Skip to content

Skip to content

Pros and Cons of Buying Property Through a Limited Company (UK Guide)

Last updated:

March 12, 2026

Buying property through a limited company has become a widely discussed strategy among UK landlords, particularly after changes to mortgage interest tax relief altered the economics of buy to let ownership. Many investors now analyse whether limited company buying property offers a more sustainable structure for long term portfolio growth. Decisions often involve comparing corporation tax against personal income tax, evaluating buy to let ltd company mortgage products, and understanding how profits are managed within a corporate structure.

This guide explains the benefits and risks of buying property through a limited company, when investors choose to buy property through limited company or personally, and how professional structuring can affect long term returns. It also outlines how to buy property through a limited company in practical terms, including the steps required to set up a limited company to buy property. By understanding these mechanics, investors can better assess whether the benefits of setting up a limited company for property investment align with their strategy.

Table Of Contents

show

- What Does Buying Property Through a Limited Company Mean and Who Does It Suit?

- What Are the Pros of Buying Property Through a Limited Company?

- What Are the Cons of Buying Property Through a Limited Company?

- Should You Buy Property Through a Limited Company or Personally?

- How Do You Buy Property Through a Limited Company Step by Step?

- Why Do Investors Buy Commercial Property Through a Limited Company?

- What Risks and Mistakes Do Investors Make When Buying Property Through a Limited Company?

- Is Buying Property Through a Limited Company Worth It?

- Frequently Asked Questions

What Does Buying Property Through a Limited Company Mean and Who Does It Suit?

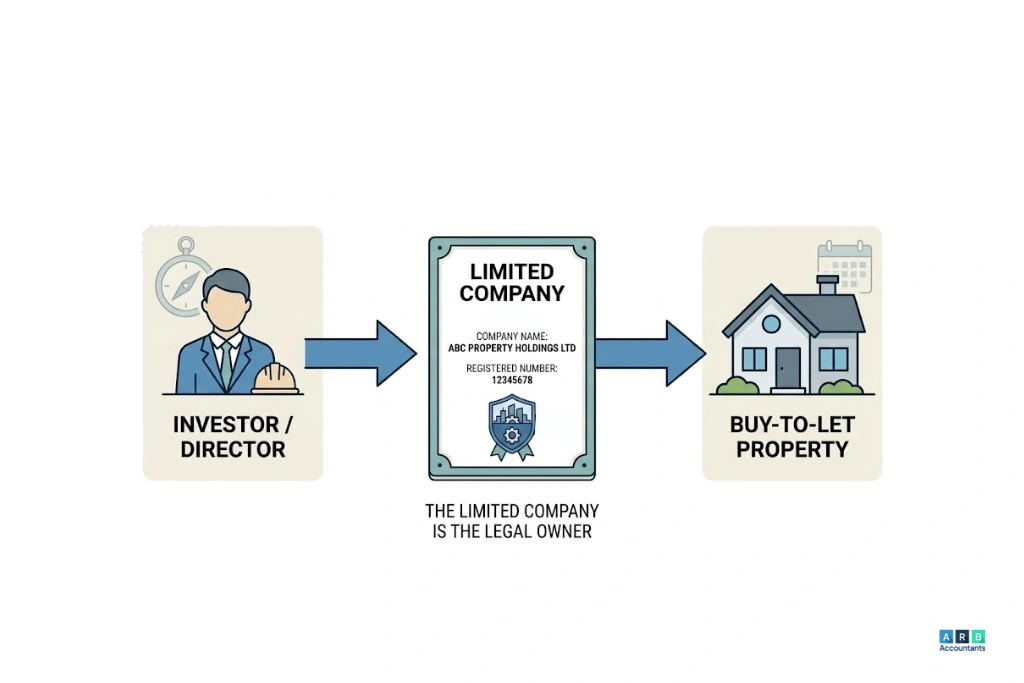

Buying property through a limited company means the company, rather than the individual investor, becomes the legal owner recorded at HM Land Registry. The investor typically acts as director and shareholder, meaning they control the company but do not personally hold the property asset. Profits generated from rent are taxed under corporation tax rules, which differs from the income tax treatment applied to individuals.

