Skip to content

Skip to content

How to Read a Balance Sheet: A Guide for UK Business Owners

Last updated:

March 18, 2026

Most business owners glance at their balance sheet when their annual accounts arrive, check the profit figure is positive, and move on. Sound familiar? You’re not alone, but you’re also missing one of the most useful documents your accountant produces each year.

Knowing how to read a balance sheet gives you a real picture of your business’s financial health. Not just whether you made money, but whether the business is stable, how much debt it’s carrying, and whether you could survive a slow month. This guide on how to read a balance sheet walks you through every section in plain English, with a worked UK example and practical tips on what to look for.

Table Of Contents

show

- What Is a Balance Sheet? The Purpose of Balance Sheet Reporting

- What Does a Balance Sheet Show? Three Key Sections

- How to Read a Balance Sheet UK: A Worked Example

- Where Is Debt on a Balance Sheet?

- How to Do Balance Sheet Analysis: How to Read a Balance Sheet Beyond the Basics

- Understanding Financial Statements: How to Read a Balance Sheet in Context

- What Are the Warning Signs on a Balance Sheet?

- Your Balance Sheet and Companies House: What UK Businesses Must File

- Final Thoughts

- Frequently Asked Questions

What Is a Balance Sheet? The Purpose of Balance Sheet Reporting

A balance sheet is a financial snapshot of your business at a single point in time, usually the last day of your financial year. Before we get into how to read a balance sheet in detail, it helps to understand why it exists. The purpose of balance sheet analysis is to give you a complete picture of financial health that your profit figure alone never can. It answers three questions: what does your business own, what does it owe, and what is left over for the owners?

That “left over” figure is the real measure of your business’s worth. You can think of it like this, and this is the real purpose of balance sheet reporting: if you sold everything your business owns today and paid off every debt, what would remain? That’s what the balance sheet tells you, and that’s precisely what does balance sheet show as a document.

The purpose of balance sheet reporting goes well beyond compliance, and most business owners underestimate how much it can tell them. Banks use it when you apply for a loan. Investors look at it before putting money in. HMRC may refer to it during an enquiry. But most importantly, you should use it because if you don’t know how to read a company balance sheet, you’re running your business with one eye closed. And learning how to read a company balance sheet is simpler than most people think.

Every balance sheet follows the same equation:

Assets = Liabilities + Equity

Everything on one side must equal everything on the other. That’s not an accounting quirk; it’s a logical reflection of how every business is funded and what it holds.

What Does a Balance Sheet Show? Three Key Sections

What is balance sheet information really telling you? Three things, and each tells you something different.

Assets – What Your Business Owns

Assets are split into two groups:

Fixed assets (non-current assets) are things the business holds for more than 12 months. This includes property, machinery, vehicles, and equipment. It also includes intangible assets like goodwill, the value attributed to a business’s reputation or customer relationships when it was bought.

Current assets are things the business owns or expects to convert to cash within 12 months. This is where you’ll find stock, trade debtors (money customers owe you), and your cash balance.

One thing many business owners miss: the order matters. Current assets are listed in order of liquidity, from the easiest to convert to cash (cash itself) to the hardest (stock).

Liabilities – What Your Business Owes

Liabilities are also split into two groups.

Current liabilities are debts due within 12 months, trade creditors, VAT payable to HMRC, corporation tax due, and short-term loan repayments. This is the section that catches people out. A business can look profitable and still collapse because its current liabilities outstrip its current assets.

Long-term liabilities are debts due after 12 months, typically bank loans, director’s loans, or finance lease obligations.

Equity in Balance Sheet Terms – What It Means for You

Equity in balance sheet terms is the residual value once you’ve subtracted all liabilities from all assets. For a limited company, this usually includes share capital (the initial investment when the company was set up) and retained earnings (profits kept in the business over time).

A growing retained earnings figure is a good sign. It means the business is generating profit and not distributing all of it. A negative equity figure, on the other hand, means the business technically owes more than it owns, and that’s a situation that needs addressing fast.

How to Read a Balance Sheet UK: A Worked Example

Let’s make this concrete. Understanding how to read a balance sheet that UK businesses produce is much easier with a real example. Here’s a simplified example balance sheet for a fictional UK business. This is the kind of layout you’d see in a typical set of small company accounts. Use this example balance sheet to follow along as we explain each section.

