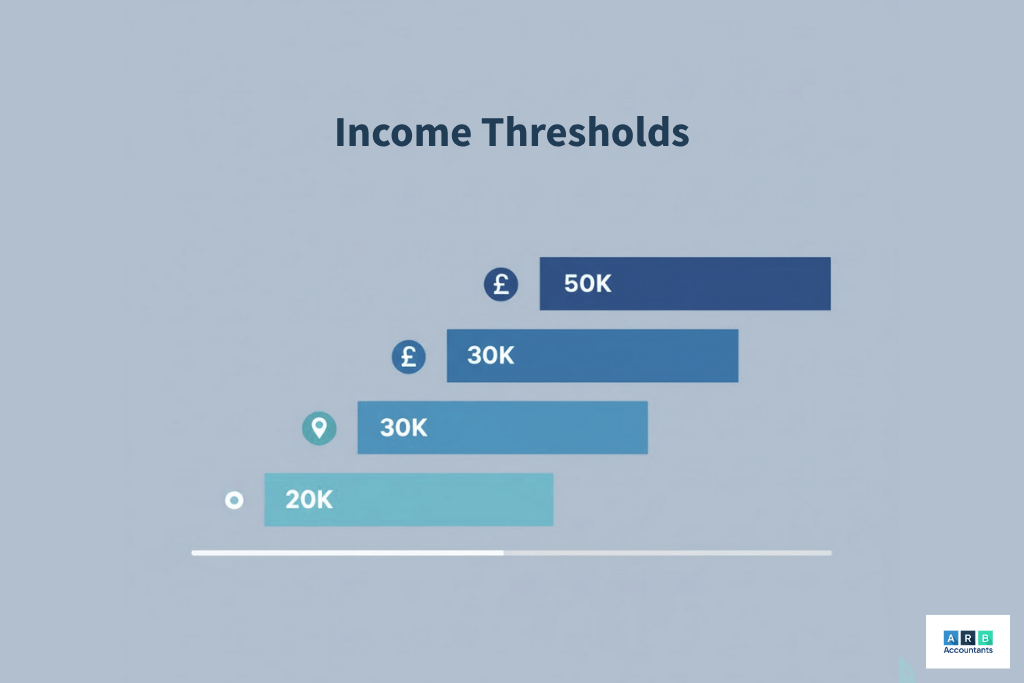

MTD for ITSA is phased in by gross qualifying income: over £50,000 from 6 April 2026, over £30,000 from 6 April 2027, and over £20,000 from 6 April 2028 (the £20k stage was confirmed at the Spring Statement 2025). It covers self-employment and property income only.

It is a guide, not formal advice — the threshold uses gross income from your last full tax year, and joint property and multiple trades have their own rules.

If you’ve had a letter from HMRC about MTD for ITSA, missed the April 2026 start date, or you’re not sure whether the £50k threshold even catches you — you’re not the only one. MTD for ITSA went live on 6 April 2026 for sole traders and landlords with gross income over £50,000, and there’s still time to get compliant if you act now. The first quarterly deadline is 7 August. Book a free 20-minute call and we’ll tell you exactly where you stand and what to do next.

This guide covers who’s affected by the MTD for ITSA rules, the exact quarterly submission dates, what software you’ll need, and how to catch up if you’ve not started yet. We’ll also walk through exemptions, the penalty regime, and practical steps to get your record-keeping right before the next deadline. If you’d rather skip the reading, our self-assessment service handles the whole quarterly cycle for you.

Table Of Contents

- Who Must Follow MTD for ITSA From April 2026?

- MTD for ITSA Income Thresholds and Qualifying Income

- MTD for ITSA Start Date and Key Deadlines

- MTD for ITSA Requirements: Digital Records and Compatible Software

- Step By Step Filing Process Under MTD for ITSA

- Exemptions and How to Apply

- Penalties for Late or Incorrect MTD for ITSA Submissions

- What MTD for ITSA Means for Sole Traders and Landlords

- Frequently Asked Questions

Who Must Follow MTD for ITSA From April 2026?

