Spring Budget 2026: What It Means for You, Your Business and Your Finances

The Spring Budget statement delivered on 3 March 2026 maintained a deliberately low-key approach. Chancellor Rachel Reeves positioned the Autumn Budget as the primary fiscal event, relegating the spring statement to reviewing economic forecasts rather than introducing sweeping policy changes. That does not mean the tax landscape is standing still - significant changes announced previously are still rolling out, and the frozen thresholds continue to bite.

Below is what matters most for individuals, directors, landlords, and business owners from April 2026 onwards.

Key Economic Indicators

Economic growth was downgraded to 1.1% for 2026, down from the 1.4% November projection. Unemployment forecasts rose slightly to 5.3%, while inflation expectations improved to 2.3% by year-end. The picture is one of slower growth and continued pressure on household budgets.

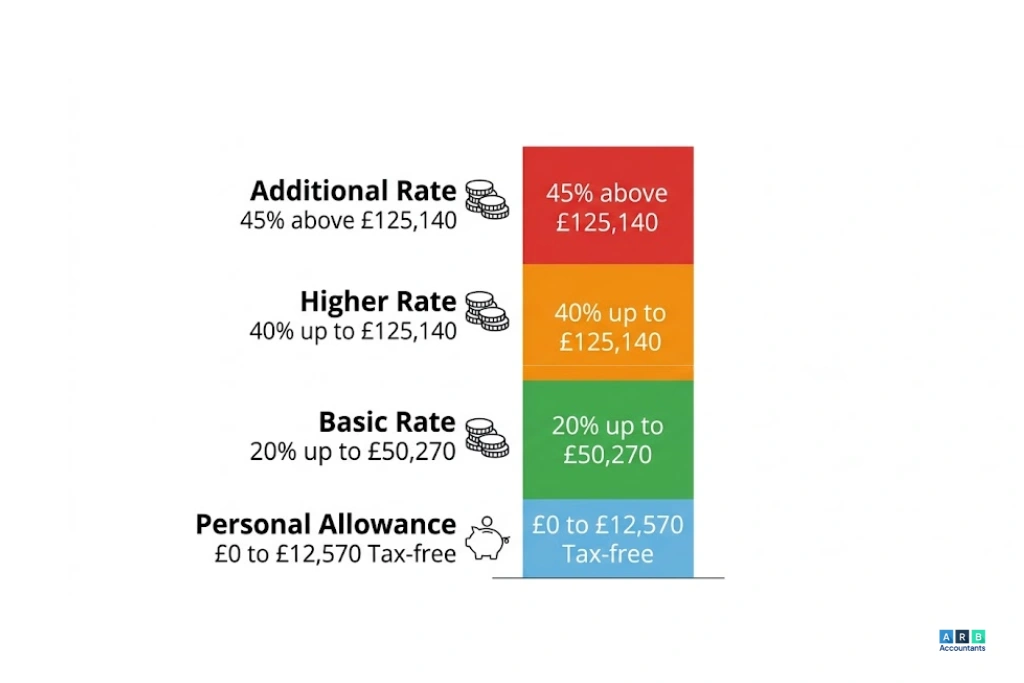

Frozen Tax Thresholds: The Silent Tax Rise

The personal allowance remains at £12,570, with the higher rate threshold locked at £50,270 through April 2031. This creates fiscal drag - a mechanism whereby wage increases push earnings into higher tax bands despite unchanged headline rates, effectively creating a stealth tax increase.

If your salary rises with inflation, more of your income crosses into the 40% band each year without any headline rate change. Planning ahead - through pension contributions, salary sacrifice, or dividend structuring - is the only way to mitigate the effect.

Dividend Tax Increases Effective April 2026

From 6 April 2026, basic rate dividend tax rose from 8.75% to 10.75%, while higher rates increased from 33.75% to 35.75%. The dividend allowance remains at £500 annually.

Limited company directors should review their salary-to-dividend structures urgently. The extra 2 percentage points on every pound of dividend above £500 adds up quickly over a tax year, and the traditional “low salary, high dividends” model now delivers less benefit than it used to.

ISA Allowance Updates

For 2026/27, the £20,000 annual ISA limit persists unchanged. However, from April 2027, cash ISA restrictions will limit that portion to £12,000 for those under 65. Additionally, savings tax rates outside ISA wrappers will increase by 2 percentage points across all bands beginning April 2027.

If you have cash savings you are planning to move into an ISA, using the current year’s allowance before the 2027 restrictions kick in is the straightforward option.

Stamp Duty Status Quo

No stamp duty adjustments were announced. The holiday ended 31 March 2025, reverting thresholds to previous levels. Landlords continue facing the 5% surcharge on additional properties, with capital gains tax at 18% (basic rate) and 24% (higher rate).

Making Tax Digital Implementation

From 6 April 2026, sole traders and landlords exceeding £50,000 in annual income must use HMRC-approved software for quarterly submissions alongside the January 31 final declaration. This threshold descends to £30,000 from April 2027 and £20,000 from April 2028.

If you are affected and have not yet chosen MTD-compliant software, now is the time. We work with Xero, QuickBooks, and FreeAgent and can get you set up before the deadline.

Inheritance Tax: No Changes Announced

The spring budget contained no reversals to inheritance tax reforms. Business property relief on listed shares now restricts to 50% from April 2026. The nil-rate band remains frozen at £325,000 through 2031, while inherited pension pots will fall within the IHT scope from April 2027 - a significant shift for estate planning strategies.

If you have pension wealth earmarked for beneficiaries, the rules changing in 2027 deserve a fresh look at your estate plan this year.

Recommended Actions for Business Owners

- Review dividend structures reflecting new rates

- Maximise 2026/27 ISA allowance before April 2027 restrictions

- Prepare systems for mandatory Making Tax Digital compliance

- Evaluate inheritance tax exposure given frozen thresholds

- Address fiscal drag impacts through legitimate planning mechanisms

The Bottom Line

Though described as unremarkable, the tax landscape continues shifting through cumulative changes from prior announcements, perpetual threshold freezes, and scheduled reforms. Proactive planning - rather than reactive responses - positions individuals and business owners to navigate these transitions effectively.

If you would like to discuss how any of these changes affect you specifically, book a free consultation with our team.

Frequently Asked Questions

Did the Spring Budget 2026 announce any new tax rises?

No new tax increases were introduced in the 3 March 2026 statement itself. However, substantial changes announced in the 2025 Autumn Budget continue rolling out throughout 2026 and beyond, including dividend tax increases and new Making Tax Digital requirements.

What happened to ISA allowances in the Spring Budget 2026?

Current limits remain unchanged for 2026/27. The £20,000 annual allowance persists, though cash ISA restrictions reducing that portion to £12,000 for under-65s begin in April 2027.

Did the Spring Budget 2026 change stamp duty?

No. No modifications were announced, maintaining the post-holiday thresholds established in April 2025. Landlords continue to face the 5% surcharge on additional properties.

What are the key tax changes actually happening in April 2026?

Dividend rates increased to 10.75% and 35.75%. Making Tax Digital became mandatory for those exceeding £50,000 income. Business Asset Disposal Relief CGT increased to 18%, and late corporation tax filing penalties doubled.

Does the Spring Budget 2026 affect landlords?

Indirectly. While no landlord-specific measures were introduced, dividend tax increases impact those holding property through limited companies. OBR forecasts suggest rising capital tax revenues through 2031.

What is fiscal drag and how does it affect me?

Fiscal drag occurs when frozen tax thresholds combine with inflation-driven income growth, pushing earnings into progressively higher tax bands without rate changes. With thresholds frozen through April 2031, this effect compounds every year.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008