Skip to content

Skip to content

How to Pay Yourself From a Limited Company: The Director’s Guide (2026)

Last updated:

April 23, 2026

Knowing how to pay yourself from a limited company is one of the most important financial decisions you will make as a director. Get it right and you keep more of what your business earns. Get it wrong and you could face unnecessary tax bills, NI charges, or HMRC scrutiny.

Most directors we work with use a combination of salary, dividends, and pension contributions to structure their income efficiently. But the exact split depends on your profits, your personal circumstances, and how the company is set up. This guide walks you through each method, the 2026/27 tax figures you need to know, and the real-world trade-offs between each approach.

If you are figuring out how to pay yourself from a limited company for the first time, or reviewing a structure that has not been looked at in a while, this guide will give you a clear, practical foundation.

Tax rules can change. The figures in this guide reflect the 2026/27 tax year. Always speak with a qualified accountant before finalising your income structure.

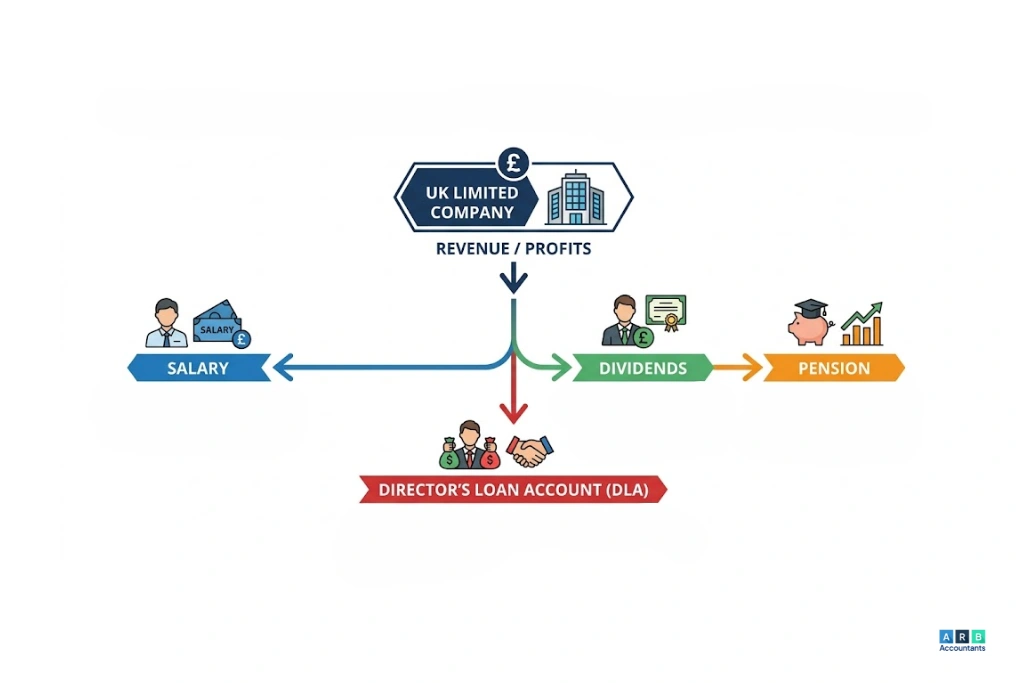

Why Getting Paid Through a Limited Company Is Different

Getting paid through a limited company is not the same as receiving a wage from an employer. You are not just an employee. You are also the shareholder, and often the sole director. That gives you options most employees never have.

Your company earns profits, pays corporation tax at 19% (for profits up to £50,000) or up to 25% (for profits above £250,000), and then you decide how to take money out. That decision affects your personal tax bill significantly.

This separation between company money and personal income is central to understanding how to pay yourself from a limited company. The company’s money is not your money until you draw it out in one of the permitted ways.

There are four main routes:

- A director’s salary through PAYE

- Dividends from company profits

- Employer pension contributions

- A director’s loan

Understanding each one is the key to structuring your income as tax-efficiently as possible.

How to Pay Yourself a Salary From a Limited Company

The most straightforward route is salary. Your company registers as an employer, runs payroll through PAYE, and pays you a regular amount each month. It is the most familiar structure for directors who previously worked as employees.

Why Most Directors Take a Low Salary

Most limited company directors do not pay themselves a large salary, and there is a good reason for that. Salary is subject to both income tax and National Insurance Contributions (NICs) for you as the employee and for the company as the employer. Keeping salary low reduces these costs significantly.

How to pay yourself a salary from a limited company in the most tax-efficient way usually means setting it at one of two levels.