Example Balance Sheet – UK Small Limited Company

| Fixed Assets | £ |

| Property, plant and equipment | 85,000 |

| Total Fixed Assets | 85,000 |

| Current Assets | |

| Stock | 12,000 |

| Trade debtors | 18,500 |

| Cash at bank | 9,200 |

| Total Current Assets | 39,700 |

| Current Liabilities | |

| Trade creditors | (8,400) |

| Corporation tax payable | (5,200) |

| VAT payable | (2,100) |

| Total Current Liabilities | (15,700) |

| Net Current Assets | 24,000 |

| Total Assets Less Current Liabilities | 109,000 |

| Long-Term Liabilities | |

| Bank loan | (35,000) |

| Total Long-Term Liabilities | (35,000) |

| Net Assets | 74,000 |

| Equity | |

| Share capital | 1,000 |

| Retained earnings | 73,000 |

| Total Equity | 74,000 |

Net assets (£74,000) equal total equity (£74,000). The balance sheet balances as it always must. This example balance sheet shows a business in a healthy position.

What Is the Balance Sheet Total?

The balance sheet total is the total assets figure: £124,700 in this case (£85,000 fixed assets + £39,700 current assets). This gives you a quick sense of the overall scale of the business’s resources, useful context when you’re learning how to read a balance sheet year on year. When you read a company’s balance sheet year on year, watch whether the balance sheet total is growing; it’s a rough indicator of whether the business is expanding.

Where Is Debt on a Balance Sheet?

This is one of the most common questions when learning how to read a balance sheet. Debt sits in the liabilities section, split by when it’s due.

Short-term debt, overdrafts, short-term loans, or the portion of a long-term loan due within the next 12 months, appear under current liabilities. Long-term debt, such as the bank loan in our example above, sits under long-term liabilities.

Here’s the important bit. To understand how to read a balance sheet properly, you need to look at debt in relation to equity, not just as a standalone number. A business with £35,000 in debt and £74,000 in equity is in a relatively comfortable position, as debt is less than half of the equity. A business with £200,000 in debt and £30,000 in equity is a different story entirely.

A simple way to check when you’re learning how to read a balance sheet: divide total liabilities by total equity. A figure below 1 means equity exceeds debt. Above 1 means debt exceeds equity. Neither is automatically good or bad, but it’s a number every business owner should know.

How to Do Balance Sheet Analysis: How to Read a Balance Sheet Beyond the Basics

Numbers on a page don’t mean much without context. Once you know how to read a balance sheet, understanding how to do balance sheet analysis using these three ratios turns it from a compliance document into a useful management tool.

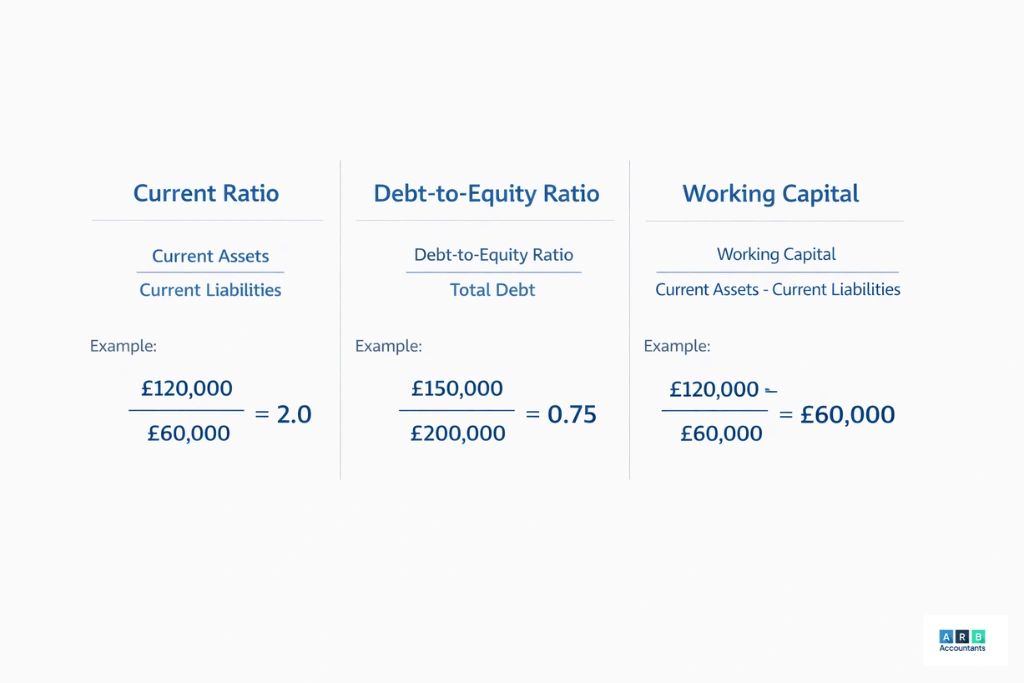

Current Ratio

Current assets divided by current liabilities

In our example: £39,700 divided by £15,700 = 2.5

A ratio above 1 means the business can cover its short-term debts with its short-term assets. Below 1 is a warning sign. Most lenders and investors want to see a current ratio of at least 1.5 before they’ll feel confident about a business’s short-term position.