MTD for ITSA is mandatory from 6 April 2026 for sole traders and landlords whose gross income from self-employment and property is over £50,000. The threshold drops to £30,000 from April 2027 and £20,000 from April 2028.

Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) becomes mandatory from 6 April 2026 for sole traders and landlords whose qualifying income exceeds £50,000 in the 2024–25 tax year. This marks the initial MTD ITSA start date. The regime replaces the traditional annual Self Assessment process with quarterly digital reporting through compatible software.

HMRC rolls out the MTD requirements in phases based on income thresholds. If your gross business or property income crosses the threshold, you’ll submit four quarterly updates each year plus a final declaration, all through approved software that connects directly to HMRC.

Sole Traders Over £50k Annual Turnover

If your gross trading income from self-employment exceeds £50,000, you’re in scope from April 2026. HMRC measures this using total receipts before deducting any expenses, so even if your net profit sits well below £50,000, you’re still caught if your turnover crosses that line. You must meet the MTD requirements for digital record keeping.

Multiple sole-trade businesses get combined for the threshold test. A consultancy bringing in £30,000 and a separate retail business generating £25,000 puts you over the limit, even though neither individually hits £50,000.

Landlords With Gross Rents Above £50k

Landlords receiving more than £50,000 in gross rental income from UK properties face the same April 2026 start date. The test uses total rents received before deducting mortgage interest, repairs, or other allowable expenses.

Joint property owners calculate their individual share of gross rents. If you own three properties 50/50 with a partner and the total gross rents come to £80,000, your personal share is £40,000 — below the threshold. However, for those above the limit, the rules apply in full from 6 April 2026.

Phased Entry for the £30k to £50k Band

The MTD for ITSA regime expands from 6 April 2027 to capture income between £30,000 and £50,000. A further extension to £20,000 was confirmed at the Spring Statement 2025 and starts on 6 April 2028, bringing roughly an extra 970,000 sole traders and landlords into scope.

MTD for ITSA Income Thresholds and Qualifying Income

The threshold uses your gross income (before expenses), adding self-employment and property income together, from your most recent complete tax year. A business with £60,000 turnover but only £15,000 profit is still in scope, because the gross figure is what counts.

HMRC assesses the £50,000 threshold using your most recent complete tax year’s figures, based on gross income before expenses. Getting this calculation right determines whether you’re in scope and when you start.

The focus on gross income rather than taxable profit catches many people by surprise. A business with £60,000 turnover but only £15,000 profit after expenses still falls into MTD for ITSA because the gross figure triggers the requirement.

Trading Income Calculation

Include all business receipts before any cost of sales, overheads, or capital allowances. Commission, fees, and other trading receipts count toward the threshold regardless of whether you’ve actually collected payment by year end.

Accruals basis traders include invoiced amounts. Cash basis traders include amounts received. Either way, you’re measuring total gross receipts from your business activities.

Property Income Calculation

Use total gross rents received or due before deductions like mortgage interest, insurance, or maintenance costs. For jointly owned property, each owner uses their share of the gross rents to determine if they individually meet the threshold for MTD for ITSA.

Property owned through a partnership doesn’t count toward your personal MTD threshold until partnerships are brought into scope separately. Keep business property income distinct from any property held in a corporate structure.

Mixed Income Scenarios

For threshold testing, add your qualifying gross trading income and your qualifying gross property income together. If the combined total exceeds £50,000, you’re in scope from April 2026, even if neither source individually crosses the line. This combined total determines your MTD for ITSA start date.

Other income types don’t count toward the MTD threshold:

-

Employment income

-

Pension income

-

Dividends

-

Savings interest

The regime currently applies only to business and property income reported through Self Assessment.

