Skip to content

Skip to content

Can You Sell Gold and Silver Without Reporting to HMRC?

Last updated:

March 26, 2026

A lot of people buying and selling gold and silver in the UK assume HMRC is watching every transaction. The reality is more nuanced, and far more favourable than most people expect. If you want to know how much gold can you buy without reporting UK rules require you to disclose, the short answer is: quite a lot, and in some cases, there is no reporting obligation at all.

The UK tax rules on precious metals are actually among the most investor-friendly in the world, thanks to a combination of VAT exemptions, Capital Gains Tax allowances, and a special CGT-free status for certain Royal Mint coins. Questions about how much gold can you buy without reporting UK thresholds set, and what tax applies when selling gold UK, come up regularly among investors who want to stay compliant without paying more than they need to.

This guide breaks down everything you need to know: which products are tax-free, how the CGT allowance works, when you must tell HMRC about a sale, and how to structure your precious metals investments in a way that keeps your tax position as clean as possible.

How Much Gold Can You Buy Without Reporting UK?

There is no legal requirement to report gold purchases to HMRC, regardless of the amount. If you want to understand how much gold can you buy without reporting UK authorities will scrutinise, the answer is that the purchase itself is not the trigger. The tax liability on any profit you later make when selling is what matters.

You can own as much gold as you like. There is no cap on how much gold can you own UK rules impose on private individuals. HMRC does not require you to declare a gold purchase or register your holdings.

That said, bullion dealers have their own reporting obligations under anti-money laundering (AML) rules. Dealers carry out identity checks on customers making purchases over £5,000, or cumulative purchases exceeding £10,000 within a 12-month period. Cash transactions above £10,000 also trigger mandatory checks. These are compliance checks on the dealer, not a tax reporting requirement on you as the buyer. Dealers retain transaction records for at least five years and share them with HMRC only if formally requested.

So when it comes to how much gold can you buy without reporting UK requirements demand, the simple position is this: buying gold does not trigger an automatic HMRC report. The tax question only arises when you sell at a profit. Whether you are selling gold to UK an online dealer or to a private buyer, it is the gain on that sale that creates any potential HMRC obligation.

READ RELATED ARTICLE: How Likely Are You to be Investigated by HMRC?

Do You Pay Tax on Gold in the UK?

Do you pay tax on gold UK? The answer depends entirely on what type of gold you are selling. Not all gold is treated the same under HMRC rules, and getting this distinction right can mean the difference between a tax-free gain and a CGT liability.

Understanding how much gold can you buy without reporting UK investors are obliged to disclose starts with understanding CGT itself. Capital Gains Tax (CGT) is the tax that applies when you sell an asset for more than you paid for it. HMRC charges CGT on the gain, not the total sale amount. If you bought a gold bar for £5,000 and sold it for £7,000, your gain is £2,000, and that is what is assessed for tax purposes.

For the 2024/25 and 2025/26 tax years, every individual has an annual CGT tax-free allowance of £3,000. If your total gains from all chargeable assets across the tax year stay below £3,000, you owe no CGT and have no reporting obligation to HMRC.

CGT Rates on Gold

If your gains exceed the £3,000 allowance, the taxable portion is added to your income and taxed at the following rates, following changes introduced in the Autumn 2024 Budget:

- Basic-rate taxpayers: 18% on gains above the allowance

- Higher-rate taxpayers: 24% on gains above the allowance

These rates changed in October 2024. Before that date they were 10% and 20% respectively. If you are planning a sale and want to understand the likely CGT charge, do you pay tax on gold matters a great deal here, and the updated rates are worth factoring into your calculations.

UK Legal Tender Coins: The CGT Exemption

Here is where things get genuinely useful for UK investors. Gold coins produced by the Royal Mint and classified as UK legal tender are completely exempt from CGT. The legal basis for this is TCGA92/S21(1)(b), which states that sterling is not an asset for CGT purposes. Because HMRC cannot tax gains made from selling its own legal currency, these coins carry an unlimited CGT exemption.

