Salary vs Dividends: The Most Tax-Efficient Way to Pay Yourself in 2026/27

Free · 60 seconds · No email needed to see your answer

How should you split your pay — salary or dividends?

The right answer depends on your company, your profits and your goals. Answer five quick questions and get a tailored split for the 2026/27 tax year.

Your tailored answer

These figures are illustrative for the 2026/27 tax year and assume fairly standard circumstances. Your optimal split depends on your exact profit, other income and goals.

Want this confirmed for your exact numbers?

If you'd like to learn more about paying yourself tax-efficiently, book a free, no-obligation call and we'll run your real figures with you.

How is this worked out?

Based on the 2026/27 figures: personal allowance £12,570, dividend allowance £500, basic-rate threshold £50,270, dividend rates 10.75% / 35.75% / 39.35%, employer NI 15% above the £5,000 secondary threshold, Lower Earnings Limit £6,708, and Employment Allowance £10,500 (not available to single-director companies with no other employees).

It is a guide, not formal advice — the right split always depends on your specific company and personal position.

Deciding between salary and dividends is one of the bigger calls a UK company director makes each year. Get it wrong and you either pay more tax than you need to, or you weaken the income proof a mortgage lender wants to see. A salary runs through PAYE and attracts Income Tax and National Insurance; dividends come out of profit the company has already paid Corporation Tax on, and they are taxed under their own, lower rates. Our limited company accountants work this split out for hundreds of directors a year.

The usual question is how much you can take in dividends before the tax rate steps up, and the answer comes down to your total income. A £12,570 salary plus £37,700 in dividends, for instance, keeps most directors inside the basic-rate band (GOV.UK). Go above that and the extra dividends are taxed at the higher rate.

The other common question is how much you can take completely tax-free. That is your Personal Allowance plus the £500 dividend allowance — £13,070 in a year where you have no other income. Whether a salary-light, dividend-heavy mix actually suits you depends on your company’s profits and what you need to draw out personally.

Not sure how to structure your pay as a director?

Our accountants calculate the most tax-efficient salary and dividend split for your specific situation. Get in touch for a free initial call.

Table Of Contents

- Salary vs Dividends: What Are the Key Differences for UK Company Directors

- What Is the At-a-Glance Comparison Between Salary and Dividends?

- Do Dividends Count as Income in the UK?

- How Much Can I Pay Myself in Dividends Without Extra Tax?

- Dividend Compliance: What Rules Must Limited Companies Follow?

- Self Assessment and Dividends: How Should Directors Report Dividend Income?

- Combining Salary and Dividends for Maximum Efficiency

- Is It Better to Pay Yourself a Salary or Dividends?

- What Are the Most Common Mistakes Directors Make When Taking Dividends?

- What Future Changes Could Impact Salary vs Dividends Strategy in the UK?