MTD for ITSA Start Date and Key Deadlines

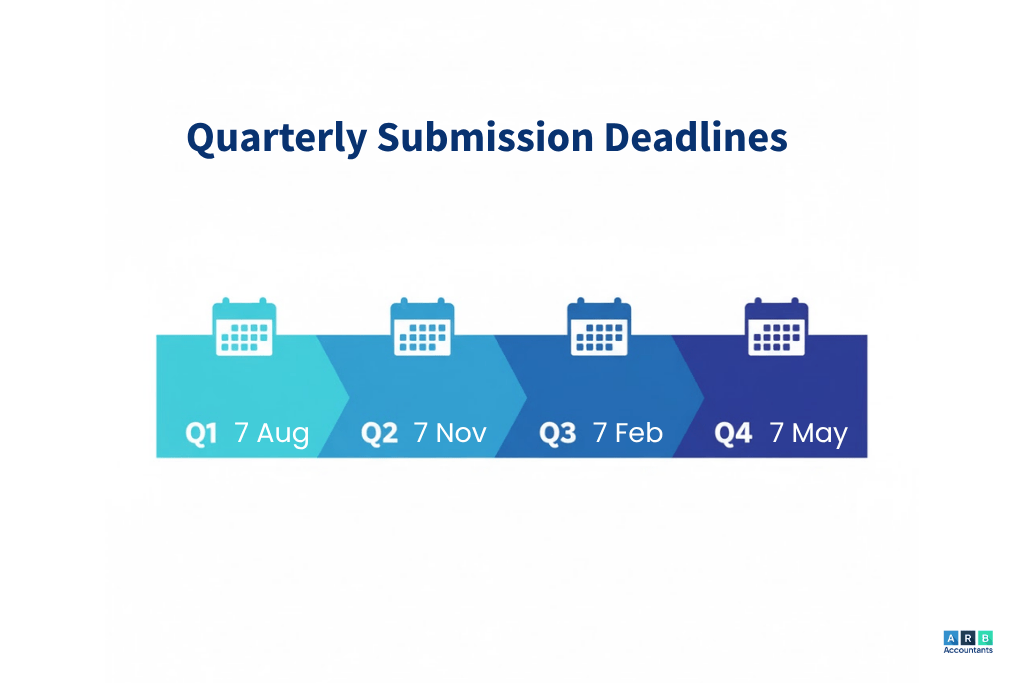

In-scope taxpayers send four quarterly updates plus a year-end Final Declaration, instead of one annual return. The 2026/27 quarterly deadlines are 7 August, 7 November, 7 February and 7 May, with the Final Declaration due by 31 January 2028.

Quarterly updates replace the annual Self Assessment return for in-scope income, with four submissions during the tax year followed by a year-end final declaration. Each update summarises your income and expenses for that three-month period.

The deadlines fall roughly one month after each quarter ends. Missing these dates triggers penalty points under HMRC’s new regime, so building reliable processes matters from the start.

| Quarter | Period Covered | Submission Deadline |

|---|---|---|

| Q1 | 6 Apr – 5 Jul | 7 Aug |

| Q2 | 6 Jul – 5 Oct | 7 Nov |

| Q3 | 6 Oct – 5 Jan | 7 Feb |

| Q4 | 6 Jan – 5 Apr | 7 May |

| Final Declaration | Whole tax year | 31 Jan (following year) |

The first quarter runs from 6 April to 5 July, with the update due by 7 August. This first submission is critical after the MTD ITSA start date. You’ll submit a summary of income received and expenses incurred during those three months through your MTD-compatible software.

The figures don’t get finalised or adjusted at this stage, quarterly updates focus on in-year reporting rather than final calculations. If you spot an error in Quarter 1, you can correct it in the Quarter 2 submission without penalty, provided you act promptly.

The second quarter covers 6 July to 5 October, due by 7 November. By this point, you’re halfway through the tax year and building a clearer picture of your annual position.

