Skip to content

Skip to content

End of Year Accounts Limited Company Checklist

Last updated:

January 10, 2026

As a director managing a trading entity, you understand the pressure of closing your books at the financial year end. When the phrase end of year accounts limited company appears, it often brings a mix of urgency and uncertainty. Completing your year end accounts checklist is not just about compliance, it reflects how accurately your business performance is recorded and presented. For limited companies, this process involves preparing statutory financial statements, confirming figures with your accountant, and ensuring submissions meet both Companies House and HMRC requirements.

In technical terms, limited companies accounts summarise the financial position of the business for a defined annual accounting period. This includes the profit and loss account, balance sheet, notes, and a director’s report. These documents must comply with the Companies Act 2006 and UK accounting standards such as FRS 105 or FRS 102. For most directors, understanding how to file end of year accounts is essential to maintaining good standing with regulators and avoiding penalties.

This guide explains the key stages of the end of year accounts limited company process, beginning with the critical filing deadlines and what every director needs to do well before submission.

Table Of Contents

show

- What deadlines apply to end of year accounts limited company filings?

- How do you define the accounting period and choose the year-end date?

- What key records and data must you gather ahead of your year-end accounts limited company?

- Which adjustments and accruals matter for an accurate end of year accounts limited company?

- How do you prepare and analyse the statutory financial statements?

- What are the filing obligations at HMRC and Companies House for a limited company’s year-end?

- What year-end tax-planning opportunities should a limited company consider?

- How can digital accounting and cloud-based workflows streamline the end of year accounts limited company process?

- What are the common pitfalls when preparing end of year accounts?

- Conclusion

- Frequently Asked Questions

What deadlines apply to end of year accounts limited company filings?

One of the most important aspects of your year end accounting checklist is understanding when to submit statutory accounts. According to GOV.UK, private limited companies must file their end of year accounts at Companies House within nine months of the accounting period’s end. The corporation tax return and payment must reach HMRC no later than nine months and one day after that same year end.

The accounts filing deadline is non-negotiable. Late submissions can result in automatic financial penalties that escalate quickly. As detailed by Concept Accountancy, missing the Companies House deadline by up to one month incurs a £150 fine, rising to £375 after three months, £750 after six months, and £1,500 beyond that. Persistent delays can also damage your company’s credit profile and raise compliance concerns with lenders or investors.

To stay compliant, directors should treat the limited company end of year accounts process as an ongoing responsibility rather than a one-off task. Use your accounting software to set reminders 4–6 weeks before deadlines and schedule an internal review before your accountant finalises the numbers. This practice not only ensures accuracy but allows enough time for necessary adjustments such as accruals, prepayments, and reconciliation of the director’s loan account.

For example, if your company’s financial year ends on 31 March, it is advisable to complete reconciliations by 31 May, send the draft accounts to your accountant by 30 June, and submit the final end of year accounts limited company filing by 30 September. Following this structured timeline keeps your compliance intact and helps maintain financial visibility, making the year end accounts checklist a foundation for smarter business planning.

How do you define the accounting period and choose the year-end date?

The accounting period is the duration for which your company’s financial performance is measured and reported. As defined by Wikipedia, it usually runs for twelve months and determines when your end of year accounts limited company filings and corporation tax are due. It begins when a company starts trading and ends on its chosen accounting reference date, forming the foundation of the annual accounting period for both Companies House and HMRC reporting.

Many directors select 31 March or 30 June as their year-end. The 31 March date aligns with the personal tax year, making it easier to coordinate director dividends and personal tax obligations. A 30 June year-end suits companies with seasonal trading patterns or irregular cash flow, offering more breathing space after a busy quarter. Your choice influences how you manage profit recognition, stock valuation, and limited companies accounts preparation, which all form part of the year end accounts checklist.

When reviewing how to do year end accounts, it helps to assess cash flow forecasts and trading cycles at least six months before the year-end. If heavy spending, asset investment, or reduced income is expected, adjusting the accounting reference date can ease reporting pressure. Small and micro-entity exemptions also depend on company size and year-end date. Micro-entities can file simplified statements, but must still comply with the accounts filing deadline and maintain accuracy in their limited company end of year accounts.

READ RELATED ARTICLE: Salary vs Dividends: What Is the Best Way to Pay Yourself

What key records and data must you gather ahead of your year-end accounts limited company?

Preparing your end of year accounts limited company accurately depends on organised recordkeeping. According to Daafl, directors should compile sales invoices, purchase receipts, bank statements, payroll reports, VAT returns, stock counts, and a fixed asset register. These records feed directly into your year end accounting checklist, ensuring every transaction aligns with the correct accounting period.

To streamline work, adopt a digital folder strategy in your cloud software. Organise receipts and reconciliations monthly and tag entries related to the director’s loan account. This prevents missing documents during the review stage. For instance, contractor businesses often track equipment depreciation and reconcile director’s loan balances each month to maintain clarity. Establishing such systems simplifies how you file end of year accounts, reduces last-minute errors, and strengthens audit readiness for your end of year accounts limited company.

