Code of Practice 9: Protecting Yourself in HMRC Investigations

What is Code of Practice 9?

Code of Practice 9 (COP9) is HMRC's civil procedure for investigating suspected serious tax fraud. HMRC issues it when it suspects deliberate behaviour caused a loss of tax but wants to resolve the matter civilly rather than through prosecution. It offers entry into the Contractual Disclosure Facility: admit the fraud, make a full disclosure, and receive written immunity from criminal prosecution. You have exactly 60 days to decide.

Receiving a Code of Practice 9 letter from HMRC is one of the most serious tax situations you can face. It means HMRC suspects deliberate fraud — not errors, not carelessness, but intentional behaviour that led to a loss of tax. How you respond in the following 60 days could be the difference between a civil settlement and a criminal prosecution.

This guide explains what Code of Practice 9 is, how the process works, what your two options are, and why appointing a specialist adviser the moment you receive that letter is something you should not delay.

Table Of Contents

- What Is Code of Practice 9?

- What Is Code of Practice 9 in Plain Terms?

- What Triggers a COP9 Investigation?

- Your Two Options: Accept or Reject the CDF

- A Real-World Example

- The COP9 Process: What Happens After You Accept

- What Happens If You Reject the CDF?

- Can You Request COP9 Voluntarily?

- COP9 vs COP8: The Difference

- Why COP9 Specialists Matter

What Is Code of Practice 9?

Code of Practice 9, known as COP9, is HMRC's formal procedure for investigating cases of suspected serious tax fraud on a civil basis. It is operated exclusively by HMRC's Fraud Investigation Service, and it is the most serious civil tax investigation HMRC conducts.

The key distinction is the word civil. HMRC uses Code of Practice 9 when it suspects fraud but does not want to pursue criminal prosecution immediately. Instead, it offers you a structured route to resolve the situation: the Contractual Disclosure Facility (CDF). This is a formal agreement between you and HMRC. You admit to the fraud, disclose everything, cooperate fully, and in return HMRC provides a written guarantee of immunity from criminal prosecution.