In practical terms, this structure often involves creating a property investment company, securing a buy to let ltd company mortgage, and operating the property through the company’s accounts. Investors frequently compare buy property through limited company or personally before deciding on structure. Research from the UK government shows that over 300,000 properties in England are owned by corporate landlords, reflecting the growing popularity of company structures among investors.

Can a Limited Company Buy a House in the UK?

Yes, a limited company can buy a house in the UK and register ownership through the Land Registry. Many investors ask can a limited company buy a house when evaluating whether to set up a limited company to buy property. The answer is yes, and the structure is commonly used in several scenarios.

Typical examples include:

- Residential buy to let investment properties financed with a buy to let ltd company mortgage

- Commercial property purchases held within a trading or investment company

- Property development companies acquiring land or housing stock for redevelopment

- Special Purpose Vehicles created specifically to hold rental property assets

Understanding how to buy property through a limited company usually begins with creating the company structure first, because lenders and conveyancing solicitors require a registered corporate borrower before the purchase process begins.

Who Typically Uses a Limited Company for Property Investment?

Limited company buying property is most common among investors building long term portfolios. Portfolio landlords often choose this structure when they expect to reinvest rental profits rather than withdraw them immediately.

Typical users include:

- Portfolio landlords expanding beyond a small number of properties

- Higher rate taxpayers seeking structured investment planning

- Investors reinvesting profits to acquire additional assets

These investors often weigh whether to buy property through limited company or personally before proceeding. For those pursuing multi property portfolios, the benefits of setting up a limited company for property investment are often linked to strategic growth rather than short term income extraction.

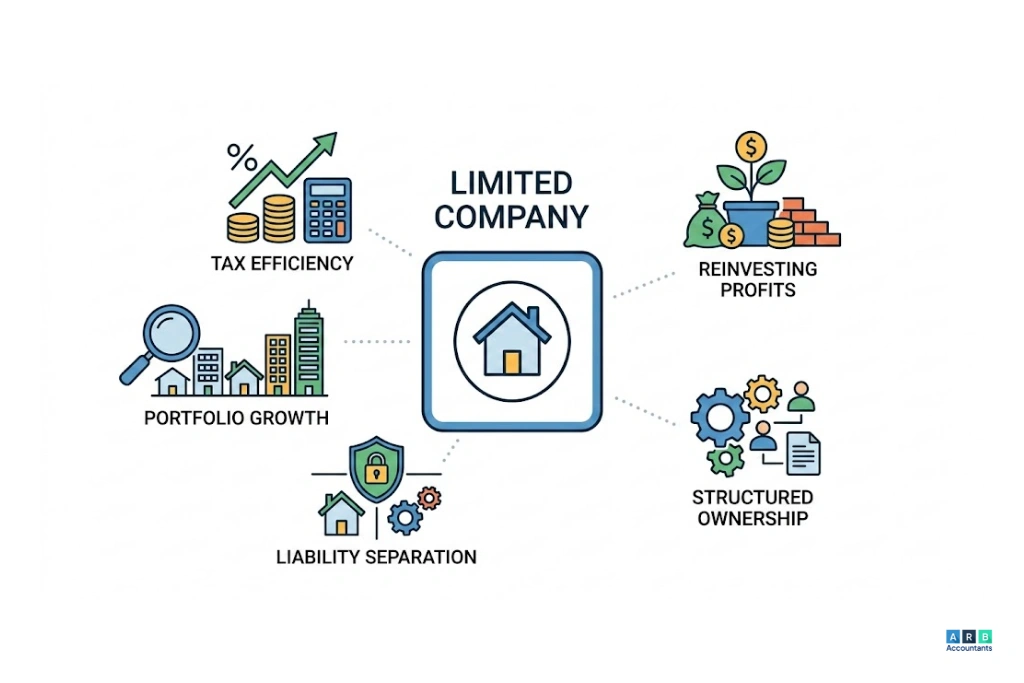

What Are the Pros of Buying Property Through a Limited Company?