Debt-to-Equity Ratio

Total liabilities divided by total equity

In our example: £50,700 divided by £74,000 = 0.68

This tells you how the business is funded. A lower number means you’re relying more on your own equity than on borrowed money, generally a stronger position. When you learn how to read a balance sheet for borrowing purposes, this is the ratio lenders look at hardest.

Working Capital

Current assets minus current liabilities

In our example: £39,700 minus £15,700 = £24,000

Working capital is the cash available to run the business day to day. Businesses that run low on working capital even profitable ones can find themselves unable to pay suppliers or staff.

READ RELATED ARTICLE: What Does a Good Balance Sheet Look Like?

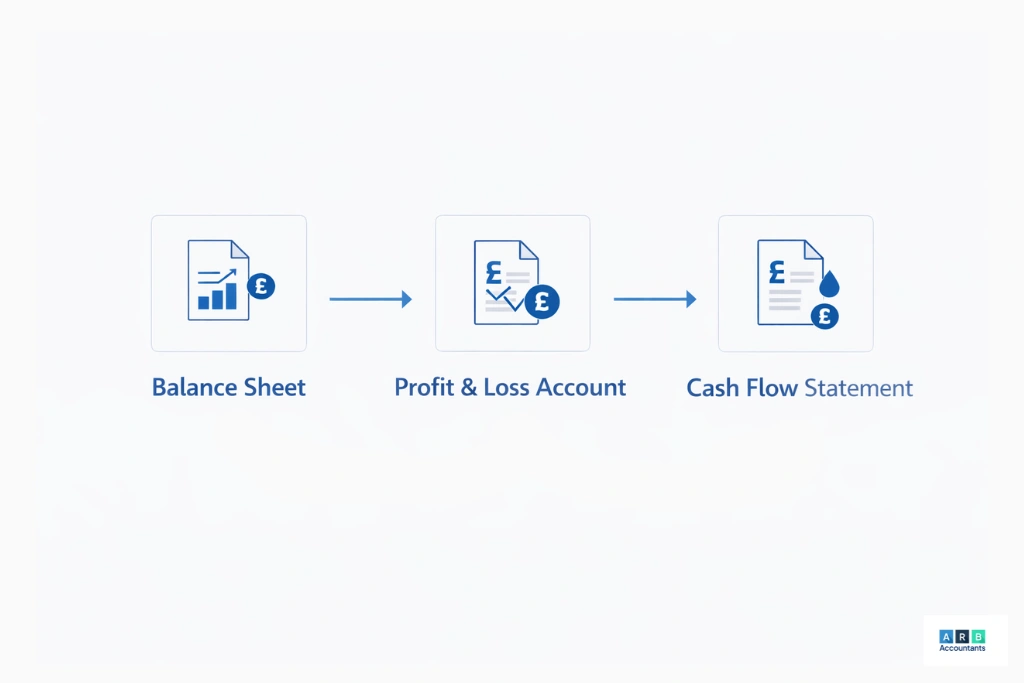

Understanding Financial Statements: How to Read a Balance Sheet in Context

Knowing how to read a balance sheet properly means looking beyond just one document. Understanding financial statements requires reading the balance sheet alongside two others.

The profit and loss account shows your revenue, costs and profit over a period. If profits are growing but retained earnings on your balance sheet aren’t increasing at the same rate, you need to ask where the money is going: dividends, drawings, or something else.

The cash flow statement shows money moving in and out of the business. Here’s a scenario we see regularly: a business owner sees strong profits and wonders why cash is tight. Nine times out of ten, the balance sheet has the answer. A large and growing trade debtors figure means customers are taking longer to pay, and that gap between invoicing and receiving cash is exactly where the pressure comes from.

Understanding financial statements as a set, not just in isolation, is what separates business owners who manage proactively from those who react to problems. Working with an accountant on regular management accounts means you get this fuller picture throughout the year, not just at year-end when it’s too late to act.

READ RELATED ARTICLE: What Does a Good Balance Sheet Look Like?

What Are the Warning Signs on a Balance Sheet?