The CGT-exempt coins include:

- Gold Britannias

- Gold Sovereigns (minted from 1837 onwards)

- Queen’s Beasts gold coins

- Tudor Beasts gold coins

- Other Royal Mint legal tender gold series

You can make an unlimited profit on any of these coins and pay zero CGT. There is no cap on the amount you sell or the gain you realise. This makes buying and selling gold in the form of Royal Mint legal tender coins one of the most tax-efficient investment strategies available to UK individuals.

Foreign gold coins, including Krugerrands, American Gold Eagles, Canadian Maple Leafs, and Australian Kangaroos, do not benefit from this exemption. They are treated as standard chargeable assets.

HMRC Gold Rules: What About Gold Bars?

The hmrc gold rules for gold bars are straightforward. All gold bars are chargeable assets for CGT purposes, regardless of purity or weight. This applies to every size, from 1g bars to 1kg bars.

When selling gold UK in bar form, you must calculate your gain, apply your £3,000 annual allowance, and pay CGT at 18% or 24% on any excess. Report the gain through Self Assessment or via HMRC’s online Capital Gains Tax reporting service. Investors asking how much gold can you buy without reporting UK sometimes focus too much on the purchase side: the reporting obligation sits firmly with the sale.

Here is a practical example. Suppose you buy a gold bar for £8,000 and sell it later for £11,500. Your gain is £3,500. After the £3,000 CGT allowance, £500 is taxable. As a basic-rate taxpayer, you would owe 18% of £500, which is £90. That is not a ruinous tax bill, but you do need to report it.

Where the HMRC gold rules get more complex is if you have made multiple disposals in the same tax year. The £3,000 allowance covers your total gains from all chargeable assets combined, not just gold. If you also sold shares, crypto, or other assets and made gains, all of it counts against your single annual allowance.

A common situation we see with clients is that they sell a modest amount of gold bars, assume their gain is below the threshold, and miss the fact that other asset disposals have already used up most of their allowance. Keeping a running total of your gains across all assets throughout the tax year helps you avoid that mistake.

How Much Gold Can You Buy Without Reporting UK: The VAT Position

When it comes to how much gold can you buy without reporting UK on the purchase side, VAT is worth understanding separately from CGT. The two taxes work very differently.