- Frequently Asked Questions

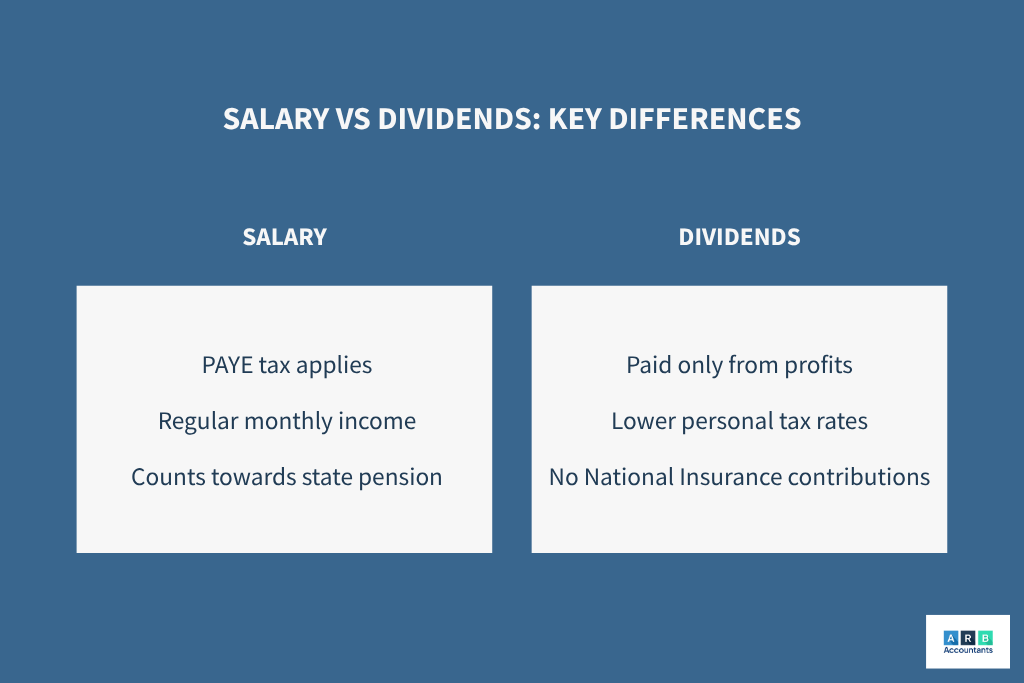

Salary vs Dividends: What Are the Key Differences for UK Company Directors

The two differ in how they are taxed and in how you actually pay them out. A salary is employment income: it carries Income Tax and National Insurance (both the employee’s and the employer’s), and it goes through payroll every month. Dividends come from profit the company has already paid Corporation Tax on, and they carry no National Insurance at all.

How Are Salary Payments Processed and Reported?

-

Salary: Run through PAYE, reported to HMRC in real-time. Provides proof of regular income for mortgages and loans.

-

Dividends: Declared by the board, recorded in minutes, and supported by a dividend voucher. Reported on your Self Assessment return.

How Much in Dividends Can a Director Take from a Limited Company?

There is no statutory limit; what you can take depends on the post-tax profit the company actually has. Pay out more than your retained profits and the excess can be treated as an illegal distribution, which brings HMRC penalties. “Should I take salary or dividends?” is usually the first thing a new director asks, and the answer is almost always a low-salary, high-dividend split.

Many freelancers face similar salary-versus-dividends decisions, which is why our accountants for freelancers often help them structure income in a tax-efficient way.

Difference Between Salary and Dividends

| Aspect | Salary | Dividends |

|---|---|---|

| Tax | Income Tax + NI | Dividend Tax only |

| Timing | Monthly PAYE | When declared |

| Proof of income | Strong | Limited |

| Pension contributions | Yes | No (unless via salary) |

| Risk | Lower HMRC scrutiny | Must have sufficient profits |

Director dividends tax for 2026/27 is 10.75% (basic), 35.75% (higher), 39.35% (additional) after a £500 dividend allowance (GOV.UK). Rates rose by 2 percentage points across the basic and higher bands from 6 April 2026, following the Autumn Budget 2025 announcement. The previous 2025/26 rates (8.75% / 33.75% / 39.35%) still apply if you’re working out tax on dividends taken in the year ending 5 April 2026. Even after the increase, dividends remain a cheaper way to draw profit than the equivalent salary, because they carry no National Insurance. Getting the structure right usually means running payroll services for the salary side and keeping clean records for the dividend declarations.

The right split depends on your numbers, not a generic example.

The optimal split changes with your salary, dividends already taken this year, and the current tax thresholds. We work this out for you. Speak to an ARB accountant today.

What Is the At-a-Glance Comparison Between Salary and Dividends?

When comparing salary vs dividends for a UK limited company director, it’s important to understand that the two are taxed in entirely different ways. Salary is processed through PAYE, meaning Income Tax and National Insurance (NI) are deducted at source. For directors, this includes both employee and employer NI, which can significantly increase the overall cost to the company. Dividends, on the other hand, are paid from post–Corporation Tax profits and are not subject to NI, making them a popular choice for tax efficiency.

PAYE vs Dividends: How Are They Taxed in the UK?

Under PAYE vs dividends, any salary above personal allowance (£12,570) is taxed at 20% (basic rate), 40% (higher rate), or 45% (additional rate), plus NI at 8% for employees (2% above the upper earnings limit) and 15% for employers (raised from 13.8% on 6 April 2025 at the Autumn Budget 2024, on earnings above the £5,000 secondary threshold). The upside of taking a salary is that it counts as qualifying income for pensions and can improve mortgage affordability.

How Do Corporation Tax Rules Affect Dividend Payments?

