PAYE refund: How to Claim Your Overpaid Tax

If you discover you are due a paye refund, it often means tax has been deducted under the HM Revenue & Customs (HMRC) Pay As You Earn (PAYE) scheme in excess of what you owed. Whether you’re an employee who has paid too much or an employer who has over-remitted PAYE tax, securing a paye refund matters: it improves cash-flow, ensures tax compliance and avoids shading your payroll account with anomalies.

Claiming a paye refund is a process that many find confusing, but it’s essential to retrieve the money that is rightfully yours. At ARB Accountants we specialise in uncovering paye refund opportunities for clients, verifying eligibility, guiding the claim paye refund process and integrating our payroll services to make the refund pathway as smooth as possible. In this article you will learn: what triggers an over-payment under PAYE, how to spot when you or your business might qualify for a paye refund, how to submit a claim from both the employee and employer perspective, expected timescales, common pitfalls and how ARB’s methodology ensures you are well-placed to reclaim the refund you’re owed under PAYE.

Table Of Contents

- What causes a PAYE refund situation to arise?

- How does the HMRC process work for a PAYE refund claim?

- What eligibility criteria and time limits apply for a PAYE refund?

- How do you calculate how much tax you can reclaim under PAYE?

- What are the ways to claim your PAYE refund and how long does it take?

- What pitfalls and risks should you know about when claiming a PAYE refund?

- How does an employer overpaid PAYE refund differ from an employee claim?

- What proactive steps can you take to avoid over-paying under PAYE in the future?

- Conclusion

- Frequently Asked Questions

What causes a PAYE refund situation to arise?

A paye refund situation arises when the tax deducted via the PAYE mechanism exceeds the actual liability. For an individual employee, this can happen for several reasons: an incorrect tax code applied (perhaps emergency tax), income from multiple jobs leading to overlapping personal allowances, starting or leaving employment mid-year benefits in kind that were mis-coded or where deductions were wrong, or when someone leaves the UK during the tax year. (TaxAid) In these scenarios, you’ve essentially paid too much tax. For example, if you find you have overpaid paye tax, it’s usually due to a discrepancy in the records held by HMRC or your employer. From the employer perspective, a business may discover that it has over-paid its PAYE liability to HMRC paye refund because of an error in the Full Payment Submission (FPS) or Employer Payment Summary (EPS), duplicate payments, or mis-reporting of leavers or incentives. (GOV.UK)

For example:imagine an employee who begins a new job in July, but their employer uses the standard annualised allowance on the tax code and fails to account for the partial-year basis. The result: the employee is taxed as if for a full year, so tax is over-deducted and they qualify for a paye refund. This is a clear case where an employee can claim paye refund. In our work at ARB we run what we call a “PAYE over-payment screening” as part of our year-end payroll review. We flag likely refund cases by comparing year-to-date tax deductions, code changes, multiple employment records and benefit-in-kind entries. That methodology ensures we identify refund-worthy situations early and integrate the claim into our payroll or agent-service process. Another common query we address is how to spot the indication of a refund, often visible as a paye refund on payslip as an adjustment.

How does the HMRC process work for a PAYE refund claim?