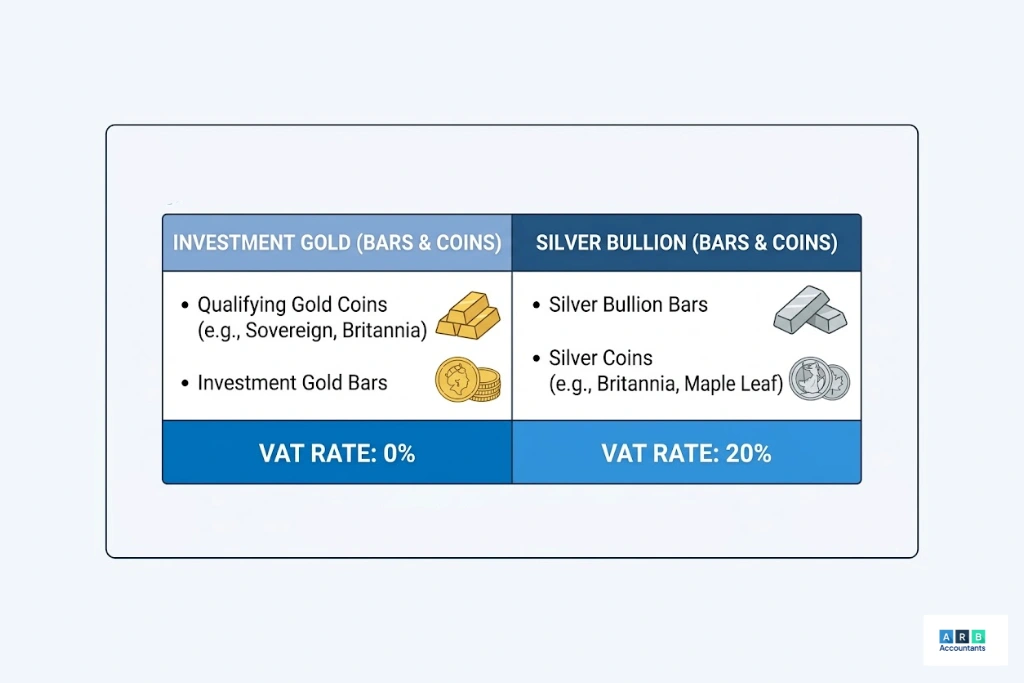

Investment-grade gold is exempt from VAT in the UK. This has been the case since 1 January 2000, when the UK aligned with EU legislation to remove VAT from investment gold. Under HMRC’s VAT Notice 701/21A, investment gold covers:

- Gold bars and wafers of at least 99.5% purity traded in weights accepted by the bullion markets

- Gold coins with at least 90% purity, minted after 1800, that have been or are legal tender in their country of origin and are normally sold at no more than 180% of their gold content value

When you buy Gold Britannias, Gold Sovereigns, or investment-grade gold bars, you pay no VAT. The price you pay is simply the market price of the gold. This zero-VAT position is a significant advantage for UK investors and is one reason why selling gold remains a more straightforward tax proposition than silver.

Silver is a different story, as we cover in the next section. Silver is subject to 20% VAT on purchase, and this has a significant impact on how investors approach the silver market.

Selling Silver UK: What Are the Tax Rules?

Selling silver UK attracts different treatment depending on the product type, and there is an important VAT consideration that does not apply to gold.

VAT on Silver

All physical silver, including silver bars and silver coins, is subject to 20% VAT in the UK when purchased. This applies regardless of purity and regardless of whether the coin is a Royal Mint product or a foreign issue. Even Silver Britannias carry 20% VAT on purchase, though they have a specific advantage when it comes to CGT.

The VAT position matters for investors because your silver needs to increase in value by at least 20% just to break even. For this reason, many investors treat silver as a longer-term holding, waiting until price movement more than offsets the initial VAT cost.

CGT on Silver

Is silver tax free UK? The answer depends on which products you hold.

Silver Britannia coins produced by the Royal Mint are classified as UK legal tender, exactly like their gold counterparts. They benefit from the same CGT exemption that applies to Gold Britannias and Sovereigns. You can sell Silver Britannias at any profit, in any quantity, and pay zero CGT. This is the key advantage that makes selling silver coins UK, specifically Royal Mint coins, particularly tax-efficient at the point of sale.

Silver bars and non-UK silver coins, including American Silver Eagles and Canadian Silver Maple Leafs, are chargeable assets. Capital gains tax on silver UK applies to any gains above the £3,000 annual allowance on these products. If you have held a collection of silver bars for several years and the silver price has risen substantially, the gain on disposal could be meaningful and will need to be reported and taxed accordingly.

The best way to sell silver UK from a tax standpoint is to hold Silver Britannias or other Royal Mint legal tender coins. You lose the VAT advantage on purchase compared with investment gold, but you recover a full CGT exemption on the way out. For larger investors planning to hold silver long term, this is the most tax-efficient structure available.

Many silver investors ask us: Is it better to hold Silver Britannias or silver bars? For UK tax purposes, the answer comes down to whether CGT efficiency at the point of selling silver coins UK outweighs the premium you pay for Royal Mint products. For most long-term holders, it does.

Do I Have to Declare Gold to HMRC?

Do I have to declare gold to HMRC? The reporting obligation depends on two separate triggers, and both are worth understanding clearly.