Option 1: At the Lower Earnings Limit (£6,708 for 2026/27)

Setting your salary at £6,708 per year means you protect your State Pension entitlement (because you are earning above the Lower Earnings Limit) without triggering any income tax or NI for you or the company. This is a popular choice for single-director companies that are not eligible for the Employment Allowance.

Option 2: At the Personal Allowance (£12,570 for 2026/27)

If your company has other employees and qualifies for the Employment Allowance (up to £10,500 in 2026/27), you may be able to take a salary up to £12,570 without paying income tax and with the employer NI offset by the allowance. The salary is also a deductible business expense, which reduces your corporation tax bill.

2026/27 Key Salary Thresholds

| Threshold | Amount |

| Personal Allowance | £12,570 |

| Lower Earnings Limit (LEL) | £6,708 |

| Employee NI Primary Threshold | £12,570 |

| Employer NI Secondary Threshold | £5,000 |

| Employer NI Rate (above £5,000) | 15% |

| Employment Allowance | Up to £10,500 |

A common situation we see is a director paying themselves £12,570 in salary but then receiving an unexpected employer NI bill because they forgot the secondary threshold dropped to £5,000 in recent years. Keep that figure in mind when setting your salary level.

Salary reduces the company’s taxable profits, which means it reduces your corporation tax liability. This is one reason why paying at least a small salary is often better than taking everything as dividends.

How to Pay Yourself Dividends From Your Limited Company

Once your company has made a profit and paid corporation tax on it, you can distribute the remaining profit to shareholders as dividends. This is the most popular method of getting paid through a limited company because dividend tax rates are lower than income tax rates.

How to pay yourself dividends from your limited company starts with confirming you have distributable profits. You cannot legally pay dividends from a company that has not made a profit. Each dividend payment requires a board resolution (even if you are the only director) and a dividend voucher.

The Dividend Allowance and Tax Rates for 2026/27

The tax-free dividend allowance is £500 for 2026/27. This is separate from your Personal Allowance.

When you combine your Personal Allowance (£12,570) and the Dividend Allowance (£500), you can receive up to £13,070 in total income free of income tax in 2026/27, assuming no other income.

Dividends above this threshold are taxed as follows:

| Band | Tax Rate (2026/27) |

| Basic rate (up to £50,270) | 10.75% |

| Higher rate (£50,270 to £125,140) | 33.75% |

| Additional rate (above £125,140) | 39.35% |

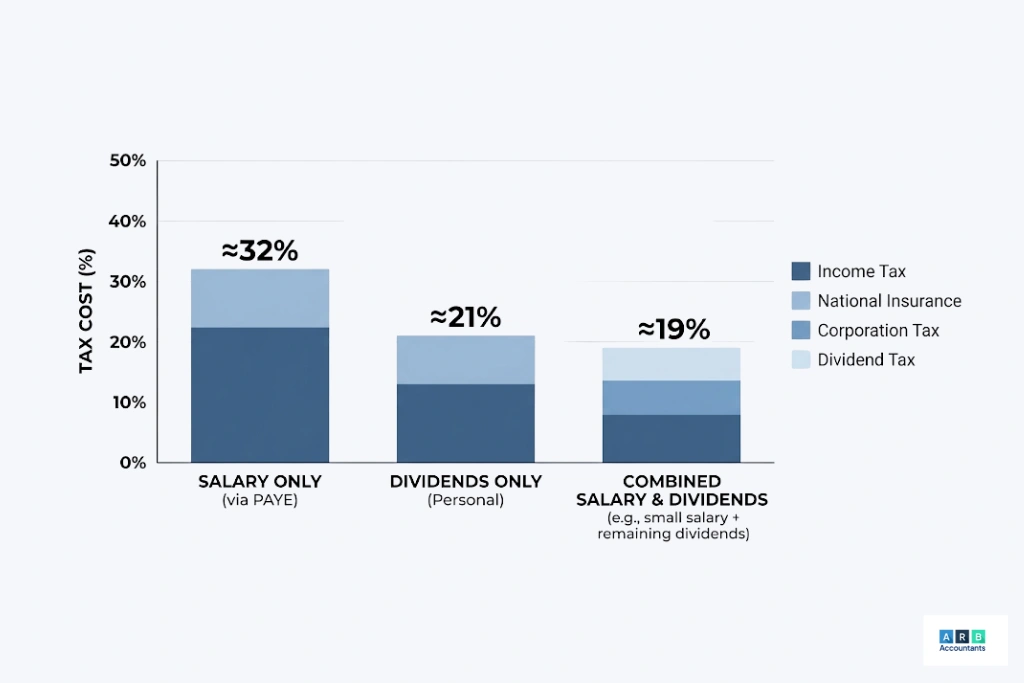

Paying yourself dividends is substantially cheaper in tax terms than taking an equivalent salary. A director taking £40,000 in dividends (after a £12,570 salary) will pay significantly less in combined income tax and NI than someone drawing the full £52,570 as a salary. That difference is one of the main reasons people set up limited companies in the first place.