A company settles its Corporation Tax first (25% on profits above £250,000, with lower rates below that), and dividends come out of what is left. So the amount available to distribute is capped by retained post-tax profit. And no, dividends do not reduce your Corporation Tax bill: unlike salary, which is a deductible business expense, they are paid from the bottom line after tax.

What Are the Current Dividend Tax Rates and Allowances in the UK?

In 2026/27 the dividend allowance is £500. Above that, dividend tax is 10.75% (basic rate), 35.75% (higher rate), or 39.35% (additional rate), after the 2-point rise across the basic and higher bands on 6 April 2026. The old 2025/26 rates (8.75% / 33.75% / 39.35%) still apply to dividends taken in the prior tax year (GOV.UK). As an example, £40,000 of dividends on top of a £12,570 salary attracts no NI on the dividend portion and works out cheaper than taking the same amount as salary. At the basic rate, your room runs up to the £50,270 threshold.

Dividends cut your tax bill, but the right amount is a balance: the short-term saving against what a salary buys you in NI credits, pension, and mortgage evidence. For most people that means a modest salary with dividends on top. Some directors also use a company car as an alternative to dividends, especially given the low benefit-in-kind rates on fully electric vehicles.

Do Dividends Count as Income in the UK?

Yes, but they are treated differently from salary. Salary is “earned income,” taxed through PAYE with Income Tax and National Insurance. Dividends are “unearned income”: no NIC, but you still declare them on your Self Assessment return. Mortgage lenders count dividend income too, as long as you can show a couple of years of dividend vouchers and tax returns to prove it is steady.

How Much Can I Pay Myself in Dividends Without Extra Tax?

In 2026/27 you can take £13,070 completely tax-free if this is your only income — a £12,570 salary covered by your personal allowance, plus the first £500 of dividends covered by the dividend allowance. Beyond that, dividends are taxed at 10.75% up to the £50,270 basic-rate threshold.

A common question is how much you can take in dividends before tipping into the higher band. It depends on your personal allowance and your dividend allowance. In 2026/27 the personal allowance is £12,570 (GOV.UK) and the dividend allowance is £500 (GOV.UK), so with no other income you can take £13,070 completely tax-free.

How Can Directors Combine Salary and Dividends Efficiently?

If you take a salary up to the personal allowance, you can add Ltd company dividends of up to £37,700 before entering the higher dividend tax rate. At this level, dividends are taxed at 10.75% in 2026/27 (was 8.75% in 2025/26 and prior years before the Autumn Budget 2025 increase), still far lower than PAYE income tax for the same amount. This is why many directors opt for a modest salary plus dividends from a limited company.

Example:

-

Salary: £12,570 (no Income Tax, minimal NI)

-

Dividends: £37,700 (taxed at 10.75% after the £500 allowance)

-

Result: £50,270 total income at the lowest combined rates

Contractors deal with the same challenges around balancing salary and dividend withdrawals, and our contractor accountants regularly guide them through the most efficient mix of limited company dividends vs salary. For directors who want a closer review of their personal tax position, our tax advice service can confirm the right structure before any decisions are locked in.

What Is the Best Strategy for Timing Salary and Dividend Payments?

Most directors run a small, steady salary through payroll across the year, then declare dividends in chunks — often quarterly, or whenever the company has clearly banked enough profit to cover them. The thing to get right is checking there are distributable profits at the point you declare each dividend, not just at the year end, and dating the minutes and vouchers accordingly.

What Happens If Dividends Push Me Above the Basic Rate Tax Band?

Once total income passes £50,270, the dividend rate jumps to 35.75% (the 2026/27 higher rate, up from 33.75% in 2025/26). That step-up is the whole reason the split is worth planning. For some directors, staying inside the basic-rate band is the right call; for others, taking more to cover personal costs is worth the extra tax.

How Much Can a Director Pay Themselves in 2026/27?