READ RELATED ARTICLE: How Does a Director’s Loan Account Work

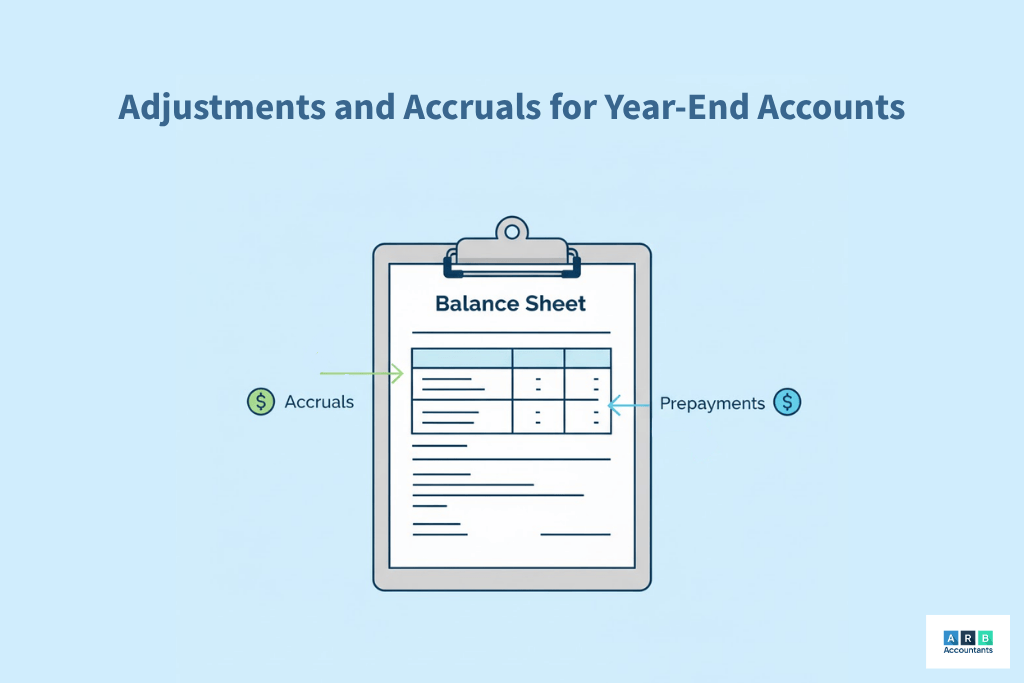

Which adjustments and accruals matter for an accurate end of year accounts limited company?

Accruals and prepayments are critical when preparing end of year accounts limited company reports. Accruals record expenses incurred but not yet paid, while prepayments represent costs paid in advance but not yet used. Ignoring these adjustments can distort the company’s profit position and working capital. For example, a limited company with £5,000 prepaid maintenance in April should only recognise the portion relating to the months before the accounting period closes. This ensures compliance with the accruals concept under FRS 102.

Another essential element in a year end accounting checklist is fixed-asset depreciation and disposals. Your fixed-asset register and depreciation schedule must be updated to reflect asset additions, disposals and accumulated depreciation. A mismatch between the register and the trial balance can lead to errors in statutory accounts and inflated balance sheets. For limited companies accounts, this review also confirms that capital allowances align with HMRC’s annual investment allowance limits.

How do you prepare and analyse the statutory financial statements?

Once adjustments are complete, the next step in the year end accounts checklist is preparing statutory financial statements. These include the profit and loss account, balance sheet, notes to the accounts, and the directors’ report. For every limited company end of year accounts, accuracy in classification and disclosure is vital to meet Companies Act 2006 requirements and filing deadlines.

ARB’s view is that the end of year accounts limited company process should go beyond compliance. We treat the annual accounting period as a strategic review opportunity. Our accountants analyse liquidity and profitability ratios such as current ratio, debt-to-equity, and net margin. A heat-map identifies one-off or exceptional costs that may not recur. For example, if net margin drops from 20% to 12%, we investigate underlying cost categories and advise whether operational restructuring is necessary.

By turning the statutory filing into a management insight exercise, businesses gain clarity before submitting accounts to Companies House and HMRC. This ensures accurate financial reporting and informed decision-making across the next financial year.

What are the filing obligations at HMRC and Companies House for a limited company’s year-end?

Companies House must receive your statutory accounts, while HMRC requires the company tax return, the CT600, with tax computations and supporting schedules. The statutory accounts create the public record for limited companies accounts, while the CT600 reconciles accounting profit to taxable profit. Because these are separate submissions, reconciling the nominal ledger to the tax computation is an essential control in any year end accounts checklist. Micro-entity and small company regimes allow simplified disclosures for qualifying companies, typically under FRS 105, which can reduce the level of notes and disclosures required. Confirm eligibility by checking turnover, balance sheet totals and employee numbers before electing a simplified route, see guidance. (source) For dormant or very low turnover entities, different filing options exist and these change the practical steps needed to file end of year accounts.

When preparing supporting schedules prepare separate reconciliations for share capital movements, related party transactions, contingent liabilities and deferred tax positions. These working papers support the statutory statements and make the numbers easier to validate when you file end of year accounts. Companies House applies stepped penalties for late statutory accounts. Consult the official penalties guidance to understand the scales and appeal routes. (source) Documenting the filing path, and the person responsible for each submission, reduces the risk that administrative change causes a missed accounts filing deadline.