Quarter 3 runs from 6 October to 5 January, with a deadline of 7 February. This quarter often includes Christmas trading periods for many businesses, plus year-end property income for calendar-aligned landlords.

The final quarter covers 6 January to 5 April, completing the tax year. The 7 May deadline gives you one month after the year end to prepare your fourth quarterly update.

After submitting all four quarterly updates, you prepare a single Final Declaration by 31 January following the tax year. This replaces the traditional Self Assessment return and crystallises your tax position for the year, including any adjustments, reliefs, capital allowances, and other items not captured in the quarterly updates. (The previously-proposed End of Period Statement was removed by HMRC ahead of MTD for ITSA going live, so there’s only one year-end submission to deal with — the Final Declaration.)

Confused about which deadline applies to you?

Book a free 20-minute call and we'll work out exactly when your first MTD for ITSA submission is due and what to file.

MTD for ITSA Requirements: Digital Records and Compatible Software

MTD for ITSA requires digital records and functional compatible software that maintains digital links and submits updates directly to HMRC. Manual-only spreadsheets fall short unless you connect them through approved bridging software.

The software handles three core functions: maintaining digital records of income and expenses, preserving those records in digital format, and transmitting quarterly updates and final declarations to HMRC via API.

Transaction Level Data to Capture

Record all income receipts, allowable expenses, and VAT where applicable at transaction level. Each transaction needs a date, description, amount, and appropriate category to satisfy HMRC’s MTD requirements.

You don’t have to scan and digitally store every paper receipt, though many businesses find it helpful. The critical requirement is that each transaction gets recorded digitally in your software, with sufficient detail to support your tax position if HMRC enquires later.

Bridging Software Options

You can connect spreadsheets to HMRC through approved bridging software as a transitional solution. The bridging software reads your spreadsheet data and formats it for HMRC’s systems, letting you maintain your existing workflow while meeting the digital submission requirement.

This approach introduces potential technical risks, broken links, version conflicts, or data mismatches that fully integrated solutions avoid. Bridging works best as a short-term stepping stone rather than a permanent arrangement for MTD for ITSA.

Native Cloud Platforms Like Xero and QuickBooks

Cloud accounting platforms with full MTD capabilities provide integrated workflows, automatic bank feeds, and fewer technical risks than bridged solutions. The platforms handle record-keeping, quarterly submissions, and final declarations within a single environment.

ARB Accountants maintains certified partnerships with both Xero and QuickBooks, offering streamlined setup, training, and ongoing support tailored to MTD for ITSA requirements. Choosing the right platform from the start saves time and reduces compliance risk as the regime matures.

Step By Step Filing Process Under MTD for ITSA

Following a structured path from registration through quarterly submissions to year-end declarations keeps you compliant and reduces the risk of penalties or errors. Each step builds on the previous one.

The process might feel unfamiliar at first, particularly if you’re used to gathering records once a year for your accountant. MTD for ITSA shifts the rhythm to quarterly engagement, which actually helps many businesses maintain better financial oversight throughout the year.

Sign Up With HMRC

Create or use your existing Government Gateway account and enrol for the MTD for ITSA service before your first mandatory quarterly deadline. HMRC’s online portal walks you through the registration process, which typically takes 10–15 minutes if you have your details ready.

You’ll receive a confirmation and unique identifiers that your software uses to link to your HMRC account. Keep these credentials secure, they’re the gateway to all your future submissions under MTD for ITSA.

Connect Approved Software

Choose HMRC-recognised software from the official compatibility list and authorise it to interact with your HMRC account. The software will prompt you through the authorisation process, which creates a secure connection between your records and HMRC’s systems.

Once connected, your software can retrieve obligations, submit updates, and receive acknowledgements automatically.

Submit Quarterly Updates

Upload your income and expense data through the software each quarter, summarising the three months’ activity. The software formats the data to HMRC’s specifications and transmits it via API, giving you an instant confirmation receipt.