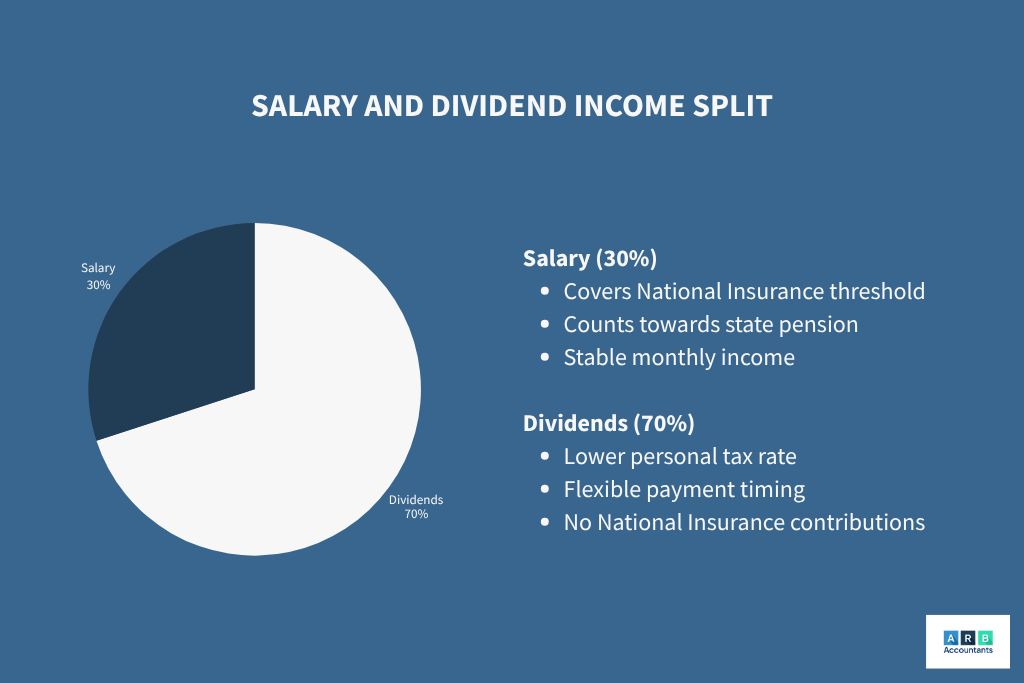

For most limited company directors in 2026/27, the most tax-efficient setup is a salary of £12,570 plus dividends up to the £50,270 basic-rate threshold, where the dividends are taxed at just 10.75%. On that split you draw £50,270 for the year and pay around £3,999 in personal tax.

Most directors we speak to ask the same thing: what is the most I can take out without paying more tax than I have to? It comes down to two numbers — your salary level, and how much you take in dividends on top. Here is how that looks for the current tax year.

The optimal director salary in 2026/27

There are two salary levels worth knowing about. The first is the Lower Earnings Limit (LEL), £6,708 a year in 2026/27. A salary at this level counts as a qualifying year for your State Pension and costs very little. It is not quite free of employer NI, though: the secondary threshold (the point above which your company pays employer NI) sits at £5,000, so the company pays 15% employer NI on the £1,708 between £5,000 and £6,708. That comes to about £256 a year — small, but no longer zero.

The second level is £12,570, the personal allowance. If your company qualifies for the Employment Allowance (£10,500), a £12,570 salary is usually the most efficient choice: no income tax, no employee National Insurance, and the Employment Allowance soaks up the £1,135 of employer National Insurance the company would otherwise pay (£12,570 minus the £5,000 secondary threshold, at 15%).

The sole director with no other employees

This is the most common small-company setup, and it changes the answer in one important way: the company cannot claim the Employment Allowance. HMRC’s rule is that you can’t claim it when the only person paid above the secondary threshold is a single director (GOV.UK). So there is no £10,500 allowance sitting there to soak up the employer NI.

That makes a £12,570 salary look dearer at first glance. The company pays employer NI of £1,135 on it — 15% of the £7,570 above the £5,000 secondary threshold — with nothing to offset it. But it is usually still the better choice, because the salary and that employer NI are both deductible against Corporation Tax. For most sole directors the CT relief slightly outweighs the NI, so £12,570 leaves you a few hundred pounds a year ahead of a £6,708 salary. At the 25% Corporation Tax rate the gap is a little wider still.

The reason to take £6,708 instead is simplicity, not tax. Employer NI on it is only about £256 a year, there is less payroll to run, and it still earns a qualifying State Pension year — both salary levels clear the £6,708 Lower Earnings Limit, so neither buys you more pension than the other. If you would rather keep things lean, that is a fair trade. Either way, the dividend side of the decision works exactly as it does for any other director.