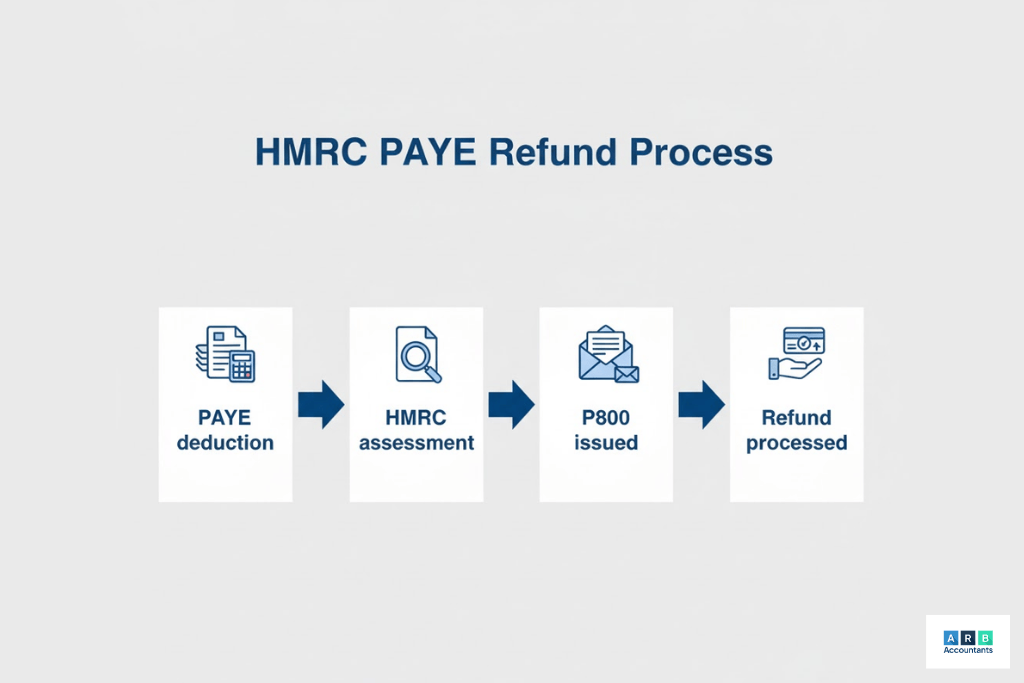

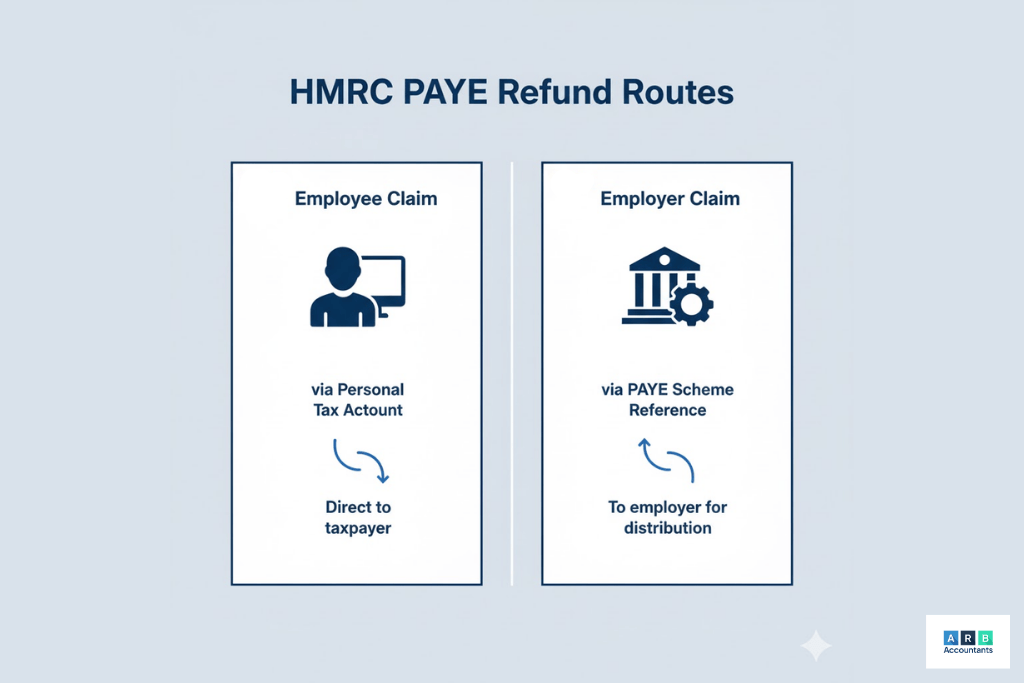

When a paye refund is due, HMRC paye refund uses an automated and a manual mechanism depending on the taxpayer’s circumstances. For most employees, the process starts with an automatic reconciliation through the P800 tax calculation letter. This document compares the total PAYE tax deducted against the actual liability for the year. If an overpayment is identified, HMRC issues a paye refund directly either by bank transfer or cheque, usually within two to four weeks of confirming the P800. If you are an employee who has noticed the P800 calculation confirms you have overpaid paye tax, the process is often automatic. However, if your situation involves multiple employments, benefits in kind, or a change in residency, you may need to claim paye refund manually using your Government Gateway account or the HMRC “Claim a tax refund” online service. (litrg.org.uk)

For employers, the refund route is slightly different. Where a business has overpaid PAYE tax, perhaps due to duplicate submissions or corrections made on the Employer Payment Summary (EPS), HMRC allows you to claim a refund if you’ve paid too much on your PAYE bill either online or by post. The claim is usually made through the employer’s PAYE Online account, or by submitting a written application with evidence such as FPS/EPS adjustments or bank statements. HMRC will first offset the overpaid amount against any outstanding liabilities before issuing an actual refund or credit. (gov.uk) This process ensures the employer isn’t seeking to recover funds that should instead cover other outstanding debts to the government. We regularly advise clients on the steps to can i claim back hmrc payment when a genuine overpayment has occurred on the PAYE bill.

