Skip to content

Skip to content

How to Apply for a Tax Residency Certificate UK

Last updated:

March 12, 2026

A tax residency certificate UK is an official document issued by HM Revenue and Customs confirming that an individual or company is resident in the UK for tax purposes under a specific Double Taxation Agreement. HMRC refers to this as a Certificate of Residence, sometimes called a certificate of fiscal residence UK. The tax residency certificate HMRC issues is relied upon by overseas tax authorities to confirm treaty entitlement and prevent withholding tax.

It is important to distinguish a tax residency certificate UK from proof of tax residency UK such as a P60 or SA302. Those documents evidence income and tax paid, but they do not confirm treaty residence status. This guide explains how to apply for tax residency certificate requests correctly, who qualifies, and how to approach a certificate of residence application with compliance in mind. The focus is on PAYE employees, self assessment taxpayers, contractors, expats, and tax residency certificate UK limited company cases.

Table Of Contents

show

- What Is a Tax Residency Certificate UK and How Is It Different from Other HMRC Letters?

- Who Can Apply for a Tax Residency Certificate UK and What Are the Eligibility Criteria?

- How Do I Apply for a Tax Residency Certificate UK Step by Step?

- What Information Does HMRC Require When You Apply for a Certificate of Residence?

- How Long Does It Take to Get a Tax Residency Certificate HMRC and What Can Delay It?

- How Does a Tax Residency Certificate UK Limited Company Application Work?

- Do You Need a Tax Residency Certificate UK to Avoid Double Taxation?

- What Are the Most Common Mistakes When Applying for a Certificate of Residence UK?

- When Should You Seek Professional Advice Before You Apply for a Certificate of Residence?

- Conclusion

- Frequently Asked Questions

What Is a Tax Residency Certificate UK and How Is It Different from Other HMRC Letters?

A tax residency certificate UK is issued under the legal framework of bilateral Double Taxation Agreements. These treaties allocate taxing rights between jurisdictions and allow residents to claim reduced withholding tax. A hmrc tax residency certificate confirms that the applicant is UK resident within the meaning of a specific treaty article.

Other HMRC documents serve different functions:

- Tax residency certificate HMRC, formal treaty confirmation

- HMRC letter of confirmation of residence, sometimes issued in complex or non standard cases

- SA302 tax calculation, summary of declared income

- Proof of tax residency UK such as P60, evidence of employment tax deducted

| Document | Purpose | Accepted Internationally | Treaty Reference |

| Tax residency certificate UK | Confirms treaty residence | Yes | Explicit |

| Letter of confirmation | Context specific | Sometimes | May refer |

| SA302 | Income evidence | Rarely | No |

| P60 | PAYE record | No | No |

Foreign authorities usually require a certificate of fiscal residence in the UK where treaty relief is claimed at source. A certificate of residence application must therefore specify the relevant country and income type.

Who Can Apply for a Tax Residency Certificate UK and What Are the Eligibility Criteria?

Eligibility is determined by the Statutory Residence Test, which assesses days in the UK, sufficient ties, and overseas work patterns. HMRC applies this test before issuing a tax residency certificate HMRC document.

The following may apply:

- PAYE employees seeking proof for foreign dividend or interest claims

- Self employed individuals completing a certificate of residence application

- Mixed income earners with PAYE and overseas clients

- Non domiciled individuals claiming treaty benefits

- Companies requiring a certificate of residence for company status

A common confusion involves foreign clients versus foreign income. If work is physically performed in the UK, it is generally UK sourced, even if clients are abroad. This distinction affects how you apply for a certificate of residence and how you complete the form. HMRC requests client names and income breakdowns to confirm treaty alignment, particularly in tax residency certificate UK limited company cases.

For companies, a certificate of residence for the company is required when claiming treaty benefits or avoiding overseas withholding tax. This often links to broader business tax advice and cross border structuring.

If you are unsure how to get a certificate of residence UK in a complex scenario, professional review ensures your tax residency certificate UK request is consistent with filed returns and treaty definitions.