The dividend allowance and rates

The dividend allowance is £500 for both 2025/26 and 2026/27. This means the first £500 of dividend income you receive each year is free from dividend tax. It is worth noting this has fallen significantly in recent years: the allowance was £5,000 in 2018 and has been cut repeatedly since.

Once you go above £500 in dividends, the tax rate depends on which income tax band your total income puts you in. Rates rose by 2 percentage points from 6 April 2026 at the Autumn Budget 2025, so the right column applies to dividends taken in the current 2026/27 tax year and the left column applies to dividends taken in 2025/26:

| Tax Band | Total Income | 2025/26 rate | 2026/27 rate |

|---|---|---|---|

| Basic rate | Up to £50,270 | 8.75% | 10.75% |

| Higher rate | £50,271 to £125,140 | 33.75% | 35.75% |

| Additional rate | Over £125,140 | 39.35% | 39.35% |

A worked example

Take a director who pays themselves a £12,570 salary plus £37,700 in dividends in 2026/27, with the company qualifying for the Employment Allowance.

| Item | Amount |

|---|---|

| Director salary | £12,570 |

| Income tax on salary | £0 (covered by the personal allowance) |

| Employee National Insurance | £0 (salary at the £12,570 primary threshold) |

| Employer National Insurance | £0 (covered by the Employment Allowance) |

| Dividends taken | £37,700 |

| Dividend allowance | £500 (tax-free) |

| Taxable dividends | £37,200 |

| Dividend tax at 10.75% | £3,999 |

| Total income received | £50,270 |

| Total tax paid | £3,999 |

So the director draws £50,270 for the year and pays just under £4,000 in personal tax. An employee earning the same £50,270 as salary alone would hand over around £10,500 once income tax and National Insurance are added together — so the split saves roughly £6,500.

Two things are worth flagging. The identical split in 2025/26 cost only £3,255 in tax, because the basic dividend rate was 8.75% then — so the April 2026 rise adds roughly £744 a year for the same setup. And if total income goes above £50,270, the dividends over that line are taxed at 35.75%, not 10.75%, which is why it pays to fix the split before the year gets away from you.

Tax rules change and your situation may differ from the example above. If you want the right numbers for your specific company, our limited company accountants can work this out for you before you make any decisions.

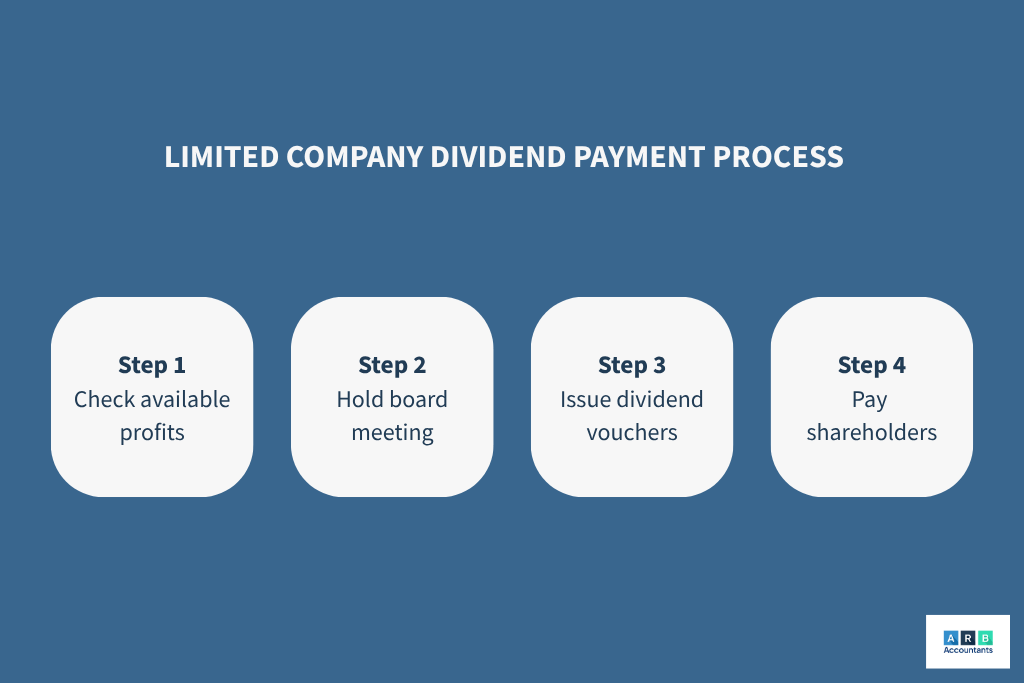

Dividend Compliance: What Rules Must Limited Companies Follow?

