Skip to content

Skip to content

Buying a Van as a Sole Trader: Tax Benefits Explained

Last updated:

March 13, 2026

If you are thinking about buying a van as a sole trader, the good news is that HMRC treats commercial vehicles far more generously than cars for tax purposes. In many cases, you can deduct the full cost of the van from your taxable profits in the year you buy it, which can significantly reduce your Self Assessment tax bill.

This guide explains the tax relief on van purchase sole trader rules and the key tax benefits of buying a van as a sole trader in the UK, including how capital allowances for vans work, whether a van is 100% tax deductible, what HMRC requires, and how to handle mixed business and private use. Whether you are buying a van for business sole trader UK purposes for the first time or reviewing your current approach, this article gives you a clear picture of where you stand.

Table Of Contents

show

- Why Buying a Van as a Sole Trader Is Treated Differently to a Car

- Is a Van 100% Tax Deductible for a Sole Trader?

- How Van Capital Allowances Work for Sole Traders

- How Much Can I Claim for My Van If I Am Self-Employed?

- VAT on Van Purchases: What You Need to Know

- Common Mistakes to Avoid When Buying a Van as a Sole Trader

- A Final Word on Buying a Van as a Sole Trader

- Frequently Asked Questions

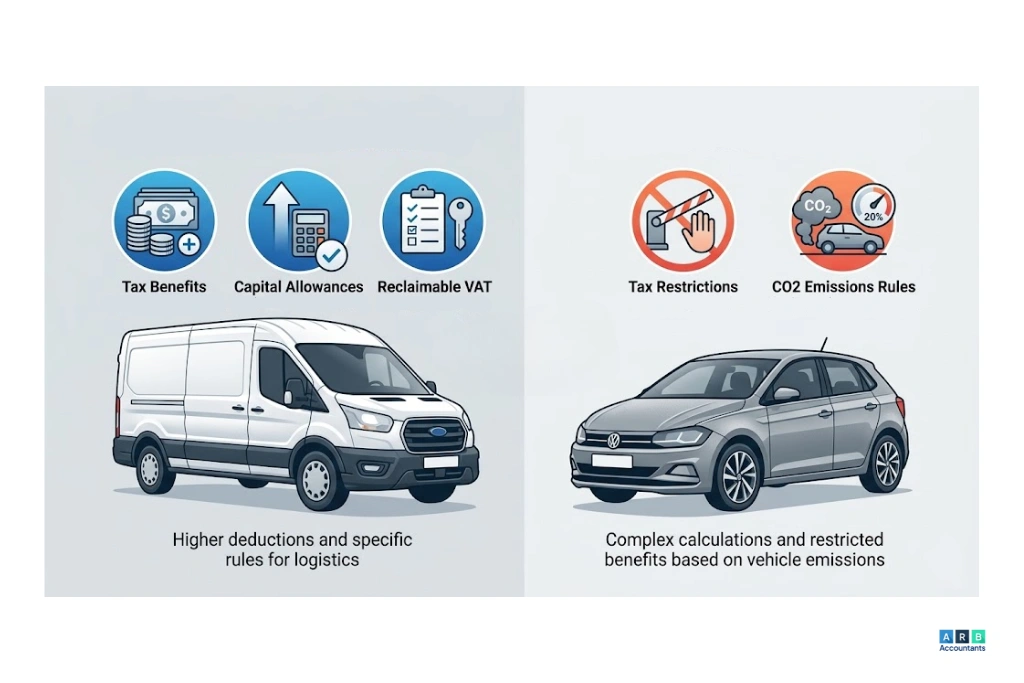

Why Buying a Van as a Sole Trader Is Treated Differently to a Car

The first thing to understand when considering a sole trader van purchase is that HMRC draws a clear distinction between vans and cars. Understanding the sole trader van purchase HMRC rules from the outset is important, as that distinction has a direct impact on how much tax relief you can claim.

HMRC defines a van as a goods vehicle primarily designed for transporting goods rather than passengers, with a payload of at least one tonne. Most panel vans, pick-up trucks, and light commercial vehicles used by tradespeople fall comfortably within this definition. Some vehicles sit in a grey area. Certain crew-cab models have been subject to reclassification in recent years, so it is always worth checking HMRC guidance for the specific vehicle you are considering.

