What Does a Good Balance Sheet Look Like?

A strong balance sheet is the backbone of a financially stable business, yet many companies struggle with managing their assets and liabilities effectively. Without the right balance, businesses face cash flow problems, high debt, and difficulty securing funding. This can lead to missed opportunities for growth and even financial instability.

Strong balance sheets aren’t just for large companies, even small businesses and freelancers benefit from clear financial reporting, which is why many rely on specialist accountants for freelancers to keep everything on track.

So, what makes a strong balance sheet? It’s one that supports business goals, ensures liquidity, and maintains a balanced capital structure. In this article, we’ll break down the key components of a strong balance sheet and why it’s crucial for long-term success.

Table Of Contents

- What Makes a Strong Balance Sheet?

- How Do You Know if a Balance Sheet is Strong?

- What is the Most Important Thing on a Balance Sheet?

- What is a Good Balance Sheet Ratio?

- Balance Sheet vs P&L: What is the Difference?

- Why is a Strong Balance Sheet Important?

- Accounting and Bookkeeping Services Essex

- Frequently Asked Questions

What Makes a Strong Balance Sheet?

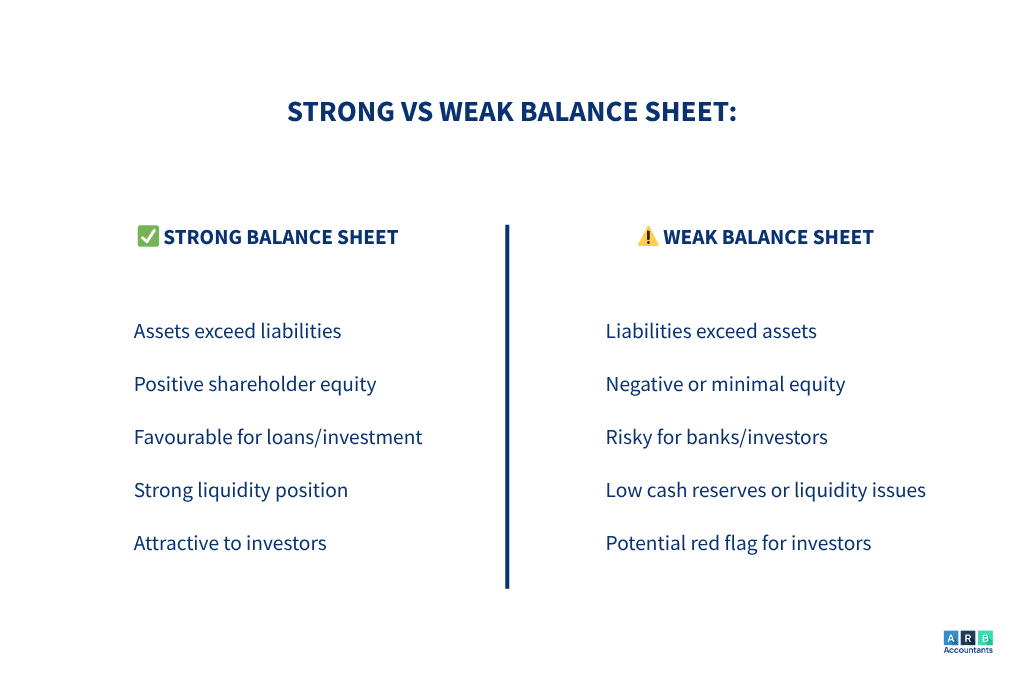

So, what is a strong balance sheet? A company with a strong balance sheet is structured to support business goals and maximize profits. A strong balance sheet should include:

-

Intelligent working capital

-

Positive cash flow

-

A balanced capital structure

-

Income-generating assets

Read on to learn more about what makes a strong balance sheet and the factors that impact it.

It is worth noting that what makes a strong balance sheet is not just about having more assets than liabilities. The quality and liquidity of those assets matters just as much as the headline figure. A business with significant fixed assets but poor cash flow can still find itself under financial pressure, which is why understanding the full picture is so important.

Contractors, in particular, depend on stable cash flow and low debt structures, making the guidance of experienced contractor accountantsespecially valuable when reviewing balance sheet health.

“One most common red flag on a weak balance sheet is assets, which some small companies don't capitalise on the balance sheet. What I mean by that is, for example, let's say Epic or even my business, ARB Accountants. Let's say we buy furniture for the office, a sofa or a table or chairs or desk or computer, the things that we use in an office. Most businesses think, 'Oh, it's just an expense,' because we've spent money for the business. But it's not, it's actually an asset.

And the reason is because it’s going to last more than a year. You’re not going to replace your desk or laptop every year. So they cannot be an overhead, they have to be capitalised. If they are capitalised on your balance sheet, suddenly you have assets that weren’t there before. Otherwise, you entered them in the profit and loss as an expense. So effectively, if you’re missing £5,000 worth of assets on your balance sheet, it will look weak because it’s just a misallocation of a transaction.”