Paying a dividend comes with strict legal requirements. It can only be paid from distributable profits — what is left after Corporation Tax (GOV.UK). If those profits are not there, a payment labelled a dividend can be treated as unlawful and may have to be repaid.

What Documentation and Records Are Required for Dividends?

For every dividend payment, directors must hold a board meeting to declare it, even if they are the only shareholders. You should prepare:

-

Minutes of the meeting

-

A dividend voucher detailing the date, shareholder name, and amount paid

These records protect you if HMRC questions whether the distribution was lawful.

What Is a Dividend Voucher and Why Is It Needed?

Whenever a limited company pays dividends, it must issue a dividend voucher. This document acts as proof of the payment and includes:

-

Company name

-

Date of payment

-

Shareholder’s name

-

Amount of the dividend

HMRC requires that dividend vouchers are retained with company records for at least six years. Even if you are the only shareholder and director, you must still produce a dividend voucher each time you take a dividend. This helps demonstrate compliance if HMRC investigates whether payments were lawful and properly documented.

How Does HMRC Treat Illegal or Unlawful Dividends?

If you withdraw funds when no distributable profits are available, HMRC may treat it as a director’s loan rather than a dividend. That can trigger an S455 charge on the company — 35.75% for loans made in 2026/27, up from 33.75%, since the rate mirrors the higher dividend rate.

Incorrect dividend records can attract HMRC attention, which is why experienced tax investigation accountants stress the importance of proper minutes and vouchers.

How Do Compliance Rules Link Back to Tax Efficiency?

The compliance side matters as much as the tax planning. Skip the paperwork and you can lose the advantage you were aiming for, because HMRC can question whether the payment was a lawful dividend at all. Clean minutes and vouchers are what prove it was.

Are Dividends Paid Before or After Corporation Tax?

No, dividends are always paid after Corporation Tax has been accounted for. This means the company pays Corporation Tax on profits first, and only the remaining post-tax profits can be distributed as dividends. Paying dividends before Corporation Tax would be considered an illegal dividend, which HMRC can demand to be repaid. This is why accurate profit calculations and board approval are essential before declaring dividends.

Self Assessment and Dividends: How Should Directors Report Dividend Income?

If you’re a UK company director, any dividends you receive must be reported through your Self Assessment dividends section. Even if your dividends fall within the £500 dividend allowance, HMRC still requires you to declare them.

Key points directors should know:

-

Where to declare: Dividend income is entered in the “UK dividends” section of the Self Assessment form.

-

Tax bands apply: Your dividend income is added to your salary and other earnings to determine your overall tax band.

-

Deadlines: Online Self Assessment filing is usually due by 31 January following the tax year. Late submissions or missed dividend declarations can trigger penalties.

-

Supporting records: Keep dividend vouchers and board meeting minutes as evidence in case HMRC requests proof.

Since every dividend must be reported correctly, a self-assessment accountant can help directors avoid mistakes that trigger penalties.

Combining Salary and Dividends for Maximum Efficiency

Most directors settle on a low salary topped up with dividends. The usual pattern is a salary around the £12,570 personal allowance: enough to count towards the State Pension and other benefits, but low enough to avoid employee National Insurance.

Why Do Many Directors Choose to Pay Themselves a Low Salary?

-

A low salary ensures NI credits for future state pension.

-

It maintains eligibility for mortgages and loans, as lenders favour regular salary evidence.

-

It reduces PAYE costs while fulfilling legal obligations.

How Much Can I Pay Myself in Dividends?