Cars are subject to much stricter capital allowance rules based on CO2 emissions, and relief is typically spread over several years. Vans, by contrast, are classified as plant and machinery, which means they qualify for the Annual Investment Allowance and can often be deducted in full in the year of purchase.

Getting the vehicle classification right matters when buying a van as a sole trader. If HMRC reclassifies your van as a car, the allowances you claimed may be incorrect. If you are uncertain about a specific vehicle, speaking with a qualified accountant before you commit is a sensible step.

Is a Van 100% Tax Deductible for a Sole Trader?

For most sole traders who are buying a van as a sole trader, yes. The question of is a van 100 tax deductible sole trader is one of the most common we are asked. The answer comes down to two things: whether the van qualifies as a commercial vehicle under HMRC rules, and how much of its use is for business.

The Annual Investment Allowance (AIA) currently allows businesses to deduct up to £1,000,000 of qualifying capital expenditure in a single tax year, and vans purchased for business use qualify. If you spend £20,000 on a van used exclusively for work, you can deduct £20,000 from your taxable profits in that year.

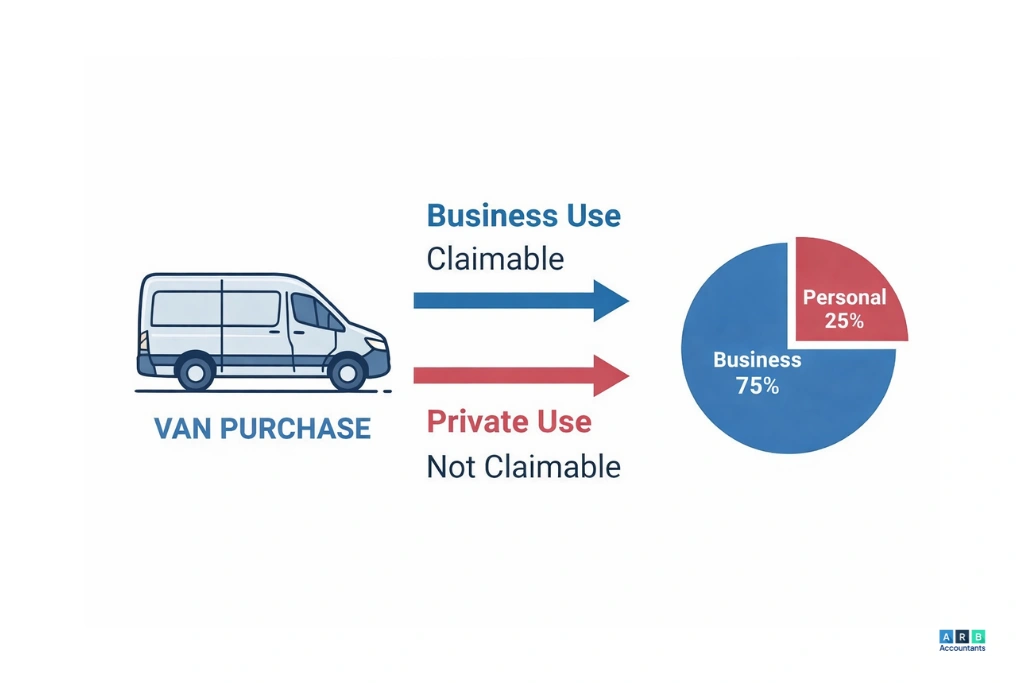

The key condition is business use. If the van is also used for private journeys, you can only claim the proportion of the cost that reflects business use. An 80/20 business-to-personal split means you claim 80% of the purchase price. This applies to both the capital allowances on the van purchase and any ongoing running costs.

This deduction is not automatic. You must actively claim it via your Self Assessment return in the accounting period you purchased the van. If you miss it, amending your return is possible but time-limited, and it is far easier to get it right from the start.