This is where most guides on how to read a balance sheet rarely go but it’s arguably the most useful part for a business owner.

Knowing how to read a balance sheet means knowing what healthy looks like and what doesn’t. Before we cover what does balance sheet show in terms of warning signs, here’s what to watch for:

Rising trade debtors with flat or falling cash. Customers are taking longer to pay. Your cash flow planning needs attention before this becomes a crisis.

Current liabilities are creeping close to or above current assets. Your current ratio is falling. Suppliers and HMRC are owed money you may not have liquid access to.

Retained earnings are falling year on year. The business is consistently losing money or paying out more than it earns. Either way, the equity base is eroding.

A balance sheet that doesn’t balance. Obvious, but worth stating, if the two sides don’t equal, there’s an error somewhere. Don’t file accounts until you know why.

Negative equity. The business owes more than it owns. This doesn’t always mean disaster, but it does mean the situation needs to be monitored closely and a clear recovery plan put in place.

Your Balance Sheet and Companies House: What UK Businesses Must File

One area that’s specific to how to read a balance sheet UK businesses produce is understanding what you’re legally required to file because that affects what level of detail you’ll see in your accounts.

Your filing obligations depend on your company’s size:

Micro-entities (turnover under £632,000, balance sheet total under £316,000, fewer than 10 employees) can file a simplified balance sheet under FRS 105. Much of the detail is condensed.

Small companies (turnover under £10.2m, balance sheet total under £5.1m, fewer than 50 employees) file under FRS 102 Section 1A. More detail is required, though some notes can be abbreviated.

Medium and large companies must file full accounts, including a detailed balance sheet, extensive notes, and, in most cases, an audit.

Most ARB clients fall into the micro or small company category. If you want help on how to do balance sheet preparation or filing correctly or just want to know what your filing obligations are, our accounts preparation service covers the full process and makes sure your balance sheet is both accurate and filed on time with Companies House.

Final Thoughts

Learning how to read a balance sheet doesn’t take an accounting qualification, and once you know how to read a balance sheet, you’ll use it every time you review your accounts. It takes a willingness to look past the profit figure and understand the full financial picture your business is carrying.

Your balance sheet tells you whether your business is truly stable, how much debt it’s servicing, whether customers are paying on time, and whether the equity you’ve built is growing or shrinking. Those aren’t abstract figures; they’re the numbers that determine whether your business can take on a new member of staff, survive a slow quarter, or secure finance for growth.

If you’d like help interpreting your balance sheet or want to use your accounts more actively as a management tool, our team of accountants in Essex works with business owners year-round to turn financial statements into genuine business insight. Get in touch with ARB Accountants to find out how we can help.

Frequently Asked Questions

What is balance sheet information and how does it differ from other accounts?

What is balance sheet information and how does it differ from other accounts?

What is balance sheet analysis at its core? It’s a financial statement that shows what your business owns (assets), what it owes (liabilities), and the resulting net worth of the business (equity) at a specific date. The assets must always equal the liabilities plus equity. That’s why it’s called a balance sheet and why knowing how to read a balance sheet starts with understanding that equation.

How do I read a balance sheet UK companies produce?

This is one of the most searched questions on the topic. To read a balance sheet UK style which is how to read a company balance sheet as filed at Companies House, start at the top with fixed assets, then current assets, then deduct current liabilities to reach net current assets. Deduct long-term liabilities to arrive at net assets, which must match the equity section at the bottom. Read each section in sequence and check that the final figures balance.

What does a balance sheet show that your profit figure misses?

The profit and loss account shows your trading performance over a period. What does balance sheet show that the P&L misses? Your financial position at a point in time, including your total debt, total assets, and the equity you’ve built up over the life of the business. Both are needed for a complete picture.

Where is debt on a balance sheet and how much is too much?

Short-term debt (due within 12 months) sits under current liabilities. Long-term debt (due after 12 months) sits under long-term or non-current liabilities. So where is debt on a balance sheet for a typical UK small business? Split across both sections. Add both together for the business’s total debt obligation.

What is equity in a balance sheet and why does it matter?

Equity in balance sheet terms is what remains for the owners once all liabilities are subtracted from all assets. For a limited company, it includes share capital and retained earnings. Growing equity year on year is one of the strongest indicators of a financially healthy business.

How often should I review my balance sheet?

Ideally every month, not just at year-end. If you only look at it once a year, you lose the ability to act on what it tells you. That’s the whole point of knowing how to read a balance sheet. Monthly management accounts give you an up-to-date balance sheet so you can spot problems early and make decisions based on current figures rather than numbers that are 12 months old.