Investors analysing buying property through a limited company usually focus on taxation structure, reinvestment flexibility, and operational control. A company structure allows property to be held inside a corporate entity rather than personally, which changes how profits, finance costs, and ownership are managed. For landlords building a portfolio, these factors often influence whether they buy property through limited company or personally.

Another important consideration is how lenders and tax rules interact with corporate ownership. Many investors learning how to buy property through a limited company begin by evaluating mortgage structures and long term tax treatment before they set up a limited company to buy property. The following advantages explain why limited company buying property has become a common strategy for portfolio landlords.

Potential Tax Efficiency on Rental Profits

One of the most cited advantages of buying property through a limited company is the potential difference between corporation tax and personal income tax. Rental profits generated within the company are taxed at corporation tax rates rather than personal income tax bands, which can reach higher marginal levels for some investors.

As of the current tax framework, UK corporation tax ranges between 19 percent and 25 percent depending on company profits. Higher rate taxpayers who hold property personally may pay more through income tax on rental profits.

For investors pursuing long term growth, reinvesting profits inside the company can compound capital faster because funds remain within the corporate structure rather than being extracted personally. This strategic reinvestment model is often cited among the benefits of setting up a limited company for property investment.

Mortgage Interest Treatment for Buy to Let Companies

Financing structure is another reason many investors evaluate buying property through a limited company. Tax rules known as Section 24 changed how individual landlords claim mortgage interest relief on buy to let properties.

Corporate landlords operating through a buy to let ltd company mortgage structure typically record finance costs directly as a business expense within company accounts. This difference is one reason investors compare buy property through limited company or personally when planning acquisitions. Many landlords researching how to buy property through a limited company began exploring corporate structures after these tax changes affected individual property investors.

Many landlords work with accountants for buy to let landlords to model mortgage interest costs, rental yield, and tax exposure before deciding on a corporate ownership structure. Specialist guidance helps investors understand how buy to let finance interacts with company taxation and long term portfolio strategy.

Easier Portfolio Scaling and Reinvestment

Operationally, limited company buying property can create a more structured environment for building a portfolio. Because profits remain within the company, investors can accumulate capital more efficiently.

Typical reinvestment strategies include:

- reinvesting rental income into new acquisitions

- funding deposits for additional properties

- building a structured portfolio growth plan

This approach is often associated with the benefits of setting up a limited company for property investment because it supports long term expansion rather than short term income extraction.

Ownership Flexibility and Succession Planning

Company ownership is based on shares rather than direct property titles. This creates flexibility that is not always available when property is owned personally.

Examples include family members holding shares in the company, transferring shares rather than selling the underlying property, or implementing estate planning strategies across generations. Investors learning how to buy property through a limited company often evaluate share structures before they set up a limited company to buy property so ownership can be structured correctly from the start.

Clear Separation Between Personal and Investment Finances

Running rental property through a corporate entity creates financial separation between personal income and property operations. This separation can improve accounting clarity and reduce the risk of mixing personal expenses with property costs.

Defined expense policies, dedicated company bank accounts, and structured bookkeeping systems can also make portfolio management easier for investors operating multiple properties.

