How to Do Accounts for Small Business: A Practical UK Guide

If you run a small business, keeping on top of your accounts is one of the most important things you can do and one of the most neglected. Most business owners we speak to say the same thing: they know accounting matters, but they have no idea where to start or how much they actually need to do.

Knowing how to do accounts for small business does not have to be complicated. The basics are manageable, and once you have a solid system in place, staying on top of your finances becomes part of the routine rather than a monthly panic.

This guide walks you through everything you need to know about small business accounting in the UK. From choosing how to record your transactions to understanding your tax obligations, you will find practical steps you can act on today, along with guidance on when it makes sense to bring in professional support.

What Does Accounting for a Small Business Actually Involve?

Accounting for a small business covers more than just filing a tax return once a year. It is an ongoing process that helps you understand how your business is performing, meet your obligations to HMRC, and make better financial decisions.

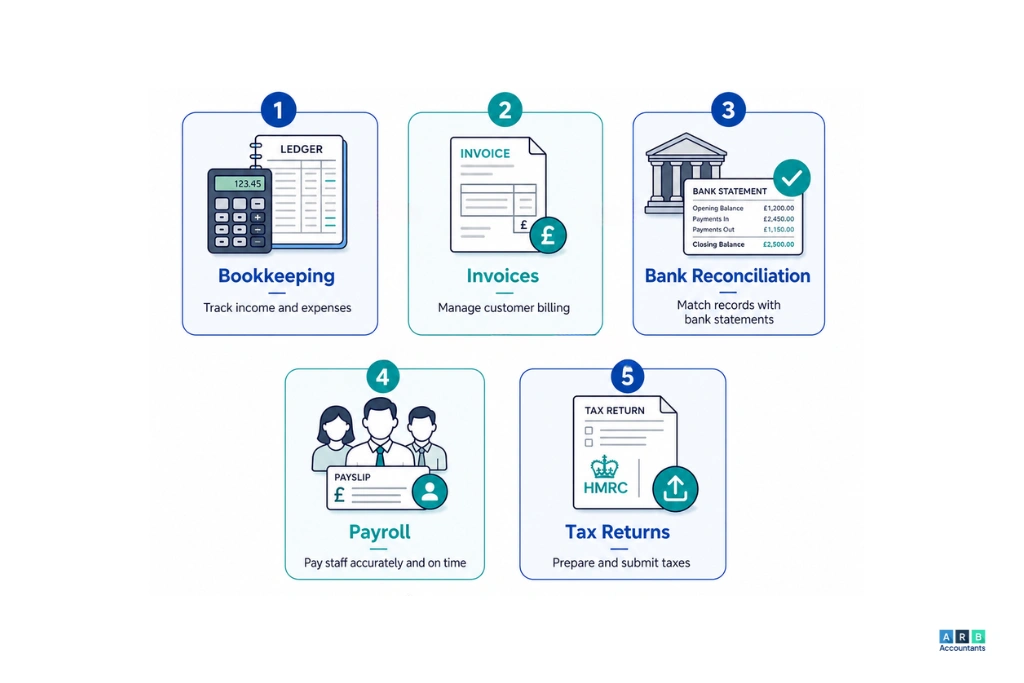

The core activities that sit under small business accounting include:

- Recording income and expenses as they happen

- Keeping receipts, invoices, and bank statements organised

- Reconciling your records against your bank account regularly

- Managing payroll if you employ staff

- Tracking what you owe suppliers and what customers owe you

- Preparing financial reports such as profit and loss statements

- Filing tax returns and paying tax on time

The scope of what you need to do will depend on your business structure. A sole trader working alone has simpler obligations than a limited company with employees. But the fundamentals of good accounting for small businesses apply across the board.

Bookkeeping vs Accounting: What Is the Difference?

These two terms get used interchangeably, but they describe different things.

Bookkeeping is the day-to-day task of recording your financial transactions. Every sale you make, every expense you pay, every invoice you raise, these all get logged as part of bookkeeping. It is the foundation that everything else builds on.

Accounting takes that data and turns it into something meaningful. An accountant analyses your records, prepares financial statements, calculates your tax liability, and gives you strategic advice about your business finances.