n both cases, individual or employer, the success of a paye refund claim depends on maintaining accurate documentation. At ARB Accountants, we advise clients to keep every P60, payslip, coding notice (P2), and payroll summary on file. This evidence helps verify income figures, ensures the right tax code is applied, and accelerates claim approval. For employees, checking for a paye refund on payslip throughout the year can be a useful proactive measure. We also recommend maintaining a record of communication with HMRC, as incomplete data or missing identifiers often cause refund delays.

If your PAYE refund relates to wider personal income or mixed sources of earnings, getting guidance from a self assessment accountant can help ensure the figures are fully accurate.

What eligibility criteria and time limits apply for a PAYE refund?

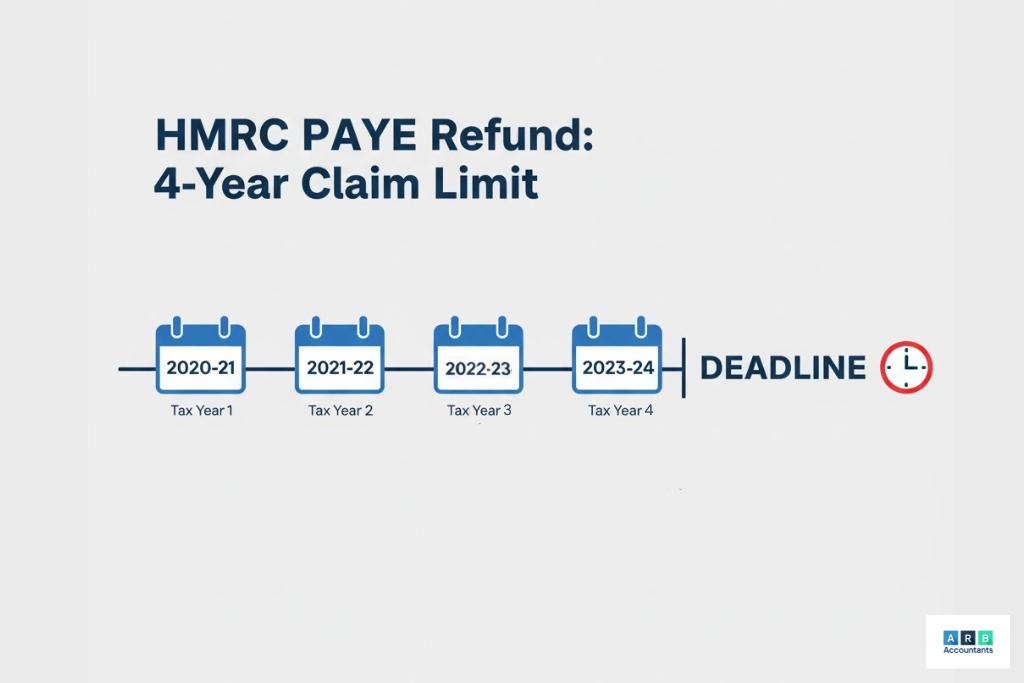

To qualify for a paye refund, you must have genuinely over-paid tax under the Pay As You Earn (PAYE) regime. For employees this means that the tax deducted via PAYE exceeds the actual liability for that tax year. According to TaxAid, an employee can normally make a claim up to four years from the end of the relevant tax year. (TaxAid)

From the employer / PAYE-bill payer perspective, the rules for claiming a paye refund are similar: you must have paid more on your PAYE bill than you owed. This can sometimes occur when an employer mistakenly makes an overpayment by employer to HMRC for the overall PAYE scheme. Importantly, if the employer has any outstanding tax liabilities or PAYE liabilities, the HM Revenue & Customs (HMRC paye refund) will offset the overpayment against those before paying out a refund.

There is a special mechanism known as “Extra-Statutory Concession B41” (ESC B41) which sometimes permits a paye refund to be made for a tax year beyond the four-year window. This only applies in limited circumstances – namely where an overpayment arose because of an error by HMRC (or another government department) and there is no dispute about the facts. (GOV.UK)

How do you calculate how much tax you can reclaim under PAYE?