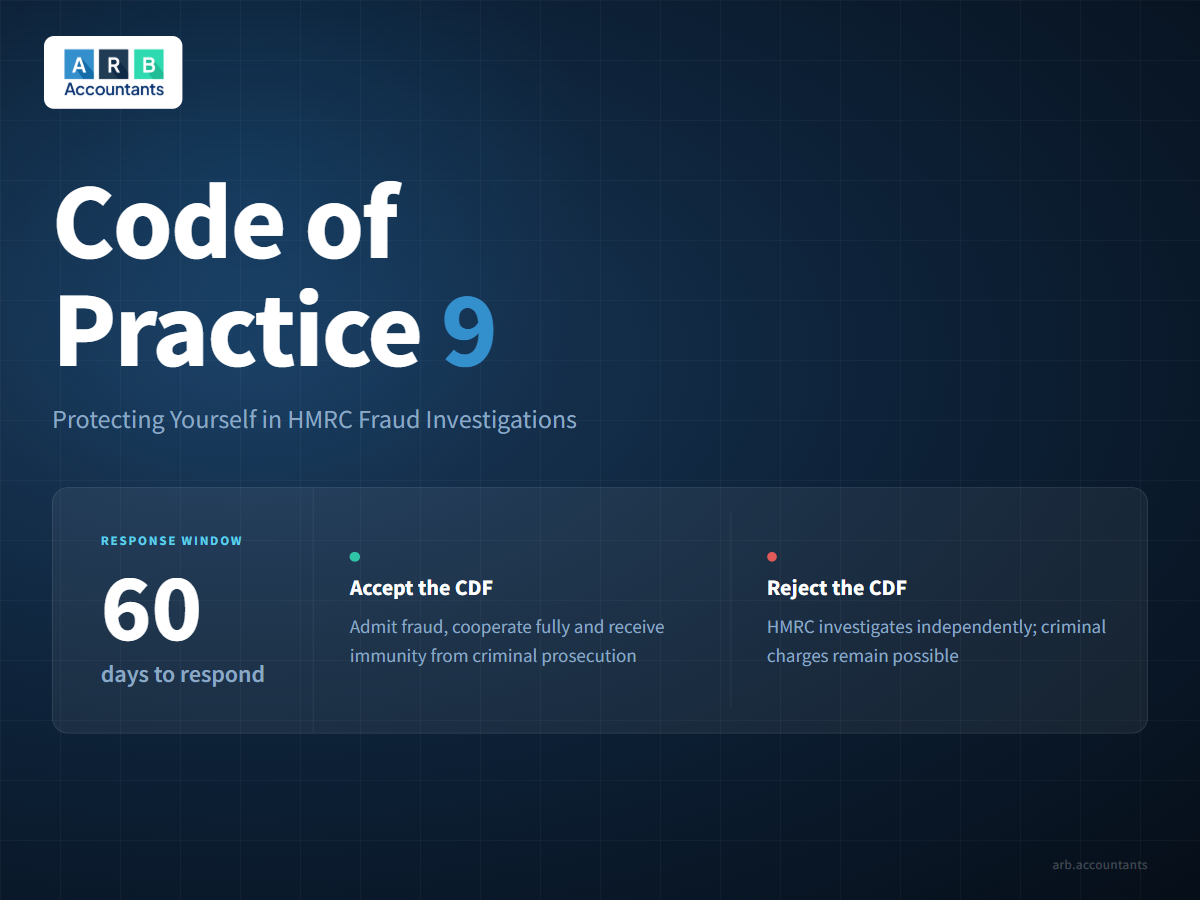

That offer comes with a clock. You have exactly 60 days to decide.

What Is Code of Practice 9 in Plain Terms?

Think of it this way. HMRC believes you deliberately underpaid tax. That is a criminal offence in the UK. Rather than referring you for prosecution immediately, HMRC is giving you a controlled way to resolve the situation on a civil basis.

You come clean about what happened, pay back what you owe along with interest and penalties, and HMRC closes the matter without criminal charges. It is not a soft outcome. The penalties can be very significant and HMRC can look back up to 20 years into your tax affairs. But for most people, it is a far better result than facing a criminal investigation.

What Triggers a Code of Practice 9 Investigation?

HMRC does not issue COP9 letters on a hunch. By the time the letter arrives, HMRC has already gathered evidence. It has access to bank transaction reports, data shared by overseas tax authorities, Companies House filings, Land Registry records, tips from the public, and referrals from law enforcement agencies.

When the information HMRC holds does not match what you have declared on your tax returns, it investigates. If HMRC concludes the discrepancy is likely deliberate rather than accidental, it moves to COP9.

Common triggers include:

- Undisclosed offshore accounts or assets

- Cash income not reported on tax returns

- Inflated or fictitious expense claims

- Rental income from property that was not declared

- Undisclosed business profits

- Improper use of company funds by directors

The Contractual Disclosure Facility: Your Two Options

When HMRC sends you a Code of Practice 9 letter, it includes an offer to enter the Contractual Disclosure Facility. You have two choices, and only two.

Option 1: Accept the CDF. You admit that your deliberate behaviour caused a loss of tax. You provide an Outline Disclosure within 60 days, setting out the nature of the fraud, the years it covered, and the involvement of other people or entities. HMRC works through the investigation with you, leading to a full Disclosure Report, penalty negotiations, and a contract settlement. In return, HMRC guarantees you will not face criminal prosecution for matters you have fully disclosed.

Option 2: Reject the CDF. If you genuinely believe you have not committed fraud, you can reject the offer. HMRC then carries out its own investigation independently. A Rejection Letter can be used in tribunal proceedings, so legal advice before signing is essential. If HMRC’s investigation finds deliberate fraud, you will face higher penalties and the real possibility of criminal charges.

One significant change to be aware of: the previous ‘Denial’ route — which allowed you to deny fraud while cooperating with HMRC’s investigation — has been withdrawn. When Code of Practice 9 is issued, you now have just two paths: accept or reject.

A Real-World Example

A self-employed builder receives cash payments from customers and, over several years, does not declare a significant portion of that income on his self-assessment returns. He reports only part of his actual earnings.

HMRC’s data matching identifies a gap between his reported income and his lifestyle, including property purchases that do not align with what his tax returns show. HMRC’s Specialist Investigations team opens a Code of Practice 9 investigation and sends the letter.

He contacts a COP9 specialist immediately. The specialist reviews the situation, confirms that the undeclared income was deliberate, and recommends accepting the CDF. The Outline Disclosure is prepared well within the 60-day window and all HMRC correspondence is handled by the specialist.