In practice, many small business owners handle bookkeeping themselves and bring in an accountant for the higher-level work. Our bookkeeping service is designed for business owners who want that day-to-day admin handled properly without taking it off their desk themselves.

How to Do Accounts for Small Business: The Essential Steps

The best way to approach accounting for a small business is to build good habits from the start. Here is a straightforward process that works for most small businesses.

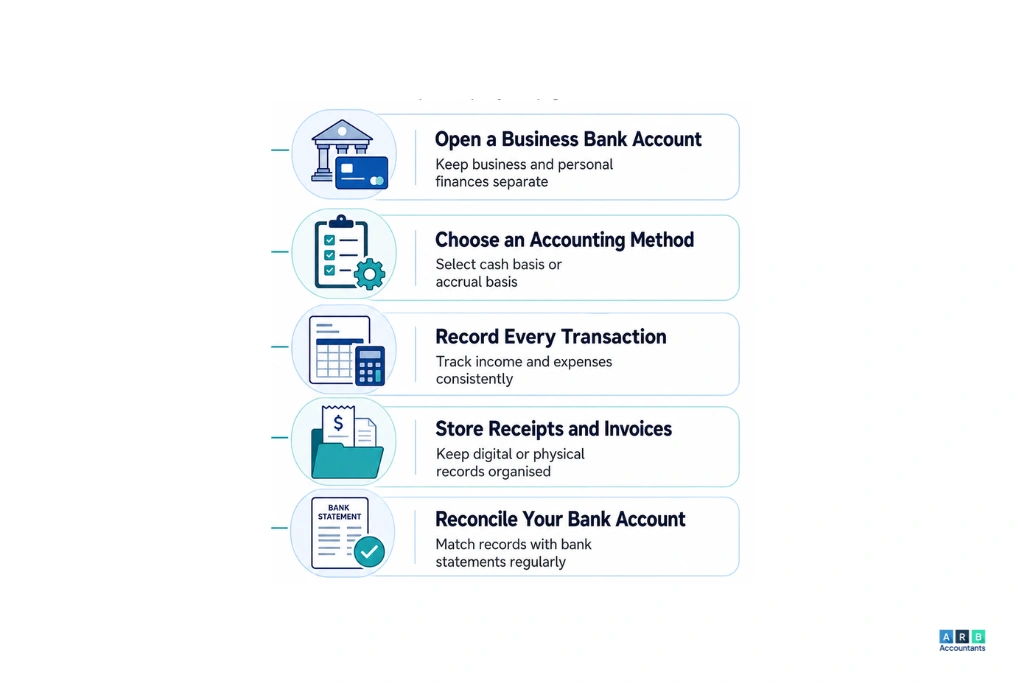

Step 1: Open a Dedicated Business Bank Account

This is the single most important first step, and many small business owners skip it. Mixing personal and business transactions makes everything harder, your bookkeeping takes longer, your tax return becomes more complicated, and HMRC has less clarity about your business activity.

Open a separate account for your business from day one. Use it exclusively for business income and expenses. This one change alone makes how to do small business accounts significantly simpler.

Limited companies are legally required to have a business bank account. Sole traders are not, but the practical benefits make it well worth doing regardless.

Step 2: Choose Your Accounting Method

There are two main approaches to small business accounting UK business owners use.

Cash basis accounting records income when you receive it and expenses when you pay them. It is simpler, and HMRC allows most small businesses and sole traders to use it. If you are just starting out, this is usually the more straightforward option.

Accrual (traditional) accounting records income when it is earned and expenses when they are incurred, regardless of when money changes hands. It gives a more accurate picture of your financial position over time, which is why it is required for limited companies and businesses above a certain size.

Most small sole traders and early-stage limited companies start with cash basis. As your business grows and your finances become more complex, you may need to switch.

Step 3: Set Up a System for Recording Transactions

Every payment you receive and every expense you pay needs to be recorded. This is non-negotiable, both for your own awareness and for HMRC compliance.

You have a few options here:

Spreadsheets work for very small businesses with a low volume of transactions. They are free and flexible, but manual, prone to errors, and hard to scale.

Accounting software is the better long-term option for most businesses. Tools like Xero, QuickBooks, and FreeAgent connect directly to your business bank account, categorise transactions automatically, and generate reports at the click of a button. They also make it easier to stay compliant with Making Tax Digital (MTD), which requires digital record-keeping for VAT-registered businesses.