How Do You Know if a Balance Sheet is Strong?

If you’re not an accountant, it can be difficult to know what a good balance sheet look like and assess your company’s financial health. The If you are not an accountant, it can be difficult to know what a good balance sheet looks like and assess your company’s financial health. The following steps will help you determine whether your company is financially strong based on balance sheet data:

-

Determine if the company has enough current assets to pay its financial obligations. A company with more liabilities than assets is considered financially weak.

-

Calculate the current ratio: divide total current assets by current liabilities. A current ratio of 1 or greater is preferable.

-

Calculate the quick ratio: subtract inventory from current assets and divide by current liabilities. A quick ratio higher than 1 indicates good financial health.

-

Calculate the cash-to-debt ratio: add cash and short-term investments, then divide by current and long-term liabilities. A ratio of 1.5 or more is favourable.

-

Calculate the debt-to-equity ratio: divide total liabilities by shareholders’ equity. A ratio lower than 1 shows financial strength.

-

Compare financial data to past balance sheets and industry ratios to assess trends.

If you are wondering what does a healthy balance sheet look like, it is one that meets these financial strength criteria consistently over time. Reviewing these figures alongside your monthly management accounts gives you a much clearer picture of performance throughout the year, rather than waiting until year end to spot any issues.

"Some clients don't understand the difference between short-term liability and a long-term liability. A short-term liability needs to be paid within the next 12 months. Long-term is anything between 1 year and 5 years. Let's say you have a bank loan of £30,000, only the portion due within the next 12 months should be current liabilities, say £4,000. The remaining £26,000 is long-term. If you put the full £30,000 under current liabilities, a third party might think the company is not doing great."

What is a Weak Balance Sheet?

A weak balance sheet typically signals poor business performance. It may reveal:

• Negative equity

• Negative or deficit retained earnings

• Negative net tangible assets

• Low current ratio

A weak balance sheet does not always mean the business is failing, but it is a clear signal that action is needed. Deficit retained earnings, for example, can result from a period of planned investment rather than trading losses. Context matters, and comparing your position against prior years and industry benchmarks will give you a more accurate read. If any of these warning signs appear in your accounts, speaking to an accountant early gives you the best chance of addressing them before they become serious problems.

What Factors Evaluate Financial Strength?

Businesses with strong balance sheets go beyond just having more assets than liabilities. They are structured for efficiency and performance, supporting business goals.

A strong balance sheet typically includes:

• A positive net asset position

• The right amount of key assets

• More debtors than creditors

• A fast-moving receivables ledger

• A good debt-to-equity ratio

• A strong current ratio

What makes a healthy balance sheet in practice is these factors working together. A fast-moving receivables ledger means your customers are paying promptly, which directly improves your cash position and reduces the risk of bad debt. Keeping a close eye on your debtor and creditor balance also helps you spot cash flow pressure before it becomes a bigger problem. Good cash flow planningsits alongside balance sheet management as part of a healthy overall financial position.

What is the Most Important Thing on a Balance Sheet?

There are three key components of a balance sheet:

Assets

Divided into current and noncurrent assets, with cash being the most important. Current assets include cash, debtors, and stock. Noncurrent assets cover property, equipment, and long-term investments. Cash is the most critical asset on any balance sheet because it represents immediate liquidity: the ability to meet obligations, pay staff, and invest in growth without needing to liquidate anything else.

Liabilities

Includes current and noncurrent liabilities. A company should have fewer liabilities than assets, particularly in relation to cash flow. Current liabilities are obligations due within 12 months, such as supplier invoices and short-term loans. Noncurrent liabilities include longer-term borrowings such as bank loans or finance leases.

Equity

Calculated as assets minus liabilities, equity represents shareholder claims on the business. Retained earnings are a crucial part of equity and are key to assessing financial health. Growing retained earnings year on year is one of the clearest signs of what a healthy balance sheet looks like over time.

"In some businesses, debtors (people who owe you money) being higher than creditors (people you owe) can be a red flag. In my case, my debtors are always higher, but I don't owe a lot to suppliers. That's fine for me. But in some industries, if you pay your suppliers quickly but your customers don't pay on time, your cash flow will suffer. You'll face shortages or cash flow issues even if your balance sheet looks fine on the surface."

What is a Good Balance Sheet Ratio?

Performing key financial calculations helps assess a company’s financial position. Here are the four ratios that matter most when evaluating what a good balance sheet looks like:

Current Ratio

Indicates whether the company has enough cash and short-term assets to cover short-term obligations.

**Formula: **Current Assets divided by Current Liabilities

**Ideal Range: **1.5 to 2 (varies by industry)

Quick Ratio

Similar to the current ratio but excludes inventory, giving a more conservative view of short-term liquidity.

**Formula: **(Current Assets minus Inventories) divided by Current Liabilities

**Ideal Range: **Higher than 1

Working Capital

Shows the difference between current assets and liabilities, indicating whether the business can fund its day-to-day operations.