Trigger 1: Your taxable gains exceed £3,000. If you sell gold, silver, or any other chargeable assets in a tax year and your total gains above the allowance are positive, you must report and pay CGT. Do this through either your annual Self Assessment tax return or HMRC’s online CGT service if you are not otherwise in Self Assessment. The filing deadline for Self Assessment is 31 January following the tax year end.

Trigger 2: Your total disposal proceeds exceed £50,000. Even if your gains are below the £3,000 allowance, if total sale proceeds from all asset disposals in the tax year exceed £50,000, you must complete the CGT pages on your Self Assessment return. This catches higher-value investors who sell significant quantities of gold or silver, even where the overall gain is modest due to a high original purchase cost.

It is worth repeating: you do not need to declare individual gold purchases. HMRC does not want a report every time someone buys a Sovereign. The reporting obligation only arises on the sale side when one of these thresholds is crossed.

Failing to report a taxable gain can lead to penalties, interest on unpaid tax, and in serious cases, an HMRC investigation. If you are buying and selling gold regularly and your annual disposals approach or exceed £50,000, making sure you are on Self Assessment and keeping thorough records is not optional.

READ RELATED ARTICLE: How to Make a HMRC Voluntary Disclosure?

Capital Gains Tax on Gold UK: How to Reduce Your Liability

There are several straightforward and entirely legal approaches to reducing capital gains tax on gold UK. Knowing how much gold can you buy without reporting UK is one part of the picture; knowing how to structure your disposals efficiently is the other.

Buy CGT-exempt coins. The most direct approach is to focus your gold and silver holdings on Royal Mint legal tender coins. Gold Britannias, Gold Sovereigns, and Silver Britannias are all CGT-free on disposal regardless of the gain. This is the single most effective way to structure a precious metals portfolio for UK investors.

Use your annual CGT allowance. If you hold chargeable gold assets such as bars or foreign coins, you can spread disposals across multiple tax years to stay within the £3,000 annual allowance each year. Selling a portion of your holdings each year rather than everything at once lets you realise gains tax-free over time.

Use your spouse or civil partner’s allowance. Each individual has their own separate £3,000 annual CGT allowance. Transferring assets between spouses or civil partners does not trigger CGT, so jointly held portfolios can effectively benefit from up to £6,000 of tax-free gains per year.

Offset losses. If you have made losses on other chargeable assets in the same tax year, offset those against your gold gains to reduce your overall taxable position. Capital losses can also be carried forward to future tax years if reported to HMRC, even in years when you have no gains to offset.

Keep meticulous records. When calculating your gain on selling gold, you can deduct allowable costs from the sale price, including the original purchase price, dealing fees, and reasonable storage costs. Thorough record-keeping from the date of purchase makes this straightforward and can reduce your taxable gain materially.

READ RELATED ARTICLE: How to Pay Capital Gains Tax Online After Sale

How Much Gold Can You Own UK and What Are the Inheritance Tax Implications?

How much gold can you own UK? There is no limit. Private individuals can hold as much gold and silver as they wish with no obligation to register holdings or report them to any authority.

However, gold and silver holdings do not escape Inheritance Tax (IHT). When someone passes away, the value of their estate including precious metals is assessed for IHT purposes. The nil-rate band is currently £325,000, with an additional residence nil-rate band of up to £175,000 when a property is left to direct descendants.

Gold and silver above these thresholds form part of the taxable estate. The standard IHT rate is 40% on the value above the nil-rate band. Unlike CGT-exempt Royal Mint coins, there is no special IHT exemption for precious metals.

Some investors gift gold or silver coins while still alive as part of broader estate planning. Gifts made more than seven years before death are generally outside the scope of IHT under the potentially exempt transfer rules. This is a complex area and personalised tax advice is strongly recommended before making significant gifting decisions.

Need Help With Your Gold and Silver Tax Position?