Calculating how much you can reclaim in a paye refund starts with understanding tax-code mechanics and PAYE deduction logic. A mis-applied tax code (for example an emergency code or incorrect allowance) will lead to paye overpaid tax. The process helps you determine if the amount you paid matches your actual liability.

The calculation steps are as follows:

-

Determine the actual tax paid via PAYE in the tax year (use year‐to‐date figures from payslips, P60, payroll summary).

-

Establish the correct tax liability: apply the personal allowance, correct tax code, benefits in kind, relevant reliefs.

-

Identify the difference between what was paid and what should have been paid, the overpaid tax amount.

-

That difference is your potential paye refund.

For example: assume an employee with earnings of £35,000 was taxed on a code assuming £40,000 earnings (so allowance reduced incorrectly). Their tax paid via PAYE was £5,600 but correct liability should have been £5,100. They may therefore claim a paye refund of £500. This example illustrates how a calculation error can cause paye overpaid tax

In payroll/agent terminology relevant to calculating this: cumulative vs non-cumulative tax codes, “month 1/week 1” basis (non-cumulative), tax year to date (YTD) figures, benefits in kind and the interplay with National Insurance contributions (NICs). Getting the code and basis right is essential to compute an accurate paye refund.

What are the ways to claim your PAYE refund and how long does it take?

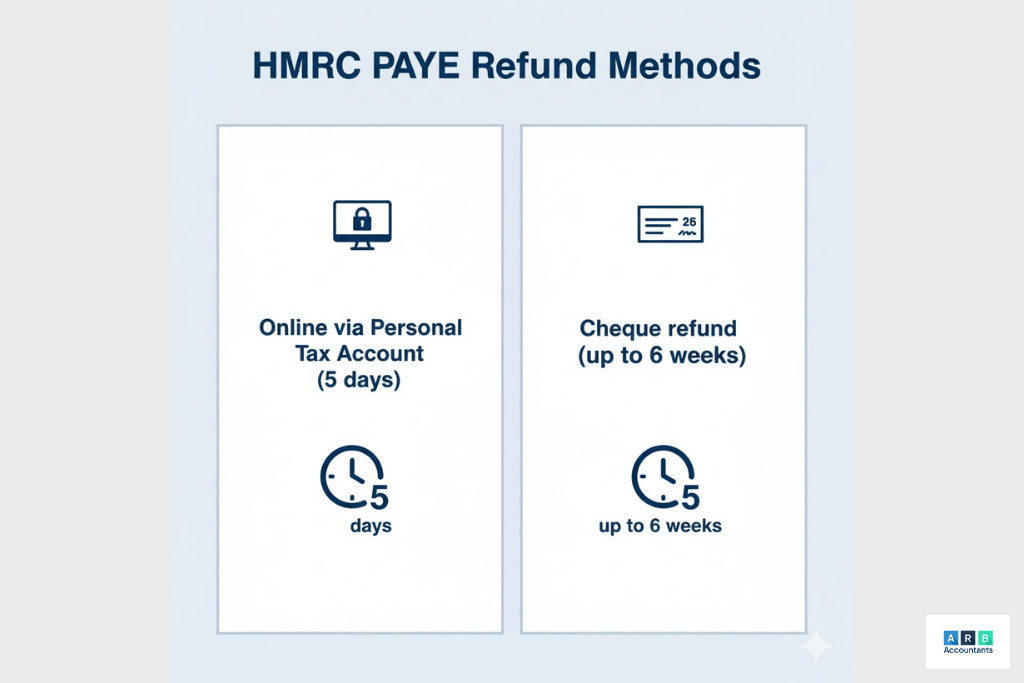

When you believe you are due a paye refund, the method of claim and payment route will significantly affect how quickly you receive your money. For employees, one route is via the HM Revenue & Customs Personal Tax Account or the HMRC app. By choosing the online bank-transfer option and submitting all required details, you can typically secure your paye refund within five working days. (litrg.org.uk) If you opt for a cheque instead, the timeframe lengthens historically up to six weeks.

For employers or agents making a claim of over-paid PAYE tax (i.nclude submitting the online form (for example R38) or posting a letter entitled “Employer PAYE Overpayment” with supporting documentation. (GOV.UK) We understand that employers need to know what happens if you are overpaid by your employer uk on their PAYE account. (GOV.UK)

In terms of typical timescales, HMRC advises five working days for online claims, and up to six weeks for a cheque. However, recent reporting highlights serious delays: some PAYE refunds are taking more than four months to land. (The Guardian) This is a key reason why many ask can i claim back hmrc payment through an agent like ARB for efficiency.