What year-end tax-planning opportunities should a limited company consider?

A pre year-end tax review can meaningfully change the corporation tax charge and near term cash flow. Consider timing deductible expenditure, crystallising capital allowances, documenting R and D claims where qualifying, and confirming pension contribution treatment within the annual accounting period. From April 2023 the main corporation tax rate for companies with profits above the upper threshold is 25 percent, with marginal relief rules for intermediate profits. (source)

Practical steps include reconciling capital allowance pools, validating carried forward losses, and documenting the commercial rationale for accelerated expenditure. Contractors may accelerate qualifying purchases into the current annual accounting period to maximise relief, while R and D claimants should collate technical records before filing. Record the decisions and the supporting calculations in your year end accounting checklist. Clear documentation both supports the figures in limited company end of year accounts and provides an audit trail that explains how to do year end accounts in a tax compliant way.

READ RELATED ARTICLE: Do All Businesses Pay Corporation Tax?

How can digital accounting and cloud-based workflows streamline the end of year accounts limited company process?

Cloud-based accounting systems such as Xero, QuickBooks Online, and FreeAgent have redefined how limited companies manage their books. Instead of exporting spreadsheets at the year-end, real-time bank feeds and automatic reconciliation keep ledgers continuously updated. This approach transforms the end of year accounts limited company process from a reactive task into a controlled workflow. Using a year end accounts checklist inside your accounting software ensures that all adjustments, reconciliations, and verifications are logged throughout the year, not just at closing.

Digital receipt capture tools like Dext or Hubdoc also eliminate missing paperwork, helping directors maintain accurate audit trails. These integrate directly into the general ledger, allowing expenses to be matched against bank transactions in real time. Automated reconciliation rules classify transactions consistently, while machine learning suggestions speed up coding for regular suppliers. When your cloud dashboard is maintained weekly, the year-end review becomes a validation exercise rather than a data entry marathon.

A clear advantage of digital-first processes is visibility. Directors can monitor KPIs such as gross margin or debtor days through live dashboards, allowing informed financial decisions within the annual accounting period. This also simplifies collaboration with accountants and auditors who can securely access the same ledgers and working papers online. For example, a company that maintains bank-feed reconciliation every week will only need final adjustments at the year-end, not a complete catch-up. This structured, real-time workflow significantly reduces the risk of errors when you file end of year accounts and improves confidence in the final numbers.

What are the common pitfalls when preparing end of year accounts?

Many directors underestimate how easy it is for small mistakes to snowball into major accounting errors. The most frequent pitfalls include missing supplier invoices, incorrect director’s loan postings, and recording personal expenses as business transactions. These mistakes can distort profit and lead to inaccurate limited companies accounts. Missing accruals or prepayments also misstate financial results, affecting corporation tax computations and compliance accuracy.

Another recurring issue is poor debtor management. For example, a small company that fails to chase unpaid invoices in the final quarter could record inflated profits and overpay corporation tax. Introducing a structured debtor follow-up process within the year end accounting checklist helps correct this before submission. Late filing penalties remain a serious risk, with Companies House fines escalating the longer the delay. (source) Implementing automated reminders within your accounting platform ensures that the accounts filing deadline is never missed. By following clear digital workflows, documenting reconciliations, and validating every balance, you create robust limited company end of year accounts that withstand both audit and HMRC review.

Conclusion

To complete your end of year accounts limited company process effectively, set a closing date early and confirm all reconciliations by a soft-close deadline. Run a pre-year-end tax planning review, organise financial records digitally, and follow a structured year end accounting checklist to maintain compliance and clarity before submission.

Frequently Asked Questions

What constitutes the accounting period for my limited company?

What constitutes the accounting period for my limited company?

Your accounting period covers the time from incorporation or your previous year-end to the next chosen closing date. It defines when profits are assessed for corporation tax and when you must file end of year accounts. For most businesses, the accounting period aligns with the company’s financial year in Companies House records.

Can I change my limited company’s year-end date?

Yes, you can shorten or extend the annual accounting period by notifying Companies House. Many directors adjust it to match the tax year or to balance seasonal revenue. However, you can only extend a financial year once every five years, so review your trading cycle before making changes.

What happens if I miss the filing deadline for my end of year accounts?

Missing the accounts filing deadline triggers automatic penalties from Companies House and HMRC. Fines increase the longer the delay. Late submissions can also affect your company’s credit rating and reputation with lenders, so it is crucial to finalise all reports within your year end accounts checklist.

Do I need to prepare a cash flow statement for my year-end accounts?

Small and micro-entities are often exempt, but larger firms must include one in their limited companies accounts. Even if not mandatory, tracking inflows and outflows helps assess liquidity before closing your limited company end of year accounts.

What qualifies as related-party disclosures in my annual accounts?

Any transactions between the company and directors, shareholders, or connected businesses must be disclosed. This ensures transparency and compliance with statutory reporting standards.