READ RELATED ARTICLE: Buy to Let Tax Changes and Landlord Tax Deductions

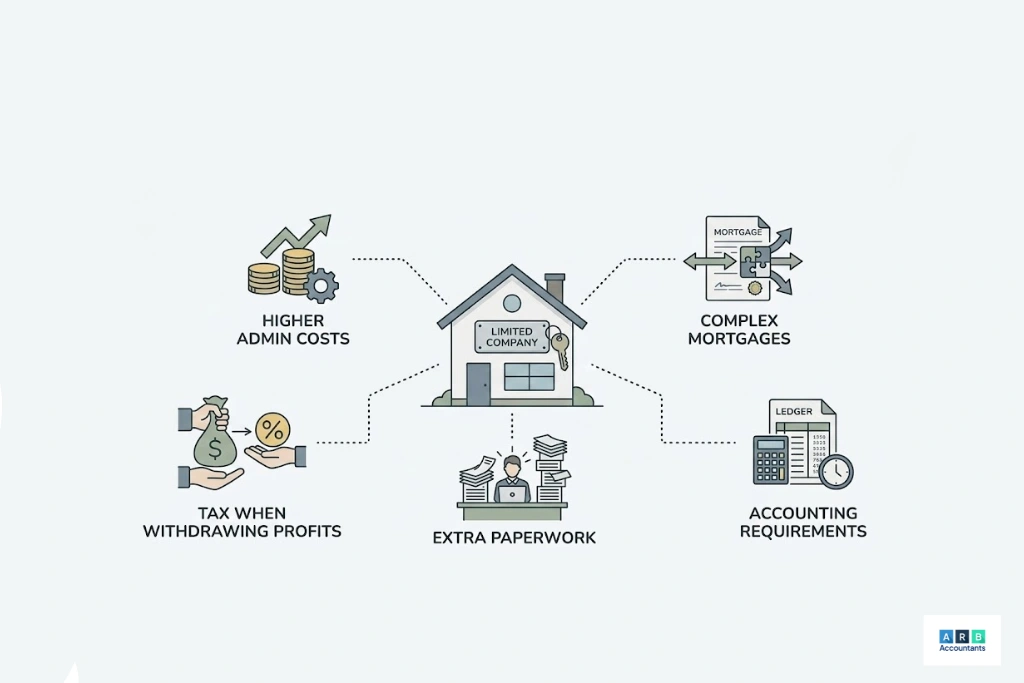

What Are the Cons of Buying Property Through a Limited Company?

Despite its advantages, buying property through a limited company also introduces additional complexity. Investors evaluating whether to buy property through limited company or personally often find that corporate ownership involves higher compliance requirements and different financing constraints.

Understanding these disadvantages is important before deciding to set up a limited company to buy property.

Higher Setup and Running Costs

Operating a property company introduces administrative and compliance costs that do not exist with personal ownership.

| Cost Type | Typical Examples |

|---|---|

| Company formation | Companies House registration fees |

| Compliance | Annual accounts and confirmation statements |

| Accounting | Corporation tax filing and bookkeeping |

| Legal | Corporate conveyancing and company documentation |

For landlords with a single property or modest rental income, these ongoing costs can outweigh the potential tax advantages of limited company buying property.

Limited Company Mortgages Can Be Harder to Obtain

Mortgage availability is another constraint. A buy to let ltd company mortgage is offered by fewer lenders compared with personal buy to let loans, and underwriting criteria are often stricter.

Lenders may charge slightly higher interest rates and require directors to provide personal guarantees. Investors evaluating buying property through a limited company should understand that these guarantees can still expose directors to risk even though the property is owned by the company.

Taking Money Out of the Company Creates Additional Tax

Profits generated inside the company are not automatically available for personal use. Investors must extract funds through structured methods.

Common approaches include:

- director salary payments

- repayment of director loans

- pension contributions

Because profits are taxed at the company level and again when extracted personally, investors may experience a form of double layer taxation depending on how funds are withdrawn.

Selling or Restructuring Property Can Be More Complex

Property transactions inside a company can involve additional legal and tax considerations. Corporate property sales may trigger corporation tax liabilities and require professional structuring.

Investors sometimes consider share sales rather than selling the property directly, which changes how transactions are negotiated. Another risk arises when landlords attempt to move property from personal ownership into a company later, because this can create tax and legal costs that were avoidable if the structure had been chosen earlier.

READ RELATED ARTICLE: Salary vs Dividends: What Is the Best Way to Pay Yourself

Should You Buy Property Through a Limited Company or Personally?

One of the most common questions investors ask when analysing buying property through a limited company is whether it is better to buy property through limited company or personally. The decision affects taxation structure, mortgage availability, administrative workload, and long term portfolio strategy. Investors also evaluate how a buy to let ltd company mortgage compares with standard personal buy to let lending when determining the most practical structure.