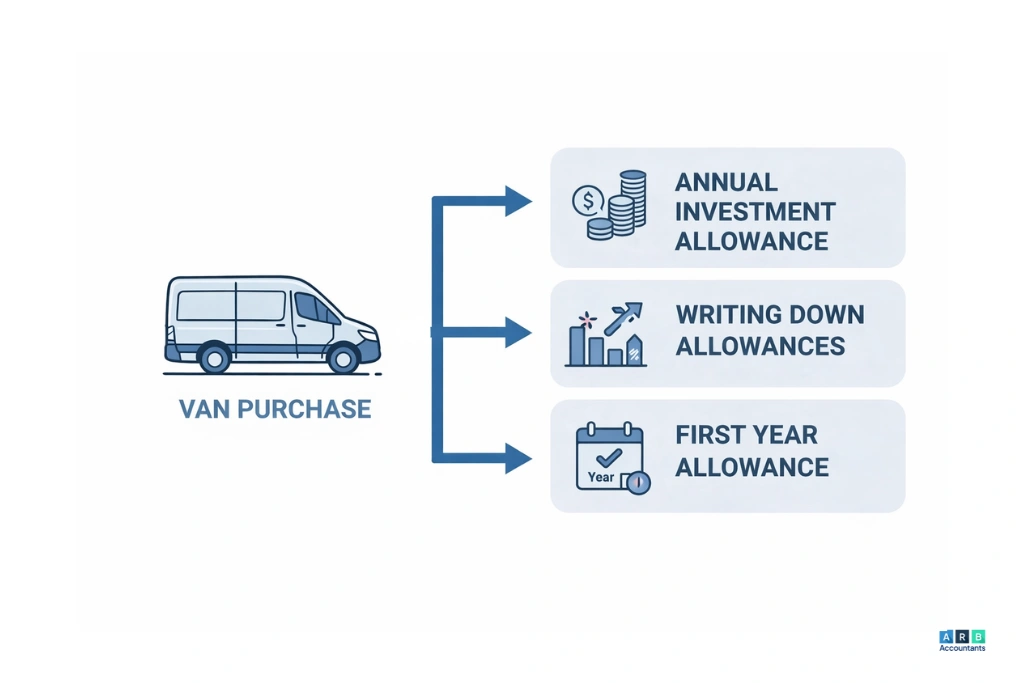

How Van Capital Allowances Work for Sole Traders

Capital allowances for vans are the formal tax mechanism that allows sole traders to recover the cost of purchasing a business vehicle. Claiming them correctly is the difference between getting maximum relief and leaving money on the table. Rather than treating the van as a simple day-to-day expense, capital allowances structure how and when you receive the tax relief.

For buying a van as a sole trader, there are three main routes.

Annual Investment Allowance

The Annual Investment Allowance is the most efficient option for most sole traders. It lets you deduct the full cost of the van (up to £1 million) from your taxable profits in the year you buy it. One advantage of annual investment allowance vans is that both new and used vehicles qualify.

For example: if your taxable profit is £55,000 and you buy a van for £18,000, your taxable profit falls to £37,000. At the basic rate of 20%, that is a tax saving of £3,600 in one year.

Writing Down Allowances

If you choose not to use the AIA, or have used your limit on other assets, vans fall into the main pool for Writing Down Allowances (WDA) at 18% per year on a reducing balance. Capital allowances on van expenditure claimed this way are recovered gradually rather than upfront. For most sole traders buying a van as a sole trader, the AIA is the more efficient route.

First Year Allowance for Zero-Emission Vans

If you purchase a new zero-emission van, a 100% First Year Allowance may apply regardless of your AIA position, allowing the full cost to be deducted in year one. This is increasingly worth factoring in when comparing electric options.

How Much Can I Claim for My Van If I Am Self-Employed?

How much can I claim for my van self-employed? The answer varies depending on your circumstances, but the key factors are the purchase price, the proportion of business use, how you acquired the van, and which allowance route you use.

Buying Outright

Purchase the van outright and use it 100% for business, and you can claim the full purchase price through the AIA in the same tax year, reducing your income tax and Class 4 National Insurance through Self Assessment.