You’re not required to include final adjustments, capital allowances, or reliefs at this stage. Quarterly updates focus on in-year income and expenses; the detailed year-end calculations all belong on the Final Declaration.

Review your year-end position

At year end, review the software-generated summary of your four quarterly updates plus HMRC’s calculations. (HMRC originally planned a separate “End of Period Statement” between the quarterly updates and the Final Declaration, but removed it before mandation — so you go straight from quarterly summary to Final Declaration.)

Take time to review carefully, this is your opportunity to spot and correct any discrepancies before finalising. Your accountant can help verify that all reliefs and allowances have been claimed and that the figures match your actual position.

File Final Declaration

Confirm all figures are complete and accurate, then submit the final declaration by 31 January following the tax year. This last step is the culmination of the MTD for ITSA process. Once submitted, you’ll receive a calculation showing your total tax liability, payments on account, and any balance due.

Ready to simplify your MTD for ITSA transition? Get your free MTD for ITSA readiness consultation and discover how ARB Accountants can handle your quarterly submissions, software setup, and compliance monitoring with fixed-fee transparency.

Exemptions and How to Apply

Only limited exemptions exist, and you’re required to apply and receive HMRC approval before relying on one. The bar for exemption sits high, HMRC expects most taxpayers to comply digitally with MTD for ITSA.

If you believe you qualify, apply as early as possible. HMRC reviews each case individually, and processing can take several weeks, particularly as the April 2026 deadline for MTD for ITSA approaches.

Digital Exclusion Claims

If age, disability, or lack of internet access due to remote location prevents digital engagement, you can apply with supporting evidence. HMRC considers factors like availability of assisted digital support, access to public internet facilities, and whether reasonable adjustments would enable compliance with MTD for ITSA.

The exemption isn’t automatic, you make a clear case and provide evidence. If granted, you’ll continue filing on paper, but HMRC may review your circumstances periodically.

Religious Objection Route

If your religious beliefs prevent you from using electronic systems, you can apply for exemption. HMRC will want to understand the specific religious principles at stake and why no workaround exists.

Few applications succeed on religious grounds alone, particularly where the objection relates to general technology use rather than specific theological concerns.

Income Below £30k After 2027

When does MTD for self assessment start for those in the lower band? The threshold reduces to £30,000 in April 2027 and to £20,000 in April 2028 (the £20k figure was confirmed at the Spring Statement 2025). Those below the new threshold fall out of scope and can revert to traditional Self Assessment. If you’ve already joined MTD for ITSA voluntarily or were previously mandated, you’ll formally exit the regime.

Consider your projected income trajectory when planning. If you’re hovering around the threshold, joining voluntarily at a convenient time may make more sense than waiting for a mandatory start during a busy trading period.

Penalties for Late or Incorrect MTD for ITSA Submissions

MTD for ITSA introduces a points-based late submission regime alongside existing penalties for inaccuracies and late payment. The new system aims to encourage consistent compliance while allowing for occasional genuine mistakes without immediate financial penalty. This penalty regime is part of the MTD requirements.

The system is less forgiving than the old Self Assessment regime, where you could often file a few days late without immediate consequence.

Points System Overview

Each late quarterly update earns one penalty point. Once you accumulate the threshold (four points for MTD for ITSA quarterly obligations), HMRC issues a financial penalty and your points total resets. Important for the first year: HMRC has confirmed a soft landing for 2026/27 — no penalty points are issued for late quarterly updates during the first MTD for ITSA tax year. Late payment penalties and the Final Declaration deadline still apply in full from day one.

Points expire after a period of compliant behaviour if you submit on time consistently, earlier points drop off your record. This rewards getting back on track after a slip.

Financial Penalty Triggers

Fixed monetary penalties of £200 apply once you reach the points threshold, with additional penalties for continued non-compliance. Late payment of tax attracts its own penalty and interest regime, distinct from late filing penalties. MTD for ITSA requires both timely filing and payment.

You can file on time but still face late payment penalties if you don’t settle your tax bill when due.