The disclosure covers nine years of undeclared income. Penalties are negotiated down to the minimum applicable level, based on the quality of the disclosure and the full cooperation provided throughout the process. The case settles by contract. No criminal prosecution follows. Had the builder rejected the CDF or tried to handle the process himself, the outcome could have been very different.

The Code of Practice 9 Process: What Happens After You Accept

Accepting the CDF starts a structured process with clear stages. Understanding what each stage involves helps you prepare and shows HMRC you are engaged seriously.

Stage 1: Outline Disclosure (within 60 days)

You set out a summary of the deliberate conduct being disclosed. This does not need precise figures if you cannot reasonably calculate them within the timeframe, but it must be honest and made in good faith. HMRC expects you to explain what you did, how you did it, who else was involved, and how you benefited from the conduct.

Stage 2: HMRC Confirms Acceptance

HMRC reviews the Outline Disclosure and typically responds within around four weeks. Once accepted, you are formally inside the COP9/CDF process and HMRC’s guarantee of criminal immunity applies, provided you complete a full and accurate disclosure.

Stage 3: Opening Meeting

HMRC usually requests a face-to-face meeting between you, your adviser, and the case officer assigned. You are not legally required to attend, but not attending is viewed as a lack of cooperation and can affect your penalty level. The meeting covers the scope of the investigation and what HMRC expects in the Disclosure Report.

Stage 4: Disclosure Report Preparation

This is the most detailed part of the process. The report must quantify all tax irregularities — including deliberate and non-deliberate errors — across all relevant years. It must include a business history, an explanation of each irregularity, calculations of tax, interest and penalties owed, and a certified statement of worldwide assets and liabilities. Bank account and credit card certificates for the relevant period are also required.

Stage 5: Penalty Negotiations

HMRC can charge penalties of up to 200% of the tax lost, particularly for offshore deliberate conduct. The level depends on the behaviour, the quality of the disclosure, and the degree of cooperation. An experienced COP9 specialist will make representations to HMRC arguing for the minimum applicable penalty. In complex cases, getting this right makes a very significant difference to the final bill.

Stage 6: Contract Settlement

Once the tax, interest and penalties are agreed, the case is settled by contract. If you need to pay in instalments or require time to sell assets to raise funds, raising this with HMRC early in the process gives you the best chance of workable payment terms.

What Happens If You Reject the Contractual Disclosure Facility?

Rejecting the CDF does not make the investigation stop. HMRC will investigate independently and can obtain information about your finances from banks, overseas authorities, and third parties without your involvement. It can raise assessments, charge interest, start legal proceedings to secure your assets, and refer the case to its criminal investigation unit.

If a criminal prosecution follows, the consequences are serious:

- A summary conviction carries a maximum of six months in prison or a fine of up to £5,000

- Conviction on indictment carries a maximum sentence of seven years imprisonment

- The most serious charge — ‘cheating the public revenue’ — carries a maximum life sentence

- Under the Criminal Finances Act 2017, companies can also face prosecution for failing to prevent the facilitation of tax evasion

HMRC operates a selective prosecution policy, focusing on high-profile individuals, professionals such as accountants and solicitors, and cases where the fraud covered multiple years or the tax loss is large. These cases are prioritised because they send the strongest deterrent message to others.

If you genuinely have not committed fraud and are rejecting the CDF on that basis, a specialist adviser can work through HMRC’s investigation with you and demonstrate that any errors in your returns were not deliberate.

Can You Request Code of Practice 9 Voluntarily?

Yes. If you know you have committed tax fraud and want to put your affairs right before HMRC comes to you, you can proactively request Code of Practice 9 by submitting form CDF1. This is known as a voluntary or unprompted disclosure.

Unprompted disclosures attract lower penalties than disclosures made after HMRC has already opened an investigation. HMRC carries out background checks on receipt, including confirming you are not already under a criminal investigation. If accepted, the same process follows. Taking the initiative gives you the greatest control over the outcome.

COP9 and COP8: Understanding the Difference

Code of Practice 8 (COP8) applies to serious tax avoidance and cases where HMRC suspects fraud but does not yet have sufficient evidence to make that allegation directly. COP8 does not offer immunity from criminal prosecution.