The key principle is consistency. Pick a system, stick to it, and update it regularly. Leaving your bookkeeping for three months and then trying to reconstruct it from memory is one of the most common problems we see which leads to errors that cost money.

Step 4: Keep All Receipts and Invoices

HMRC can ask to see your records at any time, so you need to hold onto evidence for every transaction. That means:

- Receipts for every business expense you plan to claim

- Copies of every invoice you raise to customers

- Bank statements

- Payroll records if you have employees

- VAT records if you are VAT registered

Most accounting software lets you photograph receipts and attach them directly to transactions, which makes record-keeping much easier. HMRC generally requires you to keep business records for at least five years after the relevant Self Assessment filing deadline, and six years for limited companies.

Step 5: Reconcile Your Accounts Regularly

Bank reconciliation means checking that your accounting records match your actual bank statements. You do this by going through each transaction on your bank statement and confirming it appears correctly in your records.

It sounds tedious, but it catches errors early, a duplicate transaction, a missing payment, a subscription you forgot you were paying. Most business owners do this monthly. With accounting software and bank feeds, it takes a fraction of the time it used to.

Understanding Your Tax Obligations as a Small Business

Tax is the part of small business accounting UK owners most often get wrong. Not because the rules are impossible to follow, but because deadlines creep up and obligations differ depending on your business structure.

Sole Traders

If you are self-employed, you pay Income Tax and National Insurance through Self Assessment. You need to register with HMRC as self-employed, file a tax return each year by 31 January, and pay any tax owed by the same deadline.

You can deduct allowable business expenses from your income to reduce your tax bill. Our guide to sole trader expenses covers what you can and cannot claim. Getting this right is one of the biggest areas where people either miss out on legitimate deductions or accidentally claim things they should not.

Limited Companies

Limited companies pay Corporation Tax on their profits, currently at 19% for profits up to £50,000 (with marginal relief between £50,000 and £250,000, and 25% for profits above £250,000 as of the 2025–26 tax year). You need to file annual accounts with Companies House and a Company Tax Return with HMRC within nine months of your accounting year end.

If you are a director taking a salary and dividends, you will also need to file a personal Self Assessment return. Our Self Assessment service handles the full process for business owners who want this done correctly.

VAT

If your taxable turnover exceeds £90,000 in any rolling 12-month period, you must register for VAT. Once registered, you charge VAT on eligible sales, reclaim VAT on business purchases, and file regular VAT returns with HMRC.

VAT registration also brings Making Tax Digital obligations, which require you to keep digital records and file returns using MTD-compatible software. These rules are also expanding to cover income tax for self-employed individuals and landlords under MTD for ITSA, so it is worth understanding what is coming even if you are not yet VAT registered. Our MTD for ITSA guide explains what is changing and when.

Small Business Accounting Tips to Keep Things Under Control

SMB accounting does not need to be overwhelming if you build the right habits. Here are some small business accounting tips that make a real difference.

Do your bookkeeping little and often. Setting aside 30 minutes each week is far more manageable than facing a backlog at the end of the quarter. Regular bookkeeping means your numbers are always current, so you can spot issues before they become expensive.

Separate business and personal finances from day one. Even if you are a sole trader with no legal obligation to have a business account, mixing the two creates unnecessary complexity. Keep things clean from the start.

Set aside money for tax as you go. A common mistake is spending income without accounting for the tax you will owe on it. A simple rule of thumb for sole traders is to put 20-30% of your profit aside in a separate savings account throughout the year. That way, your January tax bill does not come as a shock.

Understand what you can claim. Many business owners claim too little and pay more tax than they should. Allowable expenses can include home office costs, travel, equipment, professional subscriptions, and more. Getting accounting advice for small business from a qualified accountant early on can help you claim everything you are entitled to.

Keep your records for the required period. Losing records is not an excuse HMRC accepts. For sole traders, keep records for at least five years after the January filing deadline for the relevant tax year. For limited companies, that period is six years.

Common Mistakes in Small Business Accounting and How to Avoid Them

Most of the accounting problems we see at ARB are avoidable. Here are the ones that come up most often.