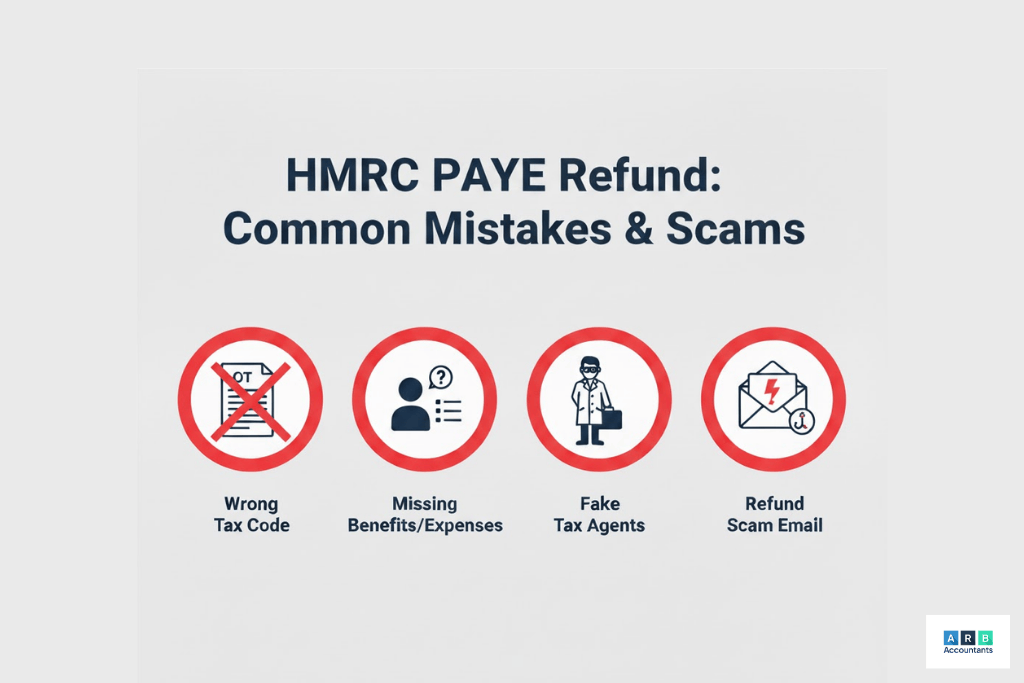

What pitfalls and risks should you know about when claiming a PAYE refund?

Although claiming a paye refund can be straightforward, there are multiple risks and pitfalls which may delay or invalidate a claim, especially when dealing with “paye overpaid tax” or “overpayment by employer”. First, error in tax code assumptions, failure to account for multiple jobs, and missing benefits in kind entries can all lead to inaccurate calculations of overpaid tax. This is where you might find yourself in a situation where the initial calculation for an HMRC paid too much tax refund is incorrect.

Second, once HMRC pays a refund, if later they identify that you were in fact under-paid tax (for example due to under-declared benefits or a changed employment status) they may recover the refunded amount. This recovery risk must be considered before pursuing a paye refund. (litrg.org.uk)

From the employer/agent perspective, a common risk is that an employer seeking a paye refund may have other outstanding liabilities; HMRC will offset the over-paid amount against those liabilities before issuing a refund. (GOV.UK) This is especially important if you suspect your organization is responsible for an overpayment by employer. Additionally, claims that involve directors or complex payroll arrangements often require extensive supporting evidence (e.g., bank statements, payroll summaries) and so pose higher audit exposure.

Another major risk area is using unregistered tax-repayment agents for PAYE rebate or refund claims. From 2 August 2023 HMRC requires registration for agents submitting PAYE rebate claims on behalf of clients. (House of Commons Library) Some tax-refund companies still operate with aggressive marketing, and taxpayers may end up paying fees for a process they could do for free. (THP Chartered Accountants)

How does an employer overpaid PAYE refund differ from an employee claim?

An employer overpaid PAYE refund arises when a business, as the registered PAYE scheme operator, pays more in PAYE liability than it actually owes to HMRC. This differs fundamentally from an employee claim for a paye refund, which typically occurs because of an incorrect tax code or employment change leading to over-deduction of income tax. When an employer overpaid me uk, it is usually about the overall scheme liability, not the individual’s tax deduction. In an employer case, the issue stems from payroll or submission discrepancies rather than personal allowances.