Limited company buying property has grown in popularity because it allows investors to manage property activity through a corporate entity rather than through personal income streams. However, the choice between buying property through a limited company and personal ownership depends heavily on investment objectives, tax position, and portfolio growth plans.

| Factor | Personal Ownership | Limited Company |

| Taxation | Income tax on rental profits | Corporation tax within the company |

| Mortgage options | Wider lender availability | More limited buy to let ltd company mortgage products |

| Admin | Low compliance requirements | Higher reporting and accounting obligations |

| Scaling portfolio | Harder to reinvest profits | Easier capital accumulation through company |

This comparison helps investors assess whether to buy property through limited company or personally before deciding how to structure acquisitions.

When Personal Ownership Often Makes More Sense

Personal ownership can remain a practical option for many landlords, particularly when property investment is small scale or designed to generate immediate personal income.

Examples include:

- Basic rate taxpayers who do not face higher marginal income tax bands

- Landlords holding a single rental property rather than building a large portfolio

- Investors who rely on rental income to support day to day living expenses

In these cases the benefits of setting up a limited company for property investment may not outweigh the administrative and compliance costs involved in running a corporate structure.

When Limited Company Buying Property May Be Better

Limited company buying property tends to suit investors who treat property as a long term investment business rather than a passive side income. Investors considering how to buy property through a limited company often do so because they plan to reinvest rental profits instead of withdrawing them immediately.

Common scenarios include:

- Higher rate taxpayers managing significant rental income

- Investors targeting long term portfolio expansion

- Landlords reinvesting profits into additional acquisitions

These investors often analyse whether they should buy property through limited company or personally before they set up a limited company to buy property that can hold multiple assets over time.

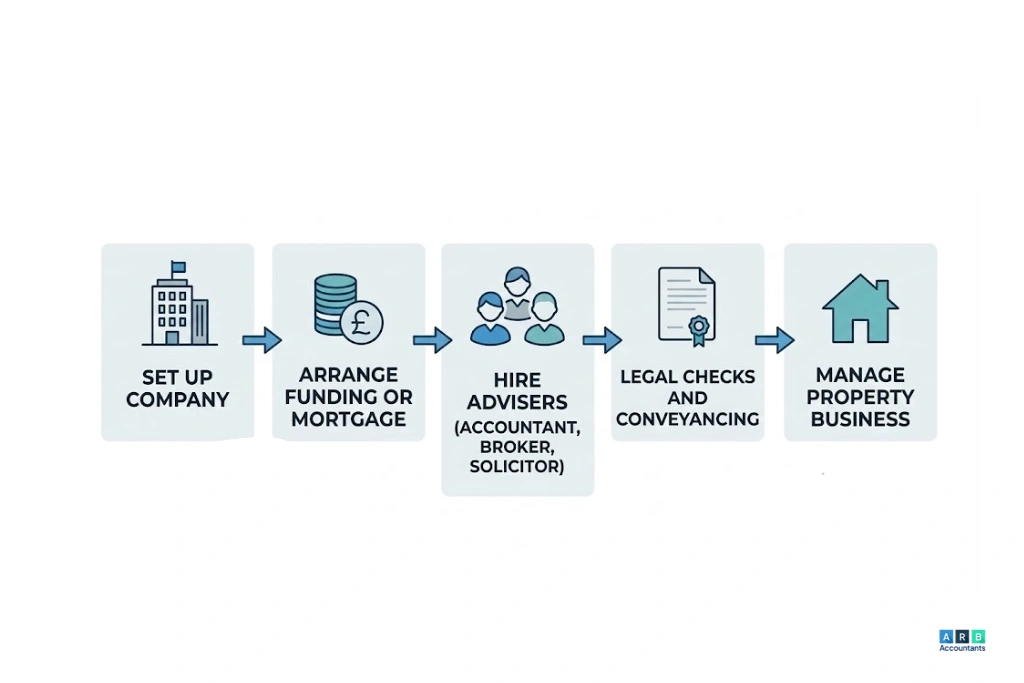

How Do You Buy Property Through a Limited Company Step by Step?