Code of Practice 9 is used where fraud is more clearly suspected. If a COP8 investigation uncovers evidence of deliberate fraud, HMRC may upgrade to COP9 or refer the case for criminal investigation. If you are currently under a COP8 investigation and you know fraud has occurred, speaking to a COP9 specialist about requesting COP9 voluntarily is worth doing quickly.

Why Code of Practice 9 Specialists Matter

HMRC’s own guidance states that many people find it helpful to appoint a specialist adviser familiar with COP9. That guidance understates the importance of getting the right support.

The COP9 process has strict deadlines, complex disclosure requirements, and serious financial consequences if you get it wrong. A poorly prepared Outline Disclosure can cause HMRC to withdraw the CDF. An incomplete Disclosure Report can leave matters outside the scope of disclosure open to criminal proceedings. Penalty negotiations without experienced representation produce worse outcomes.

Specialist advisers with knowledge of HMRC COP9 investigations understand how HMRC’s Fraud Investigation Service thinks and operates. Many have worked inside HMRC. They know where HMRC’s assessing powers reach their limits and can:

- Push back where appropriate

- Prepare a disclosure report detailed enough to satisfy HMRC without volunteering unnecessary information

- Argue effectively for the lowest penalty the circumstances allow

The cost of specialist representation is, in the vast majority of cases, a fraction of the additional penalties and interest that arise from handling Code of Practice 9 without expert help.

A Note on Tax Rules and Professional Advice

HMRC’s investigation procedures, disclosure facilities, and penalty frameworks are subject to change. The information in this article reflects the position as understood at the time of writing and is intended for general guidance only. It is not legal or tax advice specific to your situation.

If you have received a Code of Practice 9 letter, or if you are considering making a voluntary disclosure, the most important step is to contact a qualified tax specialist without delay. The 60-day window runs from the date of HMRC’s letter, not the date you open it.

Received a Code of Practice 9 letter?

Time is critical. The 60-day window runs from the date on HMRC's letter. ARB Accountants has specialist experience in COP9 investigations and can guide you through the Contractual Disclosure Facility — from Outline Disclosure to contract settlement. ACCA-chartered. No jargon.

Frequently Asked Questions

What is Code of Practice 9?

Code of Practice 9 is HMRC's civil procedure for investigating suspected serious tax fraud. It operates through the Contractual Disclosure Facility, where a taxpayer who admits to deliberate fraud and makes a full and accurate disclosure receives immunity from criminal prosecution. It is the most serious civil tax investigation HMRC carries out.

What is Code of Practice 9 and who does it apply to?

HMRC Code of Practice 9 applies to individuals, company directors, trustees, and business owners where HMRC suspects deliberate behaviour has caused a loss of tax. It is issued by HMRC's Fraud Investigation Service and is entirely separate from routine compliance checks or Code of Practice 8 avoidance investigations.

What happens when I receive a COP9 letter?

You have 60 days to respond. You must either accept the Contractual Disclosure Facility by admitting fraud and providing an Outline Disclosure, or reject it and face HMRC's independent investigation. Specialist advice should be sought as soon as the letter arrives.

Can I request Code of Practice 9 before HMRC contacts me?

Yes. If you know you have committed tax fraud, you can submit form CDF1 to HMRC to request entry into the Code of Practice 9 process voluntarily. Unprompted disclosures attract lower penalties than those triggered by HMRC opening an investigation.

How far back can HMRC investigate under COP9?

Where deliberate fraud is identified, HMRC can review up to 20 years of your tax affairs. The actual scope depends on the nature and extent of the deliberate conduct and the availability of records.

What penalty level applies under Code of Practice 9?

Penalties can reach up to 200% of the tax lost, particularly for deliberate offshore conduct. The exact level depends on the quality of the disclosure, the degree of cooperation, and whether the disclosure was unprompted. COP9 specialists will argue for the minimum applicable penalty given your specific facts.

What is the difference between Code of Practice 9 and a criminal investigation?

A Code of Practice 9 investigation is civil in nature. HMRC's focus is recovering unpaid tax and charging financial penalties. A criminal investigation aims at securing a prosecution and can result in a prison sentence. Accepting the Contractual Disclosure Facility provides immunity from criminal prosecution for matters that are fully and accurately disclosed.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008