Hire Purchase

With a hire purchase (HP) agreement, HMRC treats the transaction as a purchase from the date you start using the vehicle. You can claim capital allowances on the full value immediately, and the interest element of repayments may also be deductible.

Leasing

If you lease the van, you cannot claim van capital allowances on the vehicle. Instead, you deduct the lease rental payments as a business expense each year. For sole traders with limited cash flow, leasing can still make financial sense even if the tax position is less efficient than an outright purchase.

Mixed Business and Private Use

If you use the van for both business and personal journeys, you must reduce your capital allowances claim in proportion to private use. A mileage log from day one is the evidence HMRC will expect if your return is queried.

Van Running Costs You Can Also Claim

Buying a van as a sole trader does not only give you access to capital allowances on the purchase price. You can also claim the ongoing running costs as allowable expenses through your Self Assessment return, reducing your taxable profits further each year.

When you are buying a van as a sole trader, the claimable running costs typically include:

• Fuel (business proportion)

• Vehicle insurance

• Servicing, repairs and MOT fees

• Road tax and breakdown cover

• Interest on a finance agreement

Where the van is used partly for personal journeys, you can only claim the business share. HMRC also offers a simplified mileage rate as an alternative to tracking individual expenses. This is easier to administer but may produce a smaller deduction if your actual costs are high. Once you choose a method for a vehicle, you must stick with it.

READ RELATED ARTICLE: Sole Trader Expenses: What You Can and Can’t Claim

VAT on Van Purchases: What You Need to Know

If you are VAT-registered and buying a van as a sole trader, the VAT implications are more favourable than for cars. Unlike cars, the VAT on a commercial van can usually be reclaimed in full, provided the van is used solely for business. If there is any private use, only the business proportion of the VAT can be recovered.

For a VAT-registered sole trader using the van exclusively for work, this effectively reduces the true cost of the vehicle by 20%.

If your turnover is approaching the £90,000 registration threshold (2024-25), our guide to sole trader VAT registration explains what to consider before making a large purchase.

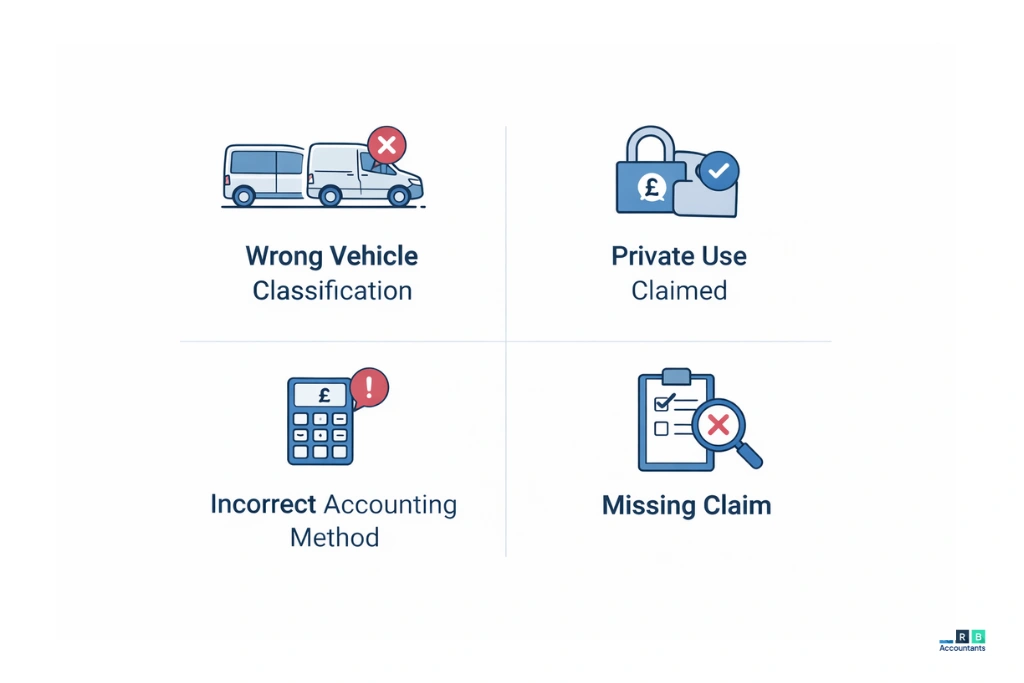

Common Mistakes to Avoid When Buying a Van as a Sole Trader

A small number of mistakes account for most of the errors we see when sole traders claim for a van purchase.