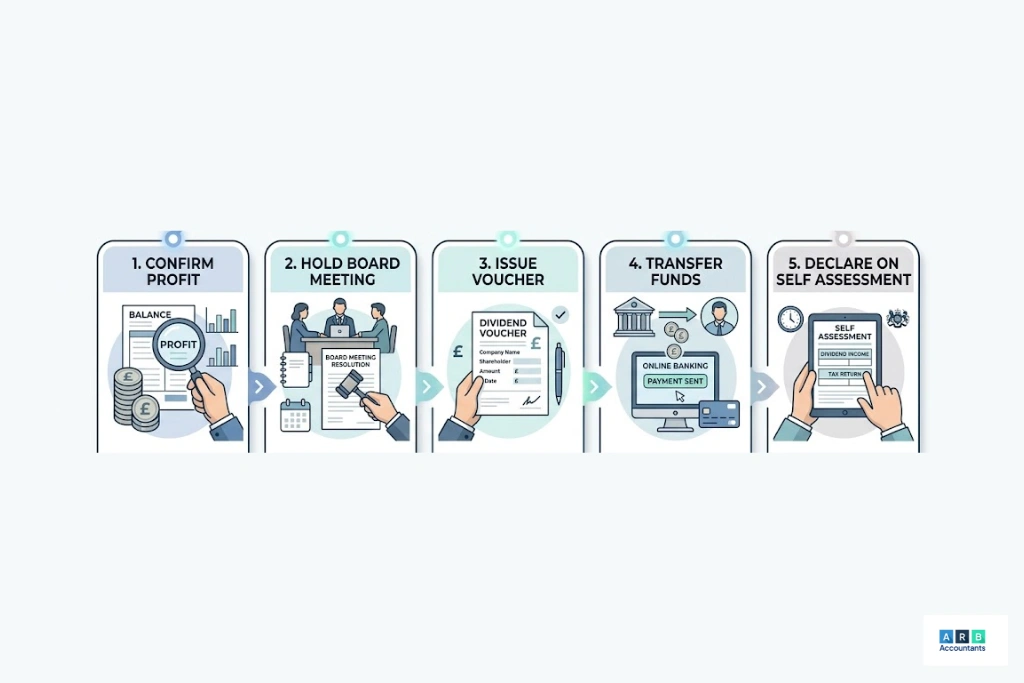

How Do You Pay Yourself Dividends: The Process

How do you pay yourself dividends correctly? Here is what is required:

- Confirm the company has sufficient distributable profits in its retained earnings

- Hold a directors’ meeting and document the decision to declare a dividend

- Issue a dividend voucher showing the date, amount, and company name

- Transfer the funds from the company account to your personal account

- Report the dividend income on your Self Assessment tax return

Pay yourself dividends correctly every time. HMRC will challenge dividends that lack proper documentation or that exceed distributable profits. These can be reclassified as salary, which triggers full PAYE and NI charges.

What Is the Most Tax Efficient Way to Pay Yourself?

The most tax efficient way to pay yourself from a limited company is almost always a combination of a low director’s salary and dividends rather than either method alone. But the precise balance depends on your profits and personal tax position.

Here is a practical example for 2026/27:

A director whose company generates £80,000 in net profits before their remuneration might structure their income like this:

- Director’s salary: £12,570 (uses Personal Allowance, no income tax due, salary is corporation tax deductible)

- Dividend: £37,700 (taxed at 10.75% basic rate, with the £500 Dividend Allowance covering the first £500)

- Total personal income: £50,270 (stays within the basic rate band)

- Retained in company: balance available for reinvestment or future extraction

This is what is the most tax efficient way to pay yourself if you want to keep your tax bill low while drawing a reasonable income. The combined tax burden on this structure is significantly lower than it would be if the same £50,270 were drawn as a salary.

However, if your personal income rises above £50,270, dividends attract the higher rate of 33.75%, and the calculation shifts. For higher earners, pension contributions become increasingly valuable.