Appeal Process

You can appeal penalties if you have a reasonable excuse, serious illness, bereavement, technology failure beyond your control, or other circumstances that prevented timely compliance. Submit appeals within HMRC’s time limits (typically 30 days) and provide evidence supporting your position.

HMRC considers each appeal on its merits. Vague explanations or simple forgetfulness rarely succeed, but genuine unforeseen circumstances often do.

What MTD for ITSA Means for Sole Traders and Landlords

Two groups carry most of the weight under the MTD for ITSA regime in 2026: self-employed sole traders and individual landlords. The mechanics of the rules are the same for both, but the practical pain points are different.

Sole traders

If you run more than one trade — say a consultancy plus a small e-commerce shop — HMRC adds the gross income from each together for the £50,000 test. £30k from one and £25k from the other puts you in scope, even though neither business individually crosses the line. The same combined figure also drives your quarterly submission once you’re in.

CIS subcontractors need particular care. Your gross CIS earnings (before the 20% or 30% deduction at source) count toward the threshold, not the net amount you actually receive. Plenty of subcontractors who think they’re under £50k discover they’re not once the gross figure is checked. The CIS deductions then come through as tax already paid against your annual liability, but they don’t reduce your turnover for MTD purposes.

For tradespeople, software choice matters as much as the numbers. The cleanest options for one-person trades are FreeAgent (free with most NatWest, Royal Bank of Scotland, Ulster Bank and Mettle business accounts), Xero, or QuickBooks Self-Employed. All three have working MTD for ITSA submission features, mobile receipt capture, and can be set up in under an hour. If you already have an accountant, ask which they support — running on a platform your accountant doesn’t use creates needless friction every quarter.

If this is starting to feel like more than you want to handle alone, our sole trader accountants cover the full quarterly cycle on a fixed monthly fee.

Landlords

For jointly-owned properties, only your share of gross rents counts toward your personal £50,000 test. A married couple owning three flats 50/50 with combined gross rents of £80,000 each report £40,000 — both below the threshold. But change the split to 70/30 and the higher-share owner crosses the line on their own. Keep the ownership split documented in writing so HMRC can see how the figures were arrived at.

Quarterly record-keeping for rental income is more granular than most landlords are used to. You’re recording every rent receipt by date, every repair invoice with VAT broken out, every mortgage interest statement, and every letting-agent fee — three months at a time, four times a year, in software that connects to HMRC. Most landlords get away with a paper folder and a January spreadsheet sprint today; under MTD for ITSA that approach stops working.

The Renters’ Rights Act has changed the rhythm of rental income too. With periodic tenancies replacing fixed-term ASTs, void periods are harder to predict and rent reviews now follow a stricter formal process. That makes income lumpier across quarters, which means the quarterly figures you report under MTD for ITSA will look more variable than the annual numbers ever did. HMRC’s risk system reads consistency as a positive signal — sudden drops or spikes can prompt a Let Property Campaign letter, so it’s worth being able to explain each quarter’s movement.

For the practical side, see our guide to bookkeeping for landlords, or hand the whole thing to our landlord accountants and let us run the quarterly cycle for you.

Frequently Asked Questions

When does MTD for ITSA start?

MTD for ITSA started on 6 April 2026 for sole traders and landlords with gross income over £50,000 in the 2024–25 tax year. The threshold drops to £30,000 from April 2027 and to £20,000 from April 2028 (the £20k extension was confirmed at the Spring Statement 2025). The first quarterly submission deadline under the 2026 rules is 7 August 2026.

How do I correct an error in a previous quarterly update?

Submit an amended update through your software as soon as you spot the error and before the next relevant deadline. HMRC’s systems accept prompt corrections without penalty, treating them as part of the normal quarterly cycle rather than formal amendments. If the error is material and surfaces after a deadline, our self-assessment service team can advise on the disclosure route.

Can I still use spreadsheets if I attach bridging software?