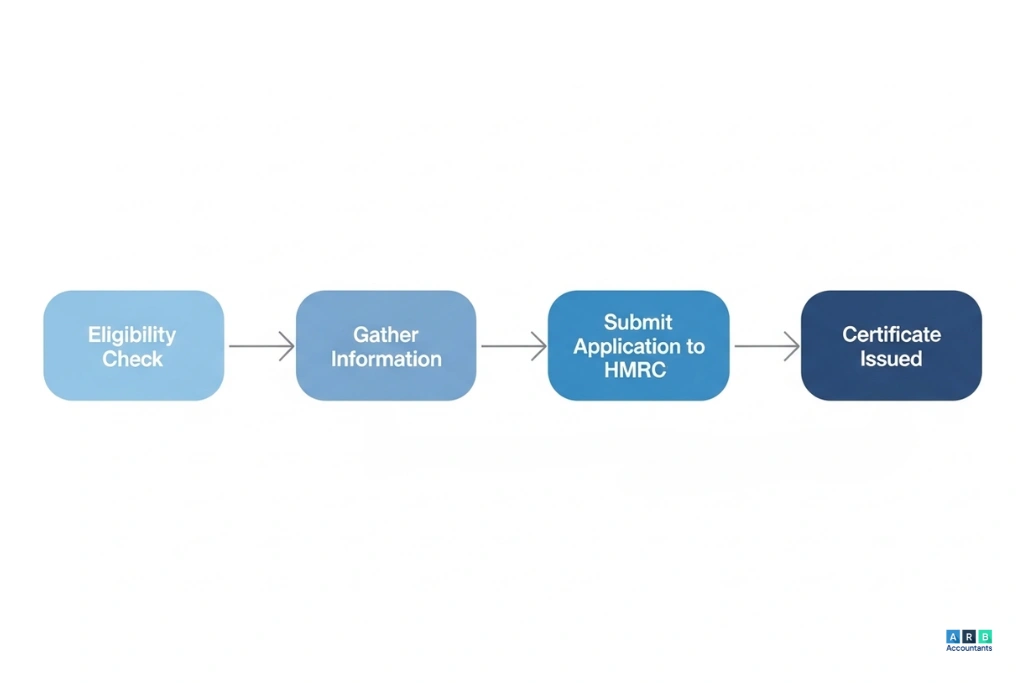

How Do I Apply for a Tax Residency Certificate UK Step by Step?

Understanding the procedural framework is essential before you apply for tax residency certificate confirmation. A tax residency certificate UK is issued by HM Revenue and Customs following a structured certificate of residence application process. HMRC offers three routes. You can apply online through your Government Gateway account, submit a paper form by post, or send a written request in complex treaty cases. The written route is often used where a tax residency certificate HMRC must include tailored wording for a specific treaty partner.

Step 1: Confirm Your Status Under the Statutory Residence Test

The first step in securing a tax residency certificate in the UK is confirming residence under the Statutory Residence Test. This involves:

- Days spent in the UK during the tax year

- Automatic overseas test for full time work abroad

- Sufficient ties test assessing family, accommodation, and work links

If residency is unclear, the HMRC tax residency certificate may be delayed. According to official service standards published by GOV.UK, most straightforward requests are processed within weeks, although complex reviews take longer.

Step 2: Identify the Relevant Income Category

When completing the certificate of residence application, you must specify the income type. Options include PAYE income, self employment, dividends, capital gains, and foreign source income. Many applicants asking how to get a certificate of residence in the UK misunderstand this section. Income earned from overseas clients but performed in the UK is typically UK sourced. Correct classification ensures your tax residency certificate HMRC aligns with your filed returns. The same principle applies to a tax residency certificate UK limited company where trading location determines source.

Step 3: Gather Supporting Information

Before you apply for certificate of residence status, collect:

- UTR and National Insurance number

- Relevant tax year

- Treaty country reference

Companies applying for a certificate of residence for a company must include Corporation Tax details. If the overseas authority requests a certificate of fiscal residence UK specifically, wording must reflect treaty terminology rather than generic proof of tax residency UK.

Step 4: Submit the Request and Consider Legalisation

Once submitted, the HMRC tax residency certificate is issued digitally or in hard copy depending on the country. If the receiving jurisdiction is part of the Hague Convention, an apostille may be required to authenticate the tax residency certificate UK for official use abroad

READ RELATED ARTICLE: Do All Businesses Pay Corporation Tax?

What Information Does HMRC Require When You Apply for a Certificate of Residence?

When submitting a certificate of residence application for a tax residency certificate UK, HM Revenue and Customs requires structured data to verify treaty entitlement. The tax residency certificate HMRC process is evidence based and cross checks against filed returns before issuing a HMRC tax residency certificate.

Key data fields include:

- Full legal name or company name

- Unique Taxpayer Reference and National Insurance number

- Relevant tax year

- Treaty country

- Type of income, such as employment, self employment, dividends or capital gains

HMRC requests client names and income amounts where foreign tax has been withheld or where foreign source income is declared. This is not administrative excess. It allows HMRC to confirm that the tax residency certificate UK reflects the correct treaty article and income stream. Applicants asking how to get a certificate of residence UK often overlook this alignment step when they apply for tax residency certificate confirmation.