The tax rules around buying and selling gold are more straightforward than most people expect, but they do require careful attention to which products you hold and how much you are disposing of each year. The distinction between CGT-exempt Royal Mint coins and chargeable assets like bars and foreign coins is critical, and getting it wrong can mean unexpected tax bills or missed reporting obligations.

If you have built up a significant precious metals portfolio, or if your total annual disposals are approaching the reporting thresholds, it is worth having a qualified accountant review your position before you sell. The team at ARB Accountants, trusted accountants in Essex, can help you understand your CGT exposure, structure disposals to use your annual allowances effectively, and make sure your Self Assessment return reflects everything correctly. You can learn more about our tax advice service and how we can help you stay on the right side of HMRC.

If you are already in Self Assessment and need help ensuring your capital gains are reported correctly, take a look at our self-assessment service. Tax rules can change, and figures in this article are correct for the 2024/25 and 2025/26 tax years. Always seek personalised advice for your specific situation.

Frequently Asked Questions

How much gold can you buy without reporting to HMRC in the UK?

How much gold can you buy without reporting to HMRC in the UK?

There is no limit on how much gold can you buy without reporting to HMRC. Purchasing gold does not trigger a tax reporting obligation. Bullion dealers carry out identity checks on transactions over £5,000 and cumulative purchases over £10,000 within a 12-month period, but these are the dealer’s anti-money laundering obligations rather than a personal tax reporting requirement. Tax reporting only arises when you sell gold and make a gain above the annual CGT allowance of £3,000, or when your total disposal proceeds in a tax year exceed £50,000.

Do you pay tax on gold UK when you sell it?

Do you pay tax on gold depends on the type of gold. Royal Mint legal tender coins, including Gold Britannias and Gold Sovereigns minted from 1837 onwards, are completely exempt from Capital Gains Tax regardless of the profit made. Gold bars and foreign coins are chargeable assets, and any gain above the £3,000 CGT allowance is taxable at either 18% (basic-rate taxpayers) or 24% (higher-rate taxpayers) following the October 2024 Budget changes.

Is silver tax free in the UK?

Is silver tax free uk depends on the specific product. Silver Britannia coins produced by the Royal Mint are classified as UK legal tender and are fully exempt from Capital Gains Tax, so you can sell them at any profit without paying CGT. Silver bars and non-UK silver coins are chargeable assets and CGT applies to gains above the annual allowance. All silver, including Silver Britannias, is subject to 20% VAT on purchase in the UK.

Do I have to declare gold to HMRC?

Do I have to declare gold to HMRC? Only when you have a taxable gain or when total disposal proceeds in a tax year exceed £50,000. You do not need to notify HMRC of gold purchases. If your total capital gains from all chargeable assets in the year exceed £3,000, or if disposal proceeds across all assets exceed £50,000, you must report through Self Assessment or HMRC’s online CGT service. Failing to report a taxable gain can result in penalties and interest.

What is the best way to sell silver UK for tax purposes?

The best way to sell silver UK from a tax perspective is to hold Silver Britannia coins issued by the Royal Mint rather than silver bars or foreign coins. Silver Britannias are CGT-exempt as UK legal tender, meaning all profits on disposal are tax-free regardless of the amount. For silver bars and non-UK coins, spreading disposals across years to stay within your £3,000 annual CGT allowance reduces overall exposure. Offsetting capital losses from other assets can also lower the net taxable gain when selling silver coins UK.

What are the CGT rates on gold and silver for 2024/25?

Capital gains tax on gold UK for chargeable assets such as gold bars and foreign coins is charged at 18% for basic-rate taxpayers and 24% for higher-rate taxpayers for the 2024/25 tax year and beyond, following the October 2024 Autumn Budget. These rates replaced the previous 10% and 20%. Capital gains tax on silver UK follows the same rates for silver bars and non-exempt silver coins. Royal Mint legal tender coins remain completely CGT-free and these rates do not apply to them.