Yes, bridging software connects spreadsheets to HMRC’s systems and satisfies the technical MTD for ITSA requirements. Fully native cloud solutions like Xero or QuickBooks typically reduce errors, eliminate technical integration issues, and streamline your compliance workflow more effectively than bridged spreadsheets — but bridging is a valid stepping stone for taxpayers transitioning from a long-running spreadsheet system.

Will partnerships definitely start MTD in 2027?

HMRC has signalled a 2027 start date for partnerships with income above the threshold, but enabling legislation hasn’t yet been finalised. Partnerships are not in scope of the 2026 MTD for ITSA rules, so general partnerships can continue with annual Self Assessment for now while monitoring HMRC announcements.

Do I need separate software for each property business?

One software subscription usually manages multiple property businesses under a single taxpayer, using separate business identifiers within the platform to distinguish different activities. Most MTD for ITSA-compatible platforms support this without an additional fee.

When does MTD for landlords start if their total rental income is over £30,000?

Landlords whose combined gross income (rental plus any self-employment) is over £30,000 but up to £50,000 enter MTD for ITSA from 6 April 2027. Until then, those landlords continue with the traditional annual Self Assessment route.

What are the main MTD for ITSA requirements for those in scope?

The main MTD for ITSA requirements are to keep digital records of your income and expenses using MTD-compatible software and to send quarterly summaries to HMRC, plus a single Final Declaration by 31 January each year. (The originally-proposed End of Period Statement was removed by HMRC before MTD for ITSA went live, so there’s only one year-end submission, not two.) There’s no requirement to scan every paper receipt, but every transaction must exist as a digital record with a date, description, amount and category.

What is the MTD for ITSA start date for those with income between £20,000 and £30,000?

The mandatory MTD for ITSA start date for taxpayers with annual gross income over £20,000 and up to £30,000 is 6 April 2028, confirmed by the government at the Spring Statement 2025.

If I have both self-employment and property income, how is the MTD for ITSA threshold determined?

The threshold is based on your total gross income from both self-employment and UK/foreign property combined. If the combined total is over the relevant threshold (£50,000 for 2026, £30,000 for 2027), you’re in scope for MTD for ITSA — even if neither source individually crosses the line.

Will I have to pay tax every quarter under MTD for ITSA?

No. The payment deadlines for your tax bill (usually 31 January for the balancing payment, plus 31 January and 31 July payments on account) are not changing under MTD for ITSA. The quarterly updates are reporting-only — no tax becomes payable each quarter.

What happens if I miss a quarterly MTD for ITSA deadline?

HMRC operates a points-based penalty system. You receive one point for each missed quarterly submission, and reaching the threshold (four points for MTD for ITSA quarterly obligations) triggers a £200 financial penalty. HMRC has confirmed a soft landing for 2026/27, so no points are issued for late quarterly updates during the first MTD for ITSA tax year — but this concession does not cover the Final Declaration deadline or late payment penalties. Points expire after a period of compliant submissions, so getting back on track promptly resets your record.

Do I still need to submit a full Self Assessment tax return after MTD for ITSA starts?

No. For income covered by MTD for ITSA, the annual Self Assessment return is replaced by the Final Declaration submitted via your MTD-compatible software. (HMRC removed the previously-proposed End of Period Statement before mandation, so there’s only one year-end submission to deal with.) Other income types — dividends, savings interest, capital gains — are added on the Final Declaration alongside your business income, so you don’t file a separate Self Assessment as well.

Missed the April deadline? You still have options.

HMRC has confirmed a soft landing for 2026/27 — no penalty points for late quarterly updates during the first MTD for ITSA tax year (late payment penalties and the Final Declaration deadline are not covered). You still need to be set up, registered and keeping digital records — so acting now matters. We'll register you, set up the right software, and run the quarterly cycle on your behalf so the next deadline is one less thing to worry about. Contact ARB today to get your account moving.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008