Income classification is critical. UK based work for overseas clients is normally UK sourced. Foreign source income arises where the economic activity occurs abroad. Declaring the wrong category during the certificate of residence application can result in queries or delay. The same principle applies when you apply for a certificate of residence status as a sole trader with multi source income.

In mixed cases, such as PAYE employment combined with EU self employment income, HMRC reviews both streams before issuing a tax residency certificate HMRC document. If the overseas authority requires formal treaty wording, the certificate of fiscal residence UK must clearly reference the relevant convention rather than simple proof of tax residency UK.

READ RELATED ARTICLE: How Likely Are You to be Investigated by HMRC?

How Long Does It Take to Get a Tax Residency Certificate HMRC and What Can Delay It?

Processing times for a tax residency certificate UK vary depending on complexity. According to official service standards published by GOV.UK, most straightforward requests are handled within weeks, although complex reviews take longer. Delays commonly arise from incomplete self assessment filings, residency ambiguity under the Statutory Residence Test, or open compliance checks.

A tax residency certificate HMRC request will pause if submitted before returns are finalised. Ensuring filings are up to date before you apply for tax residency certificate confirmation reduces risk. Where delays exceed published timeframes, escalation through HMRC correspondence channels may be appropriate. For companies, similar review standards apply to a certificate of residence for company request.

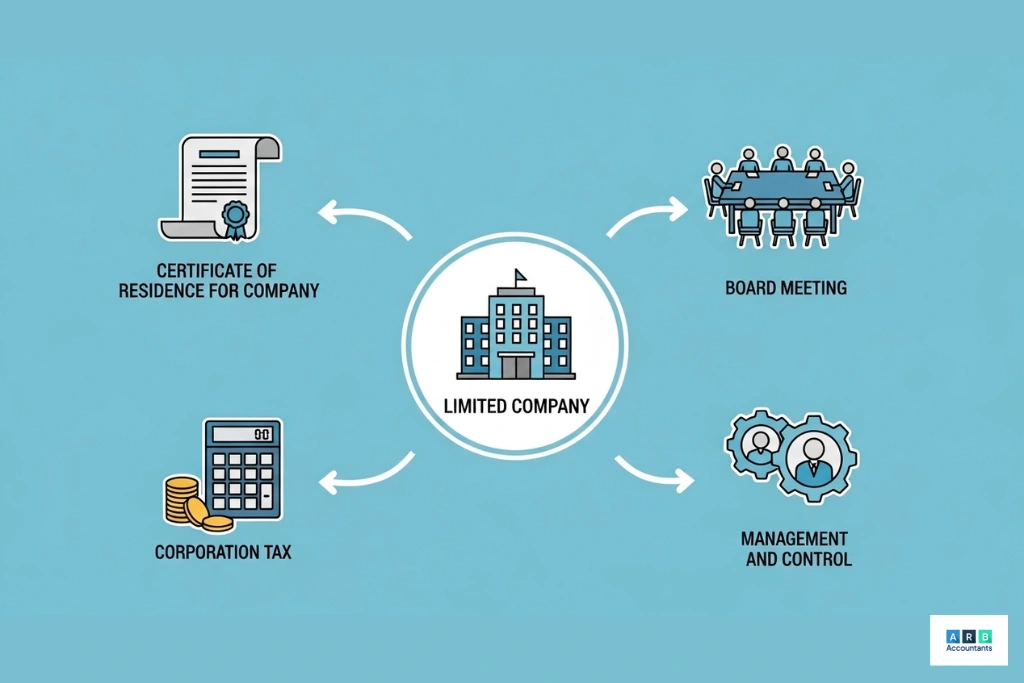

How Does a Tax Residency Certificate UK Limited Company Application Work?

A tax residency certificate UK limited company application focuses on corporate residence. A certificate of residence for the company is required when claiming treaty relief on overseas dividends, royalties or service income. HMRC examines the place of effective management, board control and Corporation Tax registration.

Permanent establishment rules may affect whether a tax residency certificate uk limited company qualifies for treaty protection. Where dual residence risk exists, treaty tie breaker tests determine which jurisdiction prevails. For example, a UK incorporated company operating in the EU must demonstrate central management in the UK before a HMRC tax residency certificate is issued.

In all cases, the tax residency certificate UK must correspond with filed Corporation Tax returns. If a foreign authority specifically demands a certificate of fiscal residence UK, wording must align precisely with treaty definitions rather than general proof of tax residency UK.