Misclassifying the vehicle

If you purchase a vehicle HMRC does not regard as a commercial van, you cannot access the AIA. Confirming the classification before purchase avoids an expensive surprise. This is one of the most important sole trader van purchase HMRC checks to carry out before you sign any paperwork.

Claiming 100% when there is private use

Commuting from home to a fixed workplace is not business use. If any element of your van use is personal, your claim must be adjusted accordingly.

Claiming through the wrong accounting basis

Sole traders on the cash basis treat the van’s cost as a straightforward expense; those on the accruals basis claim through the formal capital allowances regime. Getting this wrong produces errors in your Self Assessment return.

Missing the claim entirely

The tax relief on van purchase sole trader rules make clear the deduction does not apply automatically. You must claim it through your Self Assessment return.

Not planning the timing

Taking the full AIA in a low-profit year may not give maximum benefit. Spreading relief using writing down allowances can sometimes produce a better result.

READ RELATED ARTICLE: Can Capital Allowances Create a Loss?

A Final Word on Buying a Van as a Sole Trader

Buying a van as a sole trader is one of the most tax-efficient capital purchases available to a self-employed person in the UK. For anyone buying a van for business sole trader UK purposes, the combination of the Annual Investment Allowance, allowable running costs, and (where applicable) VAT recovery means the effective cost is considerably lower than the sticker price.

Understanding how much can I claim for my van self-employed starts with good records. The key steps are: confirm the vehicle qualifies under HMRC’s commercial vehicle definition, keep a mileage log from day one, choose the right capital allowance route, and claim accurately through your Self Assessment return.

If you are planning on buying a van as a sole trader or want to make sure an existing claim is correct, our accountants for sole traders are here to help. Our Southend accountants can also help you plan capital expenditure around your expected profits.

Tax thresholds and rates reflect HMRC guidance as of the 2025-26 tax year and may change. Always seek advice tailored to your specific situation.

Frequently Asked Questions

Does buying a van as a sole trader qualify for the Annual Investment Allowance?

Does buying a van as a sole trader qualify for the Annual Investment Allowance?

Yes. For anyone buying a van as a sole trader, annual investment allowance vans include any commercial vehicle meeting HMRC’s goods vehicle definition. The AIA lets you deduct the full purchase cost (up to £1 million) from your taxable profits in the year of purchase. Both new and used vans qualify.

Is a van 100% tax deductible for a sole trader?

Yes, provided the van qualifies as a commercial vehicle under HMRC rules. The question of is a van 100 tax deductible sole trader comes down to one variable: business use. If the van is used entirely for business, the full cost is deductible. Any private use reduces the deductible proportion. The claim must be made through your Self Assessment return and is not applied automatically.

What records does HMRC expect for a van?

Keep a mileage log showing journey dates, destinations, purposes, and distances. Retain your purchase invoice and any finance documents. If the van is used partly for personal journeys, your log must clearly separate business and private mileage.

Can I claim capital allowances on a second-hand van?

Yes. Capital allowances on van purchases under the AIA apply to both new and second-hand vehicles. The amount you paid is the figure used in your claim.

What happens when I sell the van?

When you sell a van on which you have claimed capital allowances, a balancing charge may apply if you sell for more than its tax written-down value. If you sell for less, you may be entitled to an additional deduction. Our Self Assessment service can help you handle the disposal correctly.

Why might claiming the full AIA not always be the best option?

There are situations where, even when buying a van as a sole trader, taking full tax relief in one year is not the most efficient approach. If profits are unusually low in the year of purchase, a large AIA deduction may exceed your taxable income. Spreading relief over multiple years using writing down allowances can produce a better result. Our post on why sole traders sometimes choose not to claim capital allowances goes deeper on this.