The first £500 of dividends each year is covered by the dividend allowance and taxed at 0%. Above that, the rate depends on the band your total income falls into:

-

Basic rate: 10.75% in 2026/27 (was 8.75% in 2025/26)

-

Higher rate: 35.75% in 2026/27 (was 33.75% in 2025/26)

-

Additional rate: 39.35% (unchanged)

To stay on the basic rate, keep your total income within the £50,270 higher-rate threshold. In practice that means your dividend room is roughly £50,270 minus whatever salary you have taken.

How Do Pension Contributions Affect Salary vs Dividends in the Long Term?

Unlike salary, dividends do not count towards NI or pension qualifying years. So while dividends reduce tax, a minimal salary is necessary for state benefits. Directors can make personal pension contributions from dividends but won’t get NI credits this way.

Salary vs Dividends: What’s the Best Option for Directors?

Balancing PAYE salary and dividends helps minimise overall tax while preserving pension and loan access. Each company director should tailor the split based on income and future plans.

Is It Better to Pay Yourself a Salary or Dividends?

For most limited company directors, a mix is best: a low salary (around £12,570) to use your personal allowance and protect your State Pension, then dividends for the rest — they carry no National Insurance and are taxed at lower rates than salary.

The answer depends on your priorities.

-

Salary is better if you want consistent income proof, qualify for state pension credits, and make pension contributions.

-

Dividends are often more tax efficient because they avoid NIC and are taxed at lower rates.

For most directors, a mix of the two is the most efficient approach: a modest salary (to cover NIC and pension eligibility) plus dividends for the remainder. Paying dividends vs salary balances the immediate tax saving with long-term benefits.

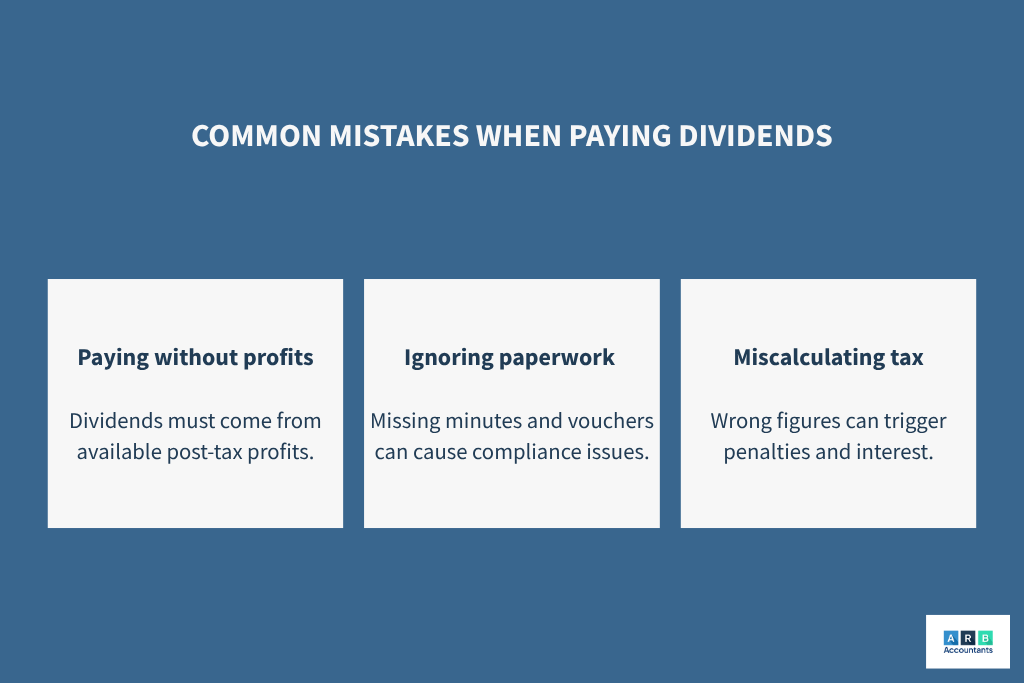

What Are the Most Common Mistakes Directors Make When Taking Dividends?

A few mistakes come up again and again, and each one can cause tax or legal trouble.

-

Drawing without profits: dividends can only come from distributable profits, not whatever cash happens to be in the account. Set aside the Corporation Tax first.

-

Ignoring your tax bands: the dividend rate steps up at £50,270. Take dividends without checking where they land and you can trigger a bigger bill than you expected.

-

Confusing cash flow with profit: some of that bank balance may already be earmarked for VAT, payroll, or supplier bills. Make sure the profit is genuinely there before you declare.