For instance, an employer might over-declare PAYE due to duplicated FPS submissions, mid-year staff terminations not properly processed, or payroll software configuration errors. HMRC’s official guidance, “Claim for a refund if you’ve paid HMRC too much on your PAYE bill” (GOV.UK), explains that before submitting any refund request, employers must identify precisely why they overpaid wages. According to Tax Journal, this has become a growing compliance focus, as HMRC has seen rising volumes of refund requests that stem from employer reporting inconsistencies. We provide clarity on if you are overpaid by employer uk on their scheme payments.

The procedural difference is key: employee claims rely on tax-code reconciliations (usually through a P800 or Self Assessment correction), while employer refund claims are processed under the PAYE scheme reference and offset against outstanding liabilities before being paid out. Employers cannot claim back tax withheld from employees, that must be handled by HMRC directly with the individual. We help clients navigate the complexities of an overpayment by employer.

What proactive steps can you take to avoid over-paying under PAYE in the future?

When it comes to avoiding a missed paye refund, proactive tax-code and payroll management matter. One key step is to review tax codes each time there’s a change in circumstances: job change, multiple jobs, benefit changes (such as a company car or health cover), starting pensions, or leaving the UK. For example, when you move from full-time employment into part-year, the wrong tax-code basis can lead to overpaid paye tax and future paye refund claims. The official guidance confirms that your tax code determines how much tax-free allowance you receive and so errors can directly impact whether you end up over-paying.

From the employer/agent side we recommend best practice: monitor scheme PAYE liabilities monthly, reconcile the employer payment summary (EPS) and FPS submissions early, adjust payroll when tax-codes change mid-year, and maintain a full evidential trail (payslips, coding notices, benefits in kind records). This ensures you avoid situations where an employer overpaid me uk on their tax bill and needs to file for an overpayment by employer claim. Understanding the rules for overpaid wages can also prevent complications down the line.

We also recommend leveraging technology/tools. Use payroll software alerts when tax-codes or employment status change, encourage employees to use their personal tax account (or HMRC app) to check their tax code and payslip, and set up internal dashboards for payroll teams to log tax-code changes and track refund-risk exposure. If you are an employee, knowing what happens if you are overpaid by your employer uk is crucial for prompt correction.

Conclusion

A paye refund may be due whenever tax has been over-deducted under the PAYE system, whether for employees (HMRC paid too much tax) or where an employer has over-paid its scheme liabilities. At ARB Accountants we help clients through every phase: from PAYE over-payment screening and refund claim support, to ongoing payroll reconciliation and proactive prevention services. The key takeaway is: act promptly and maintain audit-quality documentation so you don’t miss the time limits and can support any claim effectively. If you’d like a free review of whether you’re eligible for a paye refund or an employer over-payment audit, please contact us at ARB. The peace of mind that comes from knowing can i claim back hmrc payment effectively is invaluable.

Frequently Asked Questions

How long does it take for a PAYE refund to be paid?

Typically, when you submit a claim for a paye refund via online methods (for example using your Personal Tax Account) and choose the bank-transfer route, HMRC processes it in about five working days. If you select cheque payment, it may take up to six weeks. Recent media reports indicate delays of more than four months in some cases.

Can I claim a PAYE refund if I changed jobs mid-year?

Yes, if you changed jobs and your tax was deducted on a cumulative basis without correction for the shorter employment period, you may have overpaid wages and be eligible for a paye refund. You can claim via your Personal Tax Account or wait for the P800 calculation from HMRC paid too much tax.

If my employer over-paid my tax, can they claim the PAYE refund instead of me?

If the overpayment relates to the employer’s PAYE scheme liability (i.e., the employer paid too much to HMRC), the employer must claim the paye refund via the scheme reference. However, if the overpaid by employer uk tax was deducted from you as an employee, the employer must make arrangements to refund you unless you agree otherwise.

What happens if HMRC pays me too much PAYE refund?

If HMRC pays you a paye refund in error, you will need to repay the excess and may face arrears or penalties, especially if you knowingly kept the overpayment. This is a possibility to be aware of if HMRC paid too much tax to you

Up to how many years back can I claim a PAYE refund?

Generally, employee claims for the paye refund must be made within four years of the end of the relevant tax-year. For older years, you may only claim under limited circumstances (for example via Extra-Statutory Concession B41). If you are looking to recover overpaid wages from many years ago, the four-year limit is the primary rule.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008