READ RELATED ARTICLE: Salary vs Dividends: What Is the Best Way to Pay Yourself

Pension Contributions: The Overlooked Option

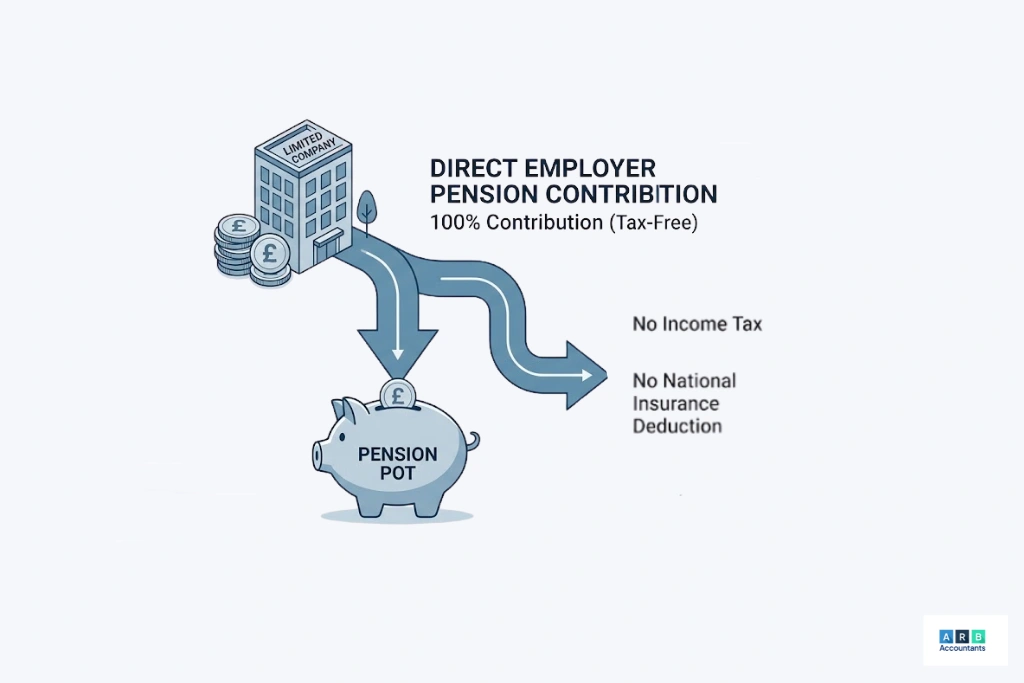

Pension contributions are one of the most tax-efficient tools available to limited company directors, and they are often underused.

Your company can make employer pension contributions directly from company profits. These contributions are not subject to corporation tax, income tax, or National Insurance. That makes them one of the most efficient ways to extract money from a company, particularly for directors who are higher-rate taxpayers.

For the 2026/27 tax year, the annual pension allowance is £60,000. You can contribute up to this amount across all pension sources combined (including both employer and personal contributions). For most owner-directors, this limit is rarely hit.

To illustrate the benefit: if your company makes a £10,000 pension contribution on your behalf, that £10,000 reduces the company’s taxable profits. No corporation tax is due on it, no income tax, and no NI. Compare that to taking £10,000 as salary, where both you and the company pay NI and you pay income tax on top.

If you are approaching retirement, or if your profits regularly exceed what you need to live on, pension contributions deserve a close look as part of your overall income strategy.

Director’s Loans: What They Are and When to Use Them

A director’s loan is money you borrow from your own company, or money you pay into it that is not salary, dividends, or expenses. It sits in a director’s loan account (DLA) and needs to be tracked carefully.

When you borrow from the company (an overdrawn DLA), the company must pay a 33.75% Section 455 tax charge on the outstanding balance if the loan is not repaid within nine months of the company’s year-end. You personally may also face a benefit-in-kind tax charge if the loan exceeds £10,000 and is not charged at HMRC’s official rate.

When you lend money to the company, it creates a credit balance in your DLA. You can repay yourself this money tax-free at any point because you are repaying a loan, not extracting profit.

Director’s loans are not a regular income method, but they can be a useful short-term cash flow tool, particularly in the early months of a business before profits build. Use them carefully, document everything, and make sure any overdrawn balance is cleared promptly.

READ RELATED ARTICLE: How Does a Director’s Loan Account Work?

The Limited Company Tax Free Allowance: What You Can Use

The limited company tax free allowance is not a single figure. It is actually a combination of allowances that work together to reduce your personal tax bill.

For 2026/27, these are the key allowances available to a director:

| Allowance | Amount |

| Personal Allowance | £12,570 |

| Dividend Allowance | £500 |

| Total income free of tax | £13,070 |

| Annual Pension Allowance | £60,000 |

The tax free allowance limited company directors use most often is the Personal Allowance applied against a low salary. By keeping your salary at £12,570, you receive this income without paying income tax. Then the £500 dividend allowance covers the first £500 of dividend income on top.