READ RELATED ARTICLE: End of Year Accounts Limited Company Checklist

Do You Need a Tax Residency Certificate UK to Avoid Double Taxation?

A tax residency certificate UK is typically required where a bilateral Double Taxation Agreement allocates taxing rights between two states.

Withholding tax relief at source versus reclaim

In a UK–Spain or UK–France scenario, local payers may deduct withholding tax unless a tax residency certificate HMRC is provided in advance. Relief at source reduces tax immediately. The reclaim method requires foreign tax to be deducted first, followed by a repayment claim supported by a HMRC tax residency certificate. The administrative burden differs significantly.

Verification by foreign authorities

Foreign tax offices verify authenticity directly with HMRC systems or by reviewing format, reference numbers and treaty citations. A certificate of fiscal residence in the UK must reference the correct convention article. Where treaty relief applies automatically, for example certain employment income articles, a formal proof of tax residency UK may not be requested, but complex dividend or royalty claims usually require a tax residency certificate UK limited company or individual certificate.

For groups, a certificate of residence for a company supports reduced withholding under corporate articles. Each application for a certificate of residence request must match the income type declared in the return.

What Are the Most Common Mistakes When Applying for a Certificate of Residence UK?

Errors in a certificate of residence application often delay a tax residency certificate UK.

Common issues include:

- Treating foreign clients as foreign source income when work is performed in the UK

- Selecting the wrong income category when you apply for tax residency certificate

- Submitting the request before filing returns that support the tax residency certificate HMRC

- Requesting the incorrect tax year on the HMRC tax residency certificate

- Using informal proof of tax residency UK instead of the official certificate of fiscal residence UK

- Failing to mirror treaty terminology in the apply for certificate of residence wording

These mistakes weaken the technical basis of the tax residency certificate uk and may trigger compliance review.

When Should You Seek Professional Advice Before You Apply for a Certificate of Residence?

Complex residency profiles require structured analysis before you apply for tax residency certificate status.

Higher risk scenarios

Professional review is advisable for:

- Cross border self employment with mixed source income

- Dual residency risk under treaty tie breaker tests

- Temporary non residence and split year treatment

- High value capital gains disposals

- Corporate management and control disputes affecting a tax residency certificate UKlimited company

A certificate of residence for company disputes may involve board minutes, strategic decision evidence and permanent establishment analysis. In these cases, a HMRC tax residency certificate must reflect precise factual positioning.

International tax compliance requires precise treaty interpretation, source analysis and correct completion of the certificate of residence application. A tax residency certificate UK issued by HM Revenue and Customs confirms residence status for treaty purposes and supports cross border withholding claims. Below are answers to common technical queries.

Conclusion

Before submission, confirm income classification, treaty wording and tax year accuracy. Misalignment between returns and your tax residency certificate UK can undermine foreign relief claims. Proactive planning is essential before relocation or expanding foreign income streams. For complex cases involving a tax residency certificate HMRC or certificate of residence for a company, specialist review ensures compliance and documentation strength. Businesses seeking chartered accountants in Southend benefit from structured cross border tax analysis and documentation strategy.

Frequently Asked Questions

How do I get a certificate of residence in the UK from HMRC?

How do I get a certificate of residence in the UK from HMRC?

Many ask how do I get a certificate of residence in the UK? You must apply for a tax residency certificate through HMRC’s online portal or by written request. The certificate of residence application requires your UTR, tax year and income category. Once approved, HMRC issues a HMRC tax residency certificate referencing the relevant treaty article.

How long does a UK tax residency certificate take?

HMRC states that most straightforward applications are processed within weeks. Complex cases, including a certificate of residence for a company or tax residency certificate for a limited company, may take longer due to management and control review.

Is a tax residency certificate the same as proof of tax residency UK?

No. Informal proof of tax residency uk, such as a tax return copy, differs from a formal certificate of fiscal residence uk. Overseas authorities generally require the official tax residency certificate HMRC.

Can I apply for a tax residency certificate UK online?

Yes. Most individuals apply for a certificate of residence digitally. The same system supports a tax residency certificate uk limited company request, provided Corporation Tax filings are up to date.

Do I need a certificate of fiscal residence in the UK every year?

Treaty partners often request an annual certificate of fiscal residence uk. Each tax residency certificate uk must match the specific tax year claimed.

Can a UK limited company apply for a tax residency certificate?

Yes. A certificate of residence for the company confirms UK corporate residence. Directors must apply for tax residency certificate status based on central management and control.

What if HMRC delays my certificate of residence application?

If a certificate of residence application is delayed, review filing status and correspondence. Escalation may be required where HMRC tax residency certificate processing exceeds standard timelines.