Understanding how to buy property through a limited company requires following a structured process. Investors often begin by forming the company entity before seeking finance or identifying properties, because lenders and solicitors must deal with the corporate borrower rather than an individual.

Step 1. Set Up a Limited Company to Buy Property

The first stage is to set up a limited company to buy property through Companies House. Investors must select directors, determine share ownership, and register the business for property investment activity.

Many landlords create Special Purpose Vehicle property companies, commonly referred to as SPVs. These companies are designed specifically for holding property assets, which simplifies underwriting for lenders providing a buy to let ltd company mortgage. At this stage investors also confirm that a company can purchase residential or commercial property, which answers the common question can a limited company buy a house.

Step 2. Open a Business Bank Account

After company formation, a dedicated business bank account is opened. Financial separation is essential because rental income, mortgage payments, and property expenses must flow through the company rather than personal accounts.

This separation allows investors to track performance more accurately when limited company buying property becomes part of a larger portfolio strategy.

Step 3. Secure a Buy to Let Limited Company Mortgage

Financing is normally arranged through a buy to let ltd company mortgage designed for corporate landlords. Lenders assess projected rental income, loan to value ratios, and the financial profile of company directors.

Although buying property through a limited company offers structural advantages, lenders frequently require directors to provide personal guarantees before approving finance.

Step 4. Complete Legal Conveyancing Through the Company

Property purchases must be completed through corporate conveyancing procedures. The solicitor acts for the company rather than the individual investor and ensures the property title is registered in the company name with HM Land Registry.

Investors researching how to buy property through a limited company often find that corporate conveyancing involves slightly more documentation than personal property purchases.

Step 5. Operate the Property as a Structured Investment Business

Once the purchase is completed, the property is operated through the company’s accounting system. Rental income, maintenance costs, mortgage interest, and compliance expenses must all be recorded within company accounts.

Over time, investors who set up a limited company to buy property can manage multiple assets within the same structure, which is one reason the benefits of setting up a limited company for property investment are often linked to long term portfolio management

Ongoing compliance usually requires professional accountancy services for limited company structures, particularly when rental income, mortgage interest, and operating costs must be reported through company accounts. Structured bookkeeping and tax planning also help investors track portfolio performance and maintain regulatory compliance.

Why Do Investors Buy Commercial Property Through a Limited Company?

Buying commercial property through a corporate entity is a long established strategy in UK property investment. Many investors exploring buying property through a limited company discover that commercial transactions are frequently structured this way because business assets are often easier to manage within a company. Limited company buying property in the commercial sector also allows investors to align ownership with trading operations, tenant agreements, and corporate finance arrangements.

Another factor is financing. Commercial lenders regularly structure funding through business entities rather than individuals, which means investors considering a buy to let ltd company mortgage for residential property often find that commercial lending naturally follows the same model. For investors deciding whether to buy property through limited company or personally, commercial property deals often favour corporate ownership from the beginning.

Why Businesses Often Buy Premises Through a Company

Several types of property investors structure acquisitions through corporate ownership when acquiring commercial premises.

Common examples include:

- Owner occupier businesses purchasing offices, warehouses, or retail units

- Commercial landlords building portfolios of income producing properties

- Mixed use developments combining residential flats with ground floor retail

These investors often evaluate how to buy property through a limited company because the structure can support operational control, structured financing, and long term asset management. When planning to set up a limited company to buy property, commercial investors frequently integrate the property holding company into their wider business structure.

Key Differences From Residential Property Investment

Commercial property investment introduces several additional considerations compared with residential buy to let.

Key differences include:

- Lease analysis, including rent review clauses and tenant obligations

- Tenant covenant strength, which lenders evaluate when approving finance

- Financing structures that may differ from standard buy to let ltd company mortgage lending

- Surveys and legal due diligence that analyse structural condition, planning classification, and commercial use restrictions

These factors explain why limited company buying property is common in the commercial sector, where structured financial planning often matters as much as property selection.