Before each dividend, confirm the company’s retained earnings and think about which tax band the payment pushes you into.

What Could Change for Salary vs Dividends Next?

The direction of travel is clear: dividends are slowly being taxed more like salary. The April 2026 rise pushed the basic and higher dividend rates up by 2 points, and the same Autumn Budget 2025 set out increases to savings and property income tax from April 2027. A few things worth keeping an eye on:

-

Further dividend rate rises. The 2026 increase may not be the last. The Treasury has been open about wanting to narrow the gap between dividend and employment tax, so it is worth leaving some headroom in your planning rather than assuming today’s rates hold.

-

Corporation tax. If the main rate goes up, there is less post-tax profit to distribute, which shrinks the dividend side of the equation regardless of what the dividend rate does.

-

The allowances. The £500 dividend allowance is already down from £5,000 in 2018, and the personal allowance is frozen until 2028. Either could move again at a future Budget.

The split that is most efficient this year may not be next year, so a quick review each April is worth the time. As one of the accountancy firms Southend businesses rely on, ARB keeps track of these changes so you do not have to.

Frequently Asked Questions

How much dividend can I pay myself tax-free?

The dividend allowance is £500 in both 2025/26 and 2026/27. This means the first £500 of dividend income you receive each year is free from dividend tax, regardless of which tax band you are in. Above the allowance, dividends are taxed at 10.75% (basic), 35.75% (higher), or 39.35% (additional) in 2026/27 — rates rose by 2 percentage points across the basic and higher bands from 6 April 2026. The 2025/26 rates were 8.75% / 33.75% / 39.35%. If you are not sure which band applies to you, our tax advice service can review your position.

What is the most tax-efficient salary for a director in 2026/27?

For most directors it is either £6,708 or £12,570, depending on whether your company qualifies for the Employment Allowance (£10,500). A £12,570 salary uses your full personal allowance, so there is no income tax, and the Employment Allowance covers the £1,135 of employer National Insurance the company would otherwise pay (15% of the £7,570 between the £5,000 secondary threshold and £12,570). If your company does not qualify — most often a sole director with no other employees — £12,570 usually still comes out ahead once you count the Corporation Tax relief on the salary, though some directors take £6,708 (the Lower Earnings Limit) for simplicity, paying around £256 of employer NI but keeping a State Pension qualifying year. The right answer depends on your company structure, so it is worth confirming with an accountant before payroll is set up.

Is it better to take salary or dividends from a limited company?

For most limited company directors, a combination of a low salary and dividends is more tax-efficient than taking salary alone. Dividends are not subject to National Insurance, which makes them a more cost-effective way to extract profit once your salary has used up your personal allowance. A salary-only approach means paying both income tax and National Insurance on every pound above £12,570. The right split depends on your total income, your company’s profitability, and whether other income sources affect your tax position for the year. Our limited company accountants can calculate the most efficient structure for your situation.

Can I pay myself dividends instead of a salary?

Technically yes, but taking dividends with no salary at all is generally not advisable. Taking at least a small salary up to the Lower Earnings Limit (£6,708 in 2026/27) protects your State Pension entitlement and counts as a qualifying National Insurance year. Dividends can only be paid out of retained profits after corporation tax has been accounted for, so your company needs to be in profit before a dividend can be declared. Paying yourself only dividends when there are no profits is a compliance risk that HMRC can challenge. If you are unsure whether your company has distributable profits, your accountant should confirm this before any dividend is declared.

The optimal split changes every April when tax thresholds update. Getting this wrong even by a small amount can cost hundreds or thousands of pounds per year. If you have not reviewed your salary and dividend structure since the new tax year started, it is worth doing now.

Ready to take the right amount?

Our accountants set up your salary and dividend structure, handle your payroll, and file your self-assessment. Contact ARB today.

About The Author

Saurabh Bedi | Director

Saurabh is a tax advisor at ARB Accountants, specialising in Self-Assessment and small business tax. He's dedicated to making tax simple and stress-free, helping clients stay compliant and confident with HMRC.

Qualifications & Experience

- Fellow of Chartered Certified Accountants (ACCA)

- MSc Chartered Certified Accountancy 2008

- Working in accountancy since 2008