**Formula: **Current Assets minus Current Liabilities

**Impact: **A positive value is good in most industries. In certain sectors like retail, negative working capital can be favourable. For most SMEs, though, positive working capital is a key marker of what is a strong balance sheet.

Debt-to-Equity Ratio

Shows how reliant the business is on debt to fund its assets.

**Formula: **Total Liabilities divided by Shareholders’ Equity

**Ideal Range: **Lower ratios are preferable, but a ratio of 0 can indicate inefficiency. A ratio below 1 is generally a sign of what makes a strong balance sheet.

These balance sheet ratios help determine financial health. Landlords also monitor assets and debt closely, and many work with accountants for landlords to keep their portfolios stable.

Balance Sheet vs P&L: What is the Difference?

Two of the most important financial documents in your business are the balance sheet and the profit and loss (P&L) statement, and the two are often confused.

The P&L shows your income, costs, and profit or loss over a defined period, typically a financial year. It tells you whether the business made money. The balance sheet is a snapshot of what the business owns and owes at a specific point in time. It tells you the cumulative financial position.

A business can be profitable on the P&L yet still have a weak balance sheet, for example if it has taken on significant debt or distributed most of its retained profits as dividends. This is why lenders and investors always review both documents together. Understanding the relationship between the two is an important part of knowing what a good balance sheet looks like in the context of your overall financial health.

Why is a Strong Balance Sheet Important?

A balance sheet provides a snapshot of what a business owns and owes within a financial year. Comparing balance sheets over time helps you assess business performance, spot trends, and make better decisions about growth, investment, and risk.

Investors use balance sheets to make informed decisions about lending, while business owners can use them to identify financial risks and opportunities early. For limited companies, preparing and filing accurate accounts including your balance sheet is also a legal requirement. Late or inaccurate filing can result in penalties from Companies House, so getting this right matters both financially and from a compliance perspective.

This is why a balance sheet is important for both businesses and investors, and why it should be reviewed regularly rather than just at year end.

"I had a client, a tile business, they were doing over a million in turnover but always struggled with cash flow. Whenever I visited them, they looked busy but if you're not making money or are just breaking even, what's the point of employing 10 people and running like a headless chicken? We looked into it. They were buying too much stock to get supplier discounts. But they weren't selling it fast enough.

They’d get 30-day payment terms from the supplier but it would take 6, 9, 12 months to sell the stock. So they’re paying for things much earlier than they’re getting money back. We had conversations and made changes: Don’t overbuy stock, Negotiate longer credit terms, say 90 days. You can apply this logic to any business whether tiles, clothes, or retail. You need a variety of stock to sell, but you also need a plan to keep your cash cycle healthy.”

Accounting and Bookkeeping Services Essex

ARB Accountants offer a wide range of accounting and bookkeeping services in Essex and across the UK, including the preparation of balance sheets. Our chartered accountants in Essex will calculate your annual balance sheet whilst ensuring that you fully understand your financial landscape, and how it can impact your business.

Get in touch with us today to learn more about how our team of experienced accountants in Essex can help you keep on top of your business’ finances.

I have worked with this company for 2 years now and it has been a great support for my business. They have helped me grow and succeed.

Is Your Balance Sheet Holding Your Business Back?

Get a free Balance Sheet Health Scorecard to instantly identify financial red flags and improvement areas.

Frequently Asked Questions

Why is a balance sheet important for business loans?

Lenders use balance sheets to assess financial health and determine whether a business can repay a loan. A healthy balance sheet with positive equity, manageable debt, and strong liquidity ratios improves your chances of approval and can help you secure more favourable terms.

How do balance sheet ratios help in financial analysis?

They measure liquidity, debt levels, and overall financial stability, helping businesses track performance over time and compare against industry benchmarks. Identifying a declining ratio early gives you the opportunity to address it before it becomes a serious issue.

What is a strong balance sheet in terms of risk management?

It balances assets and liabilities in a way that keeps debt manageable and maintains financial resilience. A strong balance sheet means the business can absorb setbacks, such as a slow trading period or an unexpected cost, without being pushed into financial difficulty.

What does a healthy balance sheet look like for liquidity?

It has enough current assets to cover short-term liabilities without financial strain. A current ratio of 1.5 to 2 and a quick ratio above 1 are the benchmarks most commonly used to assess this.

What does a good balance sheet look like for long-term growth?

It maintains a solid debt-to-equity ratio, sustainable cash flow, and growing retained earnings. This gives the business the financial foundation to invest, take on new opportunities, and attract funding when needed.

What is the difference between a balance sheet and a P&L?

The profit and loss statement shows income and expenses over a period and tells you whether the business made a profit. The balance sheet is a snapshot of what the business owns and owes at a specific date. Both are essential: the P&L tells you how the business performed, while the balance sheet tells you its current financial position.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008