What Risks and Mistakes Do Investors Make When Buying Property Through a Limited Company?

Despite the potential advantages, investors can make costly errors when structuring buying property through a limited company. Many problems occur because investors focus only on tax savings without modelling the full financial picture.

Common mistakes include:

- Assuming limited liability removes all financial risk. Directors frequently provide personal guarantees for a buy to let ltd company mortgage, meaning personal exposure can still exist.

- Choosing the wrong company structure. Investors who fail to set up a limited company to buy property correctly may face issues with lenders or tax reporting.

- Poor tax modelling when deciding whether to buy property through limited company or personally. Without modelling profit extraction, investors may misunderstand real after tax returns.

- Mixing personal and company finances, which creates accounting complexity and compliance risks.

- Misunderstanding mortgage guarantees or lending conditions when arranging finance for limited company buying property.

Professional planning helps investors evaluate the benefits of setting up a limited company for property investment while avoiding structural mistakes.

Is Buying Property Through a Limited Company Worth It?

Whether buying property through a limited company is worthwhile depends on the investor’s financial profile and long term objectives. Investors deciding whether to buy property through limited company or personally usually analyse three factors first.

Tax band is one of the most influential variables. Higher rate taxpayers often explore the benefits of setting up a limited company for property investment because corporate taxation may allow profits to be reinvested more efficiently.

Portfolio size also matters. Investors planning to acquire multiple properties often research how to buy property through a limited company and choose to set up a limited company to buy property as a scalable investment vehicle.

Reinvestment strategy is another major factor. Investors reinvesting profits rather than withdrawing them may find limited company buying property supports long term portfolio growth more effectively.

Buying property through a limited company therefore works best when property investment is treated as a structured business activity. Investors should always seek advice from experienced property tax specialists or accountants Southend before finalising the structure. Firms such as ARB Accountants regularly advise landlords on whether corporate ownership aligns with their investment goals and compliance obligations.

Frequently Asked Questions

Is buying property through a limited company worth it?

Is buying property through a limited company worth it?

It can be worthwhile for higher-rate taxpayers building portfolios and reinvesting profits. It is often less attractive for single-property owners needing income personally.

What is a buy to let ltd company mortgage?

It is a landlord mortgage where the borrower is a limited company rather than an individual. Directors often provide personal guarantees.

Should I buy property through limited company or personally?

Choose personally for simplicity and immediate income. Consider a company if you plan to reinvest and scale.

Can I live in a property owned by my limited company?

It is possible but can create complex tax consequences and is often inefficient. Professional advice is strongly recommended.

Can a limited company buy a house in the UK?

Yes. A UK limited company can legally buy residential property, including houses and flats. Many investors use a company structure specifically for buy-to-let purposes. If borrowing, you’ll need a specialist limited company mortgage rather than a standard residential loan.

How do I set up a limited company to buy property?

You must register a limited company with Companies House, appoint at least one director, define the share structure, and open a business bank account. Many investors use an accountant to structure the company tax-efficiently and ensure the business activity is aligned with property investment.

Does buying property through a limited company save tax?

It can in certain situations. Rental profits are subject to Corporation Tax rather than Income Tax, which may benefit higher-rate taxpayers who plan to reinvest profits. However, extracting money from the company (via salary or dividends) can create additional tax, so overall savings depend on your goals and tax band.

Can I transfer a property I already own into a limited company?

It’s possible, but it is usually treated as a sale at market value. This can trigger legal costs and potential tax implications. It’s important to get professional advice before attempting to move personally owned property into a company structure.

Do I need a special mortgage to buy property through a limited company?

Yes. Most lenders require a specific limited company buy-to-let mortgage product. These are assessed differently from personal mortgages and typically require directors to provide personal guarantees.

Is buying commercial property through a limited company different?

Commercial property purchases through a limited company follow a similar structure but may involve different lending criteria, lease considerations, and due diligence requirements. Commercial finance is typically assessed more on the strength of the lease and tenant covenant.