If you have a spouse or civil partner who holds shares in the company, they also benefit from their own Personal Allowance and Dividend Allowance. This can double the tax-free threshold available to a household, which is a legitimate and widely used planning approach. You should take professional advice before restructuring share ownership.

How to Pay Yourself as a Business Owner: Common Mistakes to Avoid

Knowing how to pay yourself as a business owner is one thing. Avoiding the common pitfalls is another.

These are the mistakes we see most regularly:

Paying too much salary. Some directors default to a market-rate salary without considering the NI and income tax implications. Even a small reduction in salary, offset by dividends, can save thousands each year.

Failing to document dividends. Dividends paid without board minutes and vouchers can be challenged by HMRC and reclassified as salary. This triggers NI and potentially penalties. Keep records every time.

Ignoring the corporation tax impact. How to pay yourself from your business affects not just your personal tax but also the company’s tax position. Salary reduces taxable profits; dividends do not. The interplay matters when you are calculating the net benefit of each approach.

Overlooking pension contributions. Many directors focus only on salary and dividends and miss the significant tax savings that pension contributions can provide.

Mixing personal and company finances. Taking money from the business account without declaring it as salary, dividends, or a formal loan creates accounting and tax problems. Always process payments correctly.

Paying yourself from your business UK means working within a structured framework. The flexibility is real, but so is the requirement to document and report each payment correctly.

How an Accountant Can Help You Structure Your Director’s Pay

Understanding how to pay yourself from a limited company in theory is one thing. Getting the balance right for your specific situation requires numbers, not guesswork.

An accountant who specialises in limited companies will review your company’s profits, your personal tax position, any other income you have, and your goals for the year, then work out the optimal salary and dividend split for you. They will also flag when pension contributions make sense and ensure your payroll and dividend records are correct.

Most business owners we work with save more in tax by having a properly structured remuneration plan than they spend on accountancy fees. That is particularly true when profits start growing and the decisions become more complex.

If you are looking for practical support with how to pay yourself from a limited company, our team of limited company accountants works with directors across Essex and beyond to get this right.

You can also explore our tax advice service if you want a dedicated review of your current structure.

Final Thoughts

How to pay yourself from a limited company is not a one-size-fits-all answer. The right structure depends on your profits, your other income, your plans for the business, and how close you are to key tax thresholds. For most directors, a low salary combined with dividends and employer pension contributions delivers the best outcome. But the numbers need to be modelled correctly for your situation.

If you have not reviewed your remuneration structure recently, now is a good time. Tax bands and allowances change, and a structure that was optimal two years ago may no longer be the most efficient approach.

Our team of accountants in Essex works with limited company directors at every stage to make sure they are not paying more tax than they need to. Get in touch to discuss your options.

Frequently Asked Questions

Can I pay myself from a limited company without running payroll?

Can I pay myself from a limited company without running payroll?

Not if you are taking a salary. Any salary payment to a director must go through PAYE and be reported to HMRC via Real Time Information (RTI). Dividends, however, do not go through payroll. If you take only dividends and no salary, you do not need to run payroll, but you lose the State Pension entitlement that comes from earning above the Lower Earnings Limit.

How often can I pay myself dividends from my limited company?

There is no set frequency. You can declare dividends monthly, quarterly, or annually, as long as the company has sufficient distributable profits each time. Most directors declare them quarterly or when the need arises. Each declaration must be properly documented with a board resolution and dividend voucher.

What happens if I take more money from the company than it has in profit?

If you take more than the company’s distributable profits as a dividend, that excess is classified as an illegal dividend. HMRC can challenge this, and it may be treated as a director’s loan or reclassified as salary with full tax and NI implications. Always confirm your retained profit position before declaring a dividend.

How to pay yourself from a limited company if it has made a loss?

You can still pay yourself a salary even if the company has made a loss, provided the company can fund it. You cannot, however, pay dividends from a loss-making company because there are no distributable profits. In a loss year, salary and pension contributions are the main tools available.

What is the most tax efficient way to pay yourself if you have other income?

If you have income from other sources (such as rental income, investment income, or a PAYE job), your Personal Allowance may already be used up. In that case, a salary from your limited company could push you into a higher tax band. Speak to an accountant to model the impact before setting your salary for the year.

Do I need to report dividends on a Self Assessment return?

Yes. Dividend income above the £500 allowance must be declared on your Self Assessment return. Even if you are a basic rate taxpayer, you will owe dividend tax on amounts above this threshold. HMRC cross-references company filings with personal tax returns, so unreported dividend income is regularly flagged.