Leaving everything until year-end. Accounting is not a once-a-year job. Businesses that only look at their finances when the deadline is looming always end up stressed, under-informed, and sometimes facing unexpected bills.

Not reconciling bank accounts. If your records do not match your bank statements, you are working with inaccurate data. Decisions made on inaccurate data cost money.

Confusing turnover with profit. Your turnover is what comes in. Your profit is what remains after expenses and tax. A lot of small businesses look healthy on paper until the tax bill arrives and reveals the reality.

Missing the VAT threshold. If your turnover creeps past £90,000 without you noticing, you can face backdated VAT liabilities. Track your rolling 12-month turnover regularly so you know where you stand.

Claiming personal expenses as business costs. HMRC takes a dim view of this, and the line between legitimate business expenses and personal spending is something a good accountant can help you draw clearly.

How to Do Accounts for Small Business with Professional Support

There is no rule that says you must handle all of this yourself. For many small business owners, getting professional accounting advice for small business is one of the best investments they can make.

A good accountant does more than just file your tax return. They help you understand your numbers, identify tax-saving opportunities, keep you on the right side of HMRC, and give you confidence in the decisions you make. Most business owners who switch to working with an accountant say they wish they had done it sooner.

The key question is not whether you need an accountant, but how much support you need at your current stage. Some businesses benefit from full-service support covering bookkeeping, payroll, VAT, and accounts preparation. Others just need an accountant to step in at year-end and handle the compliance work.

Our small business accounting service is built around the needs of growing businesses. We work with sole traders, limited company directors, and SME owners across Essex and the surrounding areas. Whether you want to hand over your bookkeeping entirely or just have someone review your setup and give you ongoing peace of mind, we can help.

Ready to Get Your Small Business Accounts in Order?

Getting how to do accounts for small business right from the start saves time, reduces stress, and keeps you on the right side of HMRC. Whether you are just starting out or you have been going for years with a system that is not quite working, the right support makes a real difference.

ARB Accountants works with small business owners across Essex and beyond, from sole traders taking on their first tax return to growing limited companies that need ongoing strategic support. As experienced accountants in Essex, we understand the practical realities of running a small business and how much it helps to have a reliable team behind you.

Get in touch to find out how we can support your business.

Frequently Asked Questions

What does it mean to do accounts for a small business?

Doing accounts for a small business means recording all your income and expenses, keeping financial records organised, reconciling your bank statements, and meeting your tax obligations with HMRC. It covers day-to-day bookkeeping as well as the formal preparation of annual accounts and tax returns.

How to do accounting for small business if you have no experience?

Start with a business bank account, choose an accounting method, and use accounting software to record transactions as they happen. Many sole traders manage their own bookkeeping successfully using tools like Xero or QuickBooks. For tax returns and more complex matters, most find it worthwhile to work with a professional accountant to make sure everything is accurate and compliant.

What records do I legally need to keep for my small business?

Sole traders need to keep business records for at least five years after the 31 January filing deadline for the relevant tax year. Limited companies must retain accounting records for six years from the end of the financial year they relate to. Records include bank statements, receipts, invoices, payroll records, and VAT records where applicable.

When do I need to register for VAT as a small business?

You must register for VAT when your taxable turnover exceeds £90,000 in any rolling 12-month period (correct as of the 2025–26 tax year, though thresholds can change). You can also choose to register voluntarily before this point, which may make sense if you buy a lot from VAT-registered suppliers and want to reclaim the VAT.

How much does it cost to hire an accountant for a small business?

This varies depending on the scope of work and the size of your business. Basic self-assessment and year-end accounts for a sole trader can start from a few hundred pounds annually. More comprehensive support for a limited company, including bookkeeping, payroll, VAT returns, and accounts preparation, typically runs from around £1,000 to several thousand pounds per year. Most businesses find this cost is offset by tax savings and time saved.

What is the difference between simple accounting for small business and full accounting?

Simple accounting for small business usually refers to cash basis bookkeeping, where you record income when received and expenses when paid, and keep straightforward records. Full or traditional accounting uses accrual principles, recognises income and expenses when they occur rather than when cash moves, and produces a more complete financial picture. Limited companies are generally